Mar 3, 2026

Tired of conflicting information about semaglutide costs? You have read that semaglutide can transform your weight management journey. You have heard the success stories. But then you looked at the price tag, and everything came to a halt. Brand-name Wegovy runs over $1,000 per month without insurance. Even compounded semaglutide typically costs between $150 and $350 per month depending on the provider and dosage. Over six to twelve months of treatment, that adds up to anywhere from $1,200 to over $4,200. For many people, that number is simply out of reach.

Here is what actually works. Buy now, pay later services like Afterpay, Klarna, and Affirm have entered the healthcare space, and they are changing the way people access semaglutide peptide treatments.

These platforms split your costs into smaller installments, often with zero interest, so you can start treatment without draining your savings account in a single swipe. Several telehealth providers now accept these payment methods directly at checkout, making the entire process surprisingly straightforward.

But not every buy now, pay later option works the same way. Some charge interest. Some require credit checks. Some have spending limits that will not cover a full month of medication. And not every semaglutide provider accepts every platform. This guide breaks down exactly how Afterpay works for semaglutide purchases, which telehealth providers accept it, what alternatives exist, and how to combine these tools with insurance savings programs and manufacturer discounts to bring your total cost as low as possible. Whether you are just starting to explore how to qualify for semaglutide or you have already been prescribed it and need a better way to pay, this is the complete financial playbook.

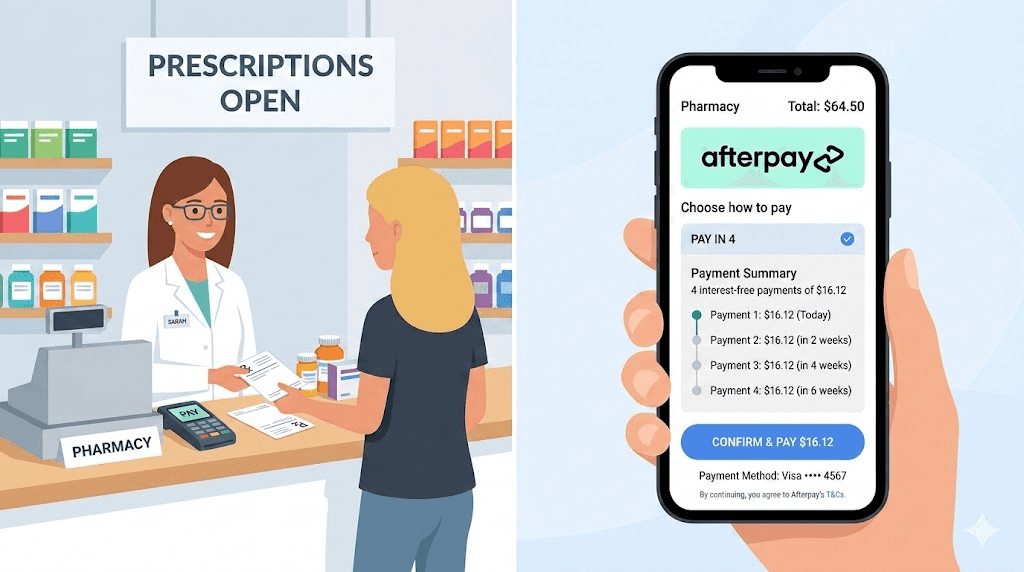

How Afterpay works for semaglutide purchases

Afterpay is a buy now, pay later platform that splits a purchase into four equal payments spread over six weeks. You pay the first installment at checkout. The remaining three payments are automatically charged to your linked debit or credit card every two weeks after that. No interest. No fees, as long as you pay on time. Late payments do trigger fees, typically around $8 per missed installment, capped at 25% of the original purchase price.

The approval process is fast. Afterpay runs a soft credit check that does not affect your credit score. You need to be at least 18 years old, a United States resident, and have a valid debit or credit card on file. Most approvals happen instantly. There is no lengthy application, no income verification paperwork, and no waiting period. You find out right away whether you qualify.

For semaglutide, this means a $300 monthly prescription becomes four payments of $75 every two weeks. A $200 monthly plan turns into four payments of $50. That kind of breakdown can make a real difference when you are budgeting for ongoing semaglutide dosage treatment alongside other monthly expenses.

Here is how the payment timeline actually looks in practice. Say you purchase your first month of semaglutide on March 1. Payment one comes out immediately. Payment two hits on March 15. Payment three arrives March 29. Payment four finalizes on April 12. By then, your next monthly subscription charge may already be due, creating a new cycle of four payments that overlaps with the tail end of your first cycle. This rolling structure is the single most important thing to understand about using Afterpay for an ongoing medication. It is not a one-time event. It is a repeating financial commitment that requires consistent budgeting.

Spending limits and how they affect semaglutide payments

Afterpay does impose spending limits. New customers typically start with a limit between $150 and $500. As you build a history of on-time payments, that limit can increase over time, sometimes reaching $1,500 or more. For most compounded semaglutide programs, the starting limit should cover at least one month of treatment.

However, if you are purchasing brand-name Wegovy or Ozempic at full retail price (often exceeding $900 per month), the standard Afterpay Pay-in-4 limit may not be enough. In that case, Afterpay does offer a "Pay Monthly" option for purchases over $400, which extends repayment over 6 or 12 months. The catch? This option does carry interest, with APR ranging from 6.99% to 35.99% depending on your creditworthiness.

Understanding these limits matters. If you are working with a telehealth provider that charges $249 per month for a semaglutide 5mg dosage program, the standard Pay-in-4 should work fine from day one. If you are looking at a more expensive option like a semaglutide 10mg program or brand-name medication, you may need to explore the monthly payment option or look into one of the alternative BNPL providers covered later in this guide.

What happens if you miss a payment

Missing an Afterpay payment triggers a late fee. The first late fee is $8. If the payment remains overdue, an additional $8 fee may apply, but total late fees will never exceed 25% of the purchase price. Afterpay will also freeze your account, preventing you from making new purchases until the balance is settled. Repeated missed payments can result in the account being sent to collections, which absolutely will impact your credit score.

This is worth keeping in mind because semaglutide treatment is ongoing. You are not making a single one-time purchase. Each month brings a new payment cycle. If you plan to use Afterpay consistently, you need to be confident that you can handle four biweekly payments every single month for the duration of your treatment, which could last one month at minimum but often extends to six months, twelve months, or longer depending on your semaglutide dosage chart and weight management goals.

Telehealth providers that accept Afterpay for semaglutide

Not every online semaglutide provider accepts Afterpay. The landscape changes frequently as providers add and remove payment options, so it pays to verify directly before committing. That said, several established telehealth platforms have integrated Afterpay, Klarna, or both into their checkout processes.

Providers with confirmed Afterpay or BNPL support

Elevate Health stands out as one of the more payment-flexible telehealth platforms. They accept Afterpay, Klarna, and Affirm, giving patients three different buy now, pay later options at checkout. The platform also includes free blood work with their programs, which is a meaningful cost savings on its own. For patients exploring how semaglutide makes you feel and wanting to try treatment without a massive upfront commitment, the multiple financing options make the barrier to entry significantly lower.

Semaglutide Online is another telehealth platform that has integrated Klarna directly into their payment flow. Patients can split costs into four interest-free payments, and prescriptions are typically approved within 24 hours. The platform connects patients with board-certified providers who manage the entire treatment process, from initial consultation through ongoing semaglutide syringe dosage adjustments.

Ivim Health has partnered specifically with Klarna. Their GLP-1 weight loss program allows patients to start treatment immediately while spreading the cost over time using Klarna Pay-in-4. The process is integrated directly into the Ivim Health checkout experience, meaning you do not need to apply for a separate financing account beforehand.

Fifty 410 is a GLP-1 focused telehealth provider that accepts multiple payment methods including buy now, pay later options. Their programs typically include medication, provider consultations, and ongoing support. WeightCare offers semaglutide programs at competitive price points and also supports flexible payment arrangements for patients who need them.

Providers worth comparing even without BNPL

Not every semaglutide provider offers BNPL, but they may still be worth considering for their pricing alone. Olympia Pharmacy is a well-known compounding pharmacy that works with many telehealth platforms, and their pricing is often competitive enough that the total monthly cost falls within easy Afterpay Pay-in-4 range even if you need to use a third-party checkout for the BNPL portion. Similarly, Empower Pharmacy supplies compounded semaglutide to a wide network of telehealth providers, and the per-vial pricing can work out to a lower per-dose cost when you understand the compounded semaglutide dose chart and how many weeks of treatment each vial provides.

The point is this: do not limit your provider search only to those with Afterpay integration. Find the best provider for your medical needs and budget first. Then figure out the payment logistics. A provider with excellent medical care, competitive pricing, and no Afterpay integration may still be cheaper than a provider with Afterpay integration but higher base prices.

How to check if your provider accepts Afterpay

If your current telehealth provider is not listed above, there are a few ways to find out if they accept buy now, pay later payments. First, check the provider website footer or FAQ section. Most providers that accept Afterpay, Klarna, or Affirm will display the logos prominently. Second, you can search directly on the Afterpay or Klarna websites for the provider name. Both platforms maintain directories of participating merchants. Third, simply contact the provider customer support team and ask. Payment options sometimes change before websites are updated.

Keep in mind that some providers accept BNPL for their consultation fees but not for the medication itself, especially if the medication ships from a separate compounding pharmacy. In that scenario, you might pay the telehealth visit fee through Afterpay but pay for the actual semaglutide directly to the pharmacy. Always clarify exactly what the BNPL option covers before you start treatment. You want to know whether it covers the full cost, including the compounded semaglutide medication, the provider consultation, and any required lab work, or just a portion of the total bill.

Complete semaglutide cost breakdown before you finance

Before deciding how to finance semaglutide, you need to understand exactly what you are financing. The total cost varies dramatically depending on whether you go with brand-name medication, compounded versions, or telehealth subscription programs. Each option has a very different price point, and that price point directly affects which buy now, pay later strategy makes sense for your situation.

Brand-name semaglutide costs

Wegovy, the FDA-approved brand-name semaglutide for weight management, carries a list price of approximately $1,349 per month without insurance. Ozempic, which contains the same active ingredient but is FDA-approved for type 2 diabetes, costs around $935 to $1,000 per month at retail. These are the prices you would pay at a traditional pharmacy without any insurance coverage, savings cards, or discount programs applied.

With commercial insurance and the Novo Nordisk savings card, the cost can drop dramatically. Eligible patients with insurance may pay as little as $25 per month for Wegovy. Self-pay patients who use the NovoCare Pharmacy can access Wegovy pens for $349 per month or Wegovy oral tablets for $199 to $299 per month. There are also introductory pricing offers for new patients at the lower dose levels, bringing costs down to $149 to $199 for the first couple of months.

These numbers matter for financing decisions. At $349 per month through NovoCare self-pay, an Afterpay Pay-in-4 plan would break that into roughly $87.25 every two weeks. Manageable for many budgets. At $1,349 per month without any discounts? That is $337.25 per payment, and most new Afterpay accounts would not even have a high enough limit to cover it. This is where understanding the semaglutide vs tirzepatide cost comparison and exploring all available discounts becomes critical before you commit to a financing plan.

Compounded semaglutide costs

Compounded semaglutide has historically been the more affordable option, typically ranging from $129 to $350 per month depending on the pharmacy, the dosage, and whether the price includes provider consultations. Several telehealth platforms bundle everything together, meaning the monthly fee covers the medication, shipping, provider access, and sometimes even lab work.

Here is a general range of what different telehealth programs charge for compounded semaglutide:

Provider type | Typical monthly cost | What is included |

|---|---|---|

Budget telehealth | $129 to $199 | Medication, basic provider access |

Mid-range telehealth | $199 to $299 | Medication, consultations, some support |

Premium telehealth | $299 to $399 | Medication, labs, coaching, full support |

In-person clinics | $350 to $500+ | In-office visits, medication, monitoring |

An important regulatory note: the FDA ended the semaglutide shortage, which has changed the landscape for compounding pharmacies. Compounded semaglutide is now available only for patients with documented medical needs, such as specific allergies or unique dosing requirements that brand-name versions cannot accommodate. This shift may affect pricing and availability going forward. If you are exploring compounded options, check with providers like Olympia Pharmacy, Empower Pharmacy, or Belmar Pharmacy for current pricing and eligibility requirements.

Other compounding options include Lavender Sky Pharmacy, BPI Labs, and Strive Pharmacy, each with their own pricing structures and formulation options.

The true annual cost of semaglutide treatment

Semaglutide is not a one-month commitment. Most treatment protocols run for six to twelve months at minimum, and many patients continue beyond that. Here is what the annual cost looks like at different price points:

At $150 per month: $1,800 per year

At $249 per month: $2,988 per year

At $349 per month: $4,188 per year

At $1,000+ per month (brand without discounts): $12,000+ per year

Even at the most affordable compounded price, you are looking at close to $2,000 over a year. That is real money. And it is exactly why buy now, pay later options, insurance programs, savings cards, and other financial strategies are so important. The goal is not just to afford the first month. It is to build a sustainable payment approach that keeps semaglutide accessible for the entire duration of your treatment, through the first week on semaglutide, past the initial weight loss phase, and through the long-term maintenance period.

Step by step guide to using Afterpay for semaglutide

Using Afterpay to pay for semaglutide is straightforward once you know the process. Here is exactly how to do it, from setting up your account to completing your first payment.

Step 1: Create your Afterpay account

Download the Afterpay app from the App Store or Google Play, or visit afterpay.com. Sign up with your email address, phone number, and date of birth. Link a debit card or credit card. The entire setup takes about three minutes. Afterpay will run a soft credit inquiry during signup that does not affect your credit score.

Step 2: Choose a semaglutide provider that accepts Afterpay

Navigate to the telehealth provider website. Check their payment options page or look for the Afterpay logo during checkout. If you are not sure whether a provider accepts Afterpay, you can also search within the Afterpay app directory. Providers like Elevate Health display their accepted BNPL options prominently.

Step 3: Complete your medical consultation

Before you reach the payment step, you will need to complete a telehealth consultation. This typically involves filling out a medical questionnaire about your health history, current medications, BMI, and weight management goals. A licensed provider reviews your information and determines whether semaglutide is appropriate for you. Some providers require blood work before prescribing. Others use your questionnaire responses and reported BMI to make a determination. The consultation is usually included in the program cost, though some providers charge a separate consultation fee.

Step 4: Select Afterpay at checkout

Once approved for treatment, you will reach the payment screen. Select Afterpay as your payment method. If this is your first purchase with that merchant, Afterpay may ask you to log in or verify your account. You will see a breakdown of your four payments, including the amount and scheduled dates.

Step 5: Confirm and track your payments

Review the payment schedule. Confirm the purchase. Your first payment processes immediately, and your semaglutide program begins. The remaining three payments will be charged automatically every two weeks. You can track all upcoming payments in the Afterpay app, set up payment reminders, and even make early payments if you prefer to pay down the balance faster.

One important detail: when your next monthly subscription payment comes due, you will go through this process again. Each monthly charge creates a new Afterpay installment plan. So if you are on a $249 per month program, you will have overlapping Afterpay plans running simultaneously after the first month. In month two, you will be paying off the tail end of month one while starting month two payments. This is normal and expected, but make sure you budget for the overlap. By month two, you could have up to six active biweekly payments at once (the last two from month one and all four from month two).

Plan your budget carefully. Know exactly when each payment is due. Track everything in the app. If you are also managing other aspects of your treatment, like figuring out how to reconstitute semaglutide or finding the best injection site, having the financial side automated and predictable frees up mental energy for the clinical side of things.

Other buy now pay later options for semaglutide

Afterpay is not the only game in town. Several other buy now, pay later platforms work for semaglutide purchases, and some may actually be a better fit depending on your financial situation, credit profile, and chosen provider. Here is how the major alternatives compare.

Klarna

Klarna operates similarly to Afterpay with their Pay-in-4 option: four interest-free payments over six weeks. The key difference is Klarna also offers a "Pay in 30" option (pay the full amount within 30 days, no interest) and longer-term financing plans of 6 to 36 months at varying interest rates. Klarna evaluates income, credit history, and outstanding balances when assessing applications.

For semaglutide, Klarna is particularly relevant because several major telehealth providers have partnered directly with them. Ivim Health uses Klarna as their primary BNPL option. Semaglutide Online also integrates Klarna at checkout. If your preferred provider offers Klarna but not Afterpay, the Pay-in-4 experience is nearly identical, the same four interest-free payments over the same six-week period.

Klarna spending limits tend to start slightly higher than Afterpay for many users, though this varies based on individual creditworthiness. For patients purchasing higher-priced semaglutide programs, Klarna extended financing options (beyond Pay-in-4) can provide more breathing room, though those longer plans do carry interest.

Affirm

Affirm takes a different approach. Instead of the standard four-payment split, Affirm offers monthly payment plans ranging from 3 to 60 months. Interest rates range from 0% to 36% APR depending on the merchant, your credit profile, and the repayment term you select. Affirm does conduct a soft credit check during the application that does not affect your score, but if you proceed with a loan, a hard inquiry may be reported.

The advantage of Affirm for semaglutide is flexibility. If you want to finance several months of treatment at once, Affirm can spread the cost over a longer repayment window. For example, financing three months of semaglutide at $249 per month ($747 total) over 12 months at 0% APR would cost you about $62.25 per month. That level of payment smoothing is not possible with Afterpay or Klarna Pay-in-4.

The disadvantage is that 0% APR is not guaranteed. Many Affirm loans carry interest, and rates can be high for borrowers with lower credit scores. Always check the total cost of financing, including interest, before committing. Some providers like Elevate Health offer Affirm alongside Afterpay and Klarna, so you can compare terms at checkout.

CareCredit

CareCredit is specifically designed for healthcare expenses. It functions as a credit card that can be used at participating medical providers, pharmacies, and wellness clinics. The standout feature is promotional financing: many CareCredit transactions qualify for 0% interest if paid within 6, 12, 18, or even 24 months depending on the provider and promotion.

For semaglutide, CareCredit can be a powerful option. If your provider or pharmacy accepts CareCredit, you could finance six months of treatment ($1,500 to $2,400 or more) at 0% interest with a promotional period. Several weight loss clinics and pharmacies accept CareCredit, and you can use the card at participating pharmacy locations to pay for GLP-1 prescriptions, vitamins, and related purchases.

The critical warning with CareCredit: if you do not pay off the full balance within the promotional period, you get charged deferred interest on the entire original amount, not just the remaining balance. The standard CareCredit APR after the promotional period is often 26.99% or higher. That can turn an affordable payment plan into a very expensive one if you are not disciplined about paying it off on time. Plan your payments carefully, and make sure you can clear the balance before the promotion expires.

BNPL comparison table

Platform | Payment structure | Interest | Credit check | Best for |

|---|---|---|---|---|

Afterpay | 4 payments over 6 weeks | 0% (Pay-in-4) | Soft check only | Monthly semaglutide payments under $500 |

Klarna | 4 payments over 6 weeks, or extended | 0% (Pay-in-4), varies for extended | Soft check | Providers that partner with Klarna directly |

Affirm | 3 to 60 months | 0% to 36% APR | Soft check (hard if approved) | Financing multiple months at once |

CareCredit | 6 to 24 months promotional | 0% promotional, 26.99% after | Hard credit check | Larger balances with promotional 0% periods |

Each platform has trade-offs. Afterpay and Klarna are simplest for ongoing monthly semaglutide payments. Affirm works best when you want to finance a larger chunk of treatment upfront. CareCredit is ideal if you qualify for a long promotional period and are confident you can pay it off. The best choice depends entirely on your financial situation, your weight loss timeline, and which platforms your provider accepts.

Insurance coverage and savings programs for semaglutide

Buy now, pay later is one piece of the affordability puzzle. But before you finance the full cost, it is worth exploring whether insurance, manufacturer savings programs, or patient assistance can reduce the amount you need to finance in the first place. Even a partial discount changes the math significantly.

Insurance coverage landscape

Insurance coverage for semaglutide depends on three things: your insurer, your specific plan, and why you are taking the medication. Semaglutide prescribed for type 2 diabetes (as Ozempic) is covered by most commercial insurance plans. Semaglutide prescribed for weight management (as Wegovy) has more inconsistent coverage.

Blue Cross Blue Shield coverage varies by state and plan. Some BCBS plans cover Wegovy with prior authorization and place it at tier 4 (specialty) on their formulary. Others exclude weight loss medications entirely. The Federal Employee Program (FEP) Blue plans have included GLP-1 coverage, with Wegovy and Zepbound placed at various formulary tiers depending on the specific FEP plan. However, some BCBS state plans have announced they will stop covering GLP-1 medications for weight loss, continuing coverage only for diabetes. You can learn more in our Blue Cross Blue Shield GLP-1 coverage guide.

United Healthcare and Aetna both offer coverage in many plans, but almost always with prior authorization requirements. You typically need to demonstrate a BMI of 30 or higher (or 27 with a weight-related comorbidity), show that you have tried other weight management approaches, and sometimes prove that you have been on a GLP-1 for a specific period with documented results. Our guide on BMI requirements for GLP-1 covers the qualification thresholds in detail.

Medicare has begun expanding coverage for select GLP-1 medications for obesity, with monthly copays expected around $50 for qualifying beneficiaries. This is a significant shift from the historical exclusion of weight loss drugs from Medicare coverage.

If your insurance does cover semaglutide, your out-of-pocket cost could drop to $25 to $150 per month with the right savings card stacked on top. At those prices, you may not need buy now, pay later at all. If insurance denies coverage, check out our guide on what to say when requesting GLP-1 options for tips on appealing denials and navigating the prior authorization process.

Novo Nordisk savings cards and programs

Novo Nordisk, the manufacturer of Wegovy and Ozempic, offers several savings programs that can dramatically reduce your costs:

Wegovy Savings Card (commercially insured patients): Eligible patients with commercial insurance can pay as little as $25 per month, with the savings card covering up to $100 per one-month prescription. This applies to all Wegovy pen strengths (0.25 mg, 0.5 mg, 1 mg, 1.7 mg, and 2.4 mg) and tablet formulations.

NovoCare Pharmacy self-pay pricing: Patients without insurance can purchase directly through the NovoCare Pharmacy at $349 per month for Wegovy pens or $199 to $299 per month for Wegovy pills. These prices are significantly lower than retail pharmacy pricing.

Introductory offers: New patients can sometimes access lower-dose Wegovy at reduced introductory prices. Recent promotions have offered the 0.25 mg and 0.5 mg starting doses at $199 per fill, and the 1.5 mg and 4 mg doses at $149 to $199 per fill. These introductory prices are time-limited and apply only to initial fills.

Patient Assistance Program: For low-income patients, Novo Nordisk offers a Patient Assistance Program that may provide medication at no cost. Eligibility typically requires household income below 400% of the Federal Poverty Level and inadequate insurance coverage. The application process requires documentation of income and insurance status.

Accessing the Wegovy savings offer is simple. You can text SAVE to 83757 to receive a digital savings card, or visit the NovoCare website to check eligibility. These programs can be combined with BNPL for whatever remaining balance you owe, creating a layered savings strategy that brings total out-of-pocket costs to their lowest possible point.

Stacking savings: insurance plus savings card plus BNPL

The most cost-effective approach combines all available resources. Here is an example of how stacking works:

Wegovy list price: ~$1,349 per month

After insurance coverage: ~$150 copay

After Novo Nordisk savings card ($100 off): ~$50 per month

Paid via Afterpay: four payments of ~$12.50 every two weeks

That final number, $12.50 every two weeks, is a fraction of where you started. Not every patient will qualify for all three layers, but even two out of three can make a dramatic difference. If insurance is not an option, the NovoCare self-pay price of $349 per month split via Afterpay comes to about $87.25 per payment. Still much more manageable than $1,349 all at once.

For patients exploring oral semaglutide drops or sublingual semaglutide as alternatives to injections, the same financial strategies apply. The cost structure may differ slightly depending on the formulation, but the approach of layering insurance, savings programs, and BNPL remains the most effective way to minimize what you pay out of pocket.

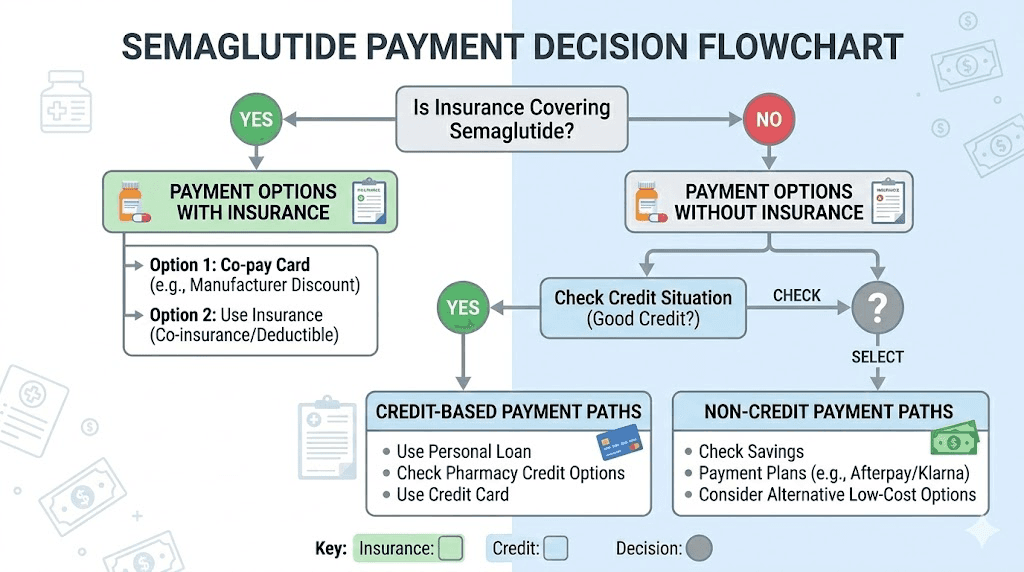

How to choose the right payment option for your situation

The right financing strategy depends on your specific circumstances. A person with good insurance and a manufacturer savings card has very different needs than someone paying entirely out of pocket. Here are five common scenarios and the recommended payment approach for each.

Scenario 1: You have commercial insurance that covers semaglutide

If your insurance covers Wegovy or Ozempic and your copay is under $200 per month, your best move is to apply for the Novo Nordisk savings card first. This can reduce your copay to as little as $25. At that price point, buy now, pay later is unnecessary for most budgets. If your copay is between $100 and $200 even after the savings card, Afterpay Pay-in-4 is a simple way to spread that cost into biweekly chunks without any interest.

Scenario 2: Insurance denied your coverage

Denials happen frequently. If you have been denied, first consider appealing. Insurance companies sometimes approve coverage on appeal, especially with additional documentation from your provider. While you wait for the appeal, look into the NovoCare Pharmacy self-pay pricing at $199 to $349 per month. This is low enough for Afterpay Pay-in-4 to work comfortably. You could also explore compounded semaglutide through telehealth providers that accept BNPL, as long as you qualify for compounded versions under current regulations. If the denial stands and you need longer-term financing, Affirm or CareCredit may offer better terms than Afterpay for larger balances.

Scenario 3: No insurance, paying entirely out of pocket

This is where strategic planning matters most. Start by checking eligibility for the Novo Nordisk Patient Assistance Program. If you do not qualify, compare the NovoCare self-pay price against compounded semaglutide pricing from telehealth providers. Then pick the BNPL option that matches your provider:

Provider accepts Afterpay: Use Pay-in-4 for monthly payments

Provider accepts Klarna: Same approach, four interest-free payments

Want to finance 3+ months at once: Consider Affirm for monthly installments

Provider accepts CareCredit: Take advantage of 0% promotional periods

Use the peptide cost calculator at SeekPeptides to estimate your total treatment cost and plan your financing accordingly. Knowing the full financial picture upfront, including how many months of treatment to expect based on your before and after semaglutide goals, helps you choose between short-term BNPL cycling and longer-term financing.

Scenario 4: You want semaglutide but have limited or bad credit

Afterpay is your friendliest option here. The soft credit check is minimal, and approval rates are generally higher than traditional credit products. Klarna Pay-in-4 is similarly accessible. Avoid Affirm and CareCredit if your credit is poor, as Affirm may charge very high interest rates (up to 36% APR) for lower credit profiles, and CareCredit requires a harder credit pull with a higher approval threshold.

Start with small Afterpay purchases to build your account history and increase your spending limit. Even if your initial limit is only $150, some budget telehealth programs fall within that range. As your limit increases with on-time payments, you will have access to higher-priced programs.

Scenario 5: You are switching from another GLP-1 or weight loss medication

If you are transitioning to semaglutide from another treatment, like phentermine or tirzepatide, your financing needs may shift. You might already have a CareCredit account or an active BNPL relationship from your previous treatment. If so, stick with what is working. If you are coming from a medication that insurance covered but semaglutide is not covered, the cost jump can be significant. In that case, take time to explore all the options above before committing. The semaglutide to tirzepatide transition guide can also help if you are weighing your options in the other direction.

Making semaglutide affordable without BNPL

Buy now, pay later is not the only way to reduce semaglutide costs. Some approaches eliminate the need for financing altogether. Others work alongside BNPL to bring the financed amount even lower. Here are strategies that do not involve taking on any payment plan debt.

GoodRx and pharmacy discount cards

GoodRx and similar prescription discount platforms negotiate lower prices with pharmacies. While these discounts are more impactful for brand-name medications at retail pharmacies, they can sometimes reduce costs by 10% to 40% depending on the pharmacy and current pricing. GoodRx has also launched a weight loss telemedicine subscription that combines provider consultations with discounted medication access. The platform introduced pricing of $199 per month for Ozempic and Wegovy through their own pharmacy partnerships.

These discount cards cannot be combined with insurance but can be used as an alternative when paying out of pocket. For patients using compounded semaglutide through telehealth, GoodRx discounts generally do not apply since the medication comes from a specialty compounding pharmacy rather than a retail chain.

Choosing the right formulation and dose

Cost varies by formulation. Injectable semaglutide, oral semaglutide drops, and sublingual semaglutide can all have different price points. Ask your provider about all available formulations and their respective costs. Sometimes switching from injections to an oral form (or vice versa) can save money without compromising effectiveness.

Dose optimization also matters. Working closely with your provider to find the lowest effective dose can reduce costs. Some patients achieve strong results at 1 mg per week rather than the full 2.4 mg, and lower doses generally cost less. Using a semaglutide dosage calculator can help you understand the relationship between dose, vial size, and number of doses per vial, especially for compounded versions.

Some patients ask about splitting semaglutide doses as a cost-reduction strategy. While dose splitting is a conversation to have with your provider (not a decision to make independently), it is worth discussing whether a modified dosing schedule could extend your supply and reduce monthly costs.

Compounded semaglutide blends

Several compounding pharmacies offer semaglutide combined with other ingredients, such as semaglutide with glycine, semaglutide glycine B12 blends, semaglutide with methylcobalamin, semaglutide with niacinamide, or semaglutide with L-carnitine. These blends sometimes offer cost advantages because you are getting multiple active ingredients in a single product rather than purchasing them separately. The added ingredients may also support your treatment outcomes, potentially reducing the total duration and therefore total cost of your weight management program.

Timing your start strategically

If cost is a major concern, timing can help. Many telehealth providers run promotional pricing for new patients, seasonal discounts, or introductory rates for the first month or first three months. Starting during a promotion and then transitioning to a BNPL-funded regular rate can save hundreds over the course of treatment. Follow your preferred providers on social media and sign up for email lists to catch these offers when they appear.

Similarly, if you have a health savings account (HSA) or flexible spending account (FSA), semaglutide prescribed by a provider typically qualifies as an eligible medical expense. Using pre-tax dollars from an HSA or FSA effectively gives you a discount equal to your marginal tax rate, which could be 22% to 37% for many people. That is a significant savings that stacks with any other discount or financing strategy.

Employer wellness programs and weight management benefits

Some employers now offer weight management benefits that can offset semaglutide costs. These programs vary widely. Some provide a flat monthly stipend for weight management medications. Others cover a percentage of the cost through a wellness reimbursement account. A few progressive employers include GLP-1 medications as a covered pharmacy benefit even when the standard insurance plan excludes them.

Check with your human resources department or benefits administrator. Ask specifically about weight management medication coverage, wellness stipends, and any partnerships with telehealth providers that might offer discounted rates. Even a $50 or $100 monthly reimbursement from an employer wellness program can dramatically change the math when combined with BNPL financing for the remainder. Every dollar you reduce from the base cost is a dollar you do not need to finance through Afterpay or any other platform.

For patients specifically interested in the fat loss applications of peptides beyond semaglutide, the peptides for fat loss resource at SeekPeptides covers a broader range of options, some of which may be more affordable depending on your goals and provider.

Risks and considerations with buy now pay later for medications

BNPL services make semaglutide more accessible. That is a genuine benefit. But financing ongoing medication comes with risks that do not apply to financing a pair of shoes or a new gadget. Here are the considerations you should weigh before committing to a BNPL strategy for semaglutide.

The compounding debt trap

With Afterpay, each monthly purchase creates a new four-payment cycle. By month two, you have overlapping payment schedules. By month three, you could have up to eight active Afterpay payments at various stages. The math works out fine if you can afford the total monthly medication cost. But the illusion of smaller individual payments can mask the reality that you are spending the same amount of money, just in a different pattern.

Let us make this concrete with numbers. Suppose you are on a $249 per month semaglutide program. In month one, you have four Afterpay payments of $62.25 each. Manageable. In month two, you start a new Afterpay plan while still paying off the last two installments from month one. You now have six active payments across two plans. By month three, you could have payments from three different Afterpay plans active simultaneously. The total biweekly outflow has not increased beyond your monthly medication cost, but the psychological and logistical complexity has multiplied. Missing even one payment creates a cascading problem across your overlapping plans.

If your financial situation changes, if unexpected expenses arise, if you lose income, those overlapping obligations do not pause. Missed payments trigger fees, account freezes, and potential collections activity. This is especially important to consider because semaglutide treatment is not optional in the same way a retail purchase is. Stopping treatment abruptly can have health consequences. Understanding what happens if you stop semaglutide cold turkey versus restarting after a break can help you plan for worst-case scenarios.

Interest costs with longer-term financing

Afterpay Pay-in-4 and Klarna Pay-in-4 are interest-free. That is their primary appeal. But the moment you step outside those short-term products, whether it is Afterpay Pay Monthly, Klarna extended financing, Affirm loans, or CareCredit after a promotional period, interest enters the picture. And it can be steep.

A $3,000 annual semaglutide cost financed at 25% APR over 12 months would cost you approximately $3,420, an extra $420 in interest alone. At 35% APR, the total jumps to roughly $3,600. That is money that could have gone toward additional months of treatment, healthier food, a gym membership, or any of the lifestyle factors that support semaglutide diet planning and long-term weight management success.

If you must use interest-bearing financing, calculate the total repayment cost before committing. Compare that total against other options. Sometimes paying a higher monthly amount on a shorter, interest-free plan is cheaper in the long run than stretching payments out over a longer, interest-bearing period.

No built-in consumer protections for medication disputes

When you buy a physical product with Afterpay and it does not arrive, you can file a dispute. Medication purchases are trickier. If you receive your semaglutide but experience side effects like bloating, constipation, fatigue, or dizziness and decide to stop treatment, you are still on the hook for payments already initiated. BNPL platforms generally do not offer refunds for services rendered or medications received.

Before purchasing, understand the provider refund and cancellation policy. Some telehealth programs offer month-to-month subscriptions that you can cancel anytime. Others require multi-month commitments. If you are financing a multi-month commitment through BNPL and discontinue early, you still owe the full amount. Match your BNPL strategy to your provider contract terms, and avoid financing more treatment upfront than you are comfortable paying for even if you stop early.

Impact on other financial goals

Recurring BNPL payments reduce your available cash flow, which can affect your ability to save, invest, or handle emergencies. Some mortgage lenders and financial institutions have started factoring BNPL obligations into debt-to-income ratio calculations, which could affect your ability to qualify for other credit products.

This does not mean you should not use BNPL for semaglutide. It means you should consider the broader financial picture. If semaglutide is a priority and BNPL makes it accessible, that is a valid and potentially health-positive choice. But go in with eyes open. Know exactly what you are committing to, for how long, and how it fits within your overall budget.

Regulatory and availability changes

The semaglutide market has shifted significantly. The FDA ended the semaglutide shortage, which has restricted the availability of compounded versions to patients with documented medical needs. This means the affordable compounded semaglutide that many patients financed through BNPL may no longer be available to everyone. If you are currently financing compounded semaglutide and it becomes unavailable to you, you will need to transition to brand-name medication, likely at a higher price point.

This creates a financing risk. You may budget for $199 per month compounded semaglutide financed through Afterpay, only to find that you need to switch to $349 per month NovoCare self-pay pricing. That jump changes your biweekly Afterpay payments from about $50 to about $87. Make sure your budget can absorb potential price increases, and have a backup financing plan ready in case the cost landscape shifts during your treatment.

For patients concerned about long-term costs, understanding the full treatment timeline is important. Factors like when side effects typically appear, how quickly appetite suppression kicks in, and how long GLP-1 takes to start working can help you set realistic expectations for how many months of financing you will actually need.

Frequently asked questions

Can you use Afterpay at a pharmacy for semaglutide?

Most traditional retail pharmacies (CVS, Walgreens, Rite Aid) do not accept Afterpay directly. However, CenterWell Pharmacy does accept Afterpay for prescription purchases. The more common way to use Afterpay for semaglutide is through telehealth providers that integrate BNPL into their checkout process. These providers typically handle the prescription, medication sourcing, and delivery as a bundled service, and you pay the total through Afterpay at their online checkout.

Does Afterpay affect your credit score?

Standard Afterpay Pay-in-4 uses a soft credit check that does not affect your credit score. Making on-time payments does not build your credit either, as Afterpay does not report positive payment history to credit bureaus in most cases. However, if your account goes to collections due to missed payments, that can negatively impact your score. The Afterpay Pay Monthly product (for purchases over $400) may involve a more detailed credit assessment.

What happens if you cannot afford your next semaglutide payment?

If you miss an Afterpay payment, you will be charged a late fee of up to $8, and your account will be frozen until the overdue amount is paid. If you realize in advance that you cannot make a payment, the best approach is to pay off the remaining balance as quickly as possible and pause your semaglutide subscription until you are financially ready to resume. Stopping and restarting semaglutide is medically manageable with proper guidance from your provider, so taking a financial break is far better than accumulating debt you cannot service.

Is it safe to buy semaglutide from providers that offer Afterpay?

The payment method itself has no bearing on the quality or safety of the medication. What matters is the legitimacy of the provider. Look for telehealth platforms that use licensed providers, source medication from licensed pharmacies, and have verifiable reviews and credentials. Whether you pay cash, use insurance, or use Afterpay, the medication quality depends entirely on the provider and pharmacy, not the payment platform.

Learn how to give a semaglutide injection with a syringe and how to reconstitute 5mg semaglutide from trusted educational resources before starting treatment, regardless of how you pay for it. Knowing about what color semaglutide should be and what to do if semaglutide appears red can help you verify that you have received a legitimate product.

Can you use Afterpay for tirzepatide as well?

Yes. The same BNPL platforms that work for semaglutide also work for tirzepatide purchases from participating providers. If you are considering tirzepatide as an alternative, check out the tirzepatide Afterpay complete guide for provider-specific details and the affordable tirzepatide resource for cost-reduction strategies specific to that medication.

How much does semaglutide cost per month with Afterpay?

Afterpay does not change the total cost of semaglutide. It changes how you pay. If your semaglutide program costs $249 per month, you still pay $249 total, just split into four payments of $62.25 every two weeks. The benefit is cash flow management, not a discount. To actually reduce the cost, combine BNPL with insurance coverage, savings cards, or patient assistance programs as described in this guide.

What if my semaglutide arrives damaged or expired?

Contact the provider immediately. Most legitimate telehealth providers will replace damaged or expired medication. Your Afterpay payment obligation does not change based on a product issue, but you can dispute the charge through Afterpay if the merchant refuses to resolve the problem. Knowing about semaglutide shelf life, how long semaglutide lasts in the fridge, the 28-day expiration question, and whether compounded semaglutide expires helps you evaluate product quality when it arrives.

Should you finance the entire semaglutide treatment upfront or month by month?

Month by month is generally safer. Financing the entire treatment upfront through Affirm or CareCredit means committing to a large amount before you know how your body will respond. You might have a great experience in the first week and continue for months. Or you might experience significant side effects and need to switch approaches. Paying month by month with Afterpay or Klarna gives you flexibility to pause or stop without being locked into a large financing commitment.

Can you use multiple BNPL services at the same time?

Technically, yes. You could use Afterpay for one month, Klarna for the next, and Affirm for a separate purchase, all running concurrently. But managing multiple payment schedules across multiple platforms increases complexity and the risk of missed payments. Stick to one platform if possible. The administrative simplicity is worth more than any marginal advantage of platform-hopping.

Does using BNPL for semaglutide affect health insurance applications?

No. BNPL payment history is not part of medical underwriting. Health insurance applications do not ask about or have access to your Afterpay, Klarna, or Affirm accounts. Your choice of payment method for semaglutide has no impact on current or future health insurance eligibility or pricing.

What is the cheapest way to get semaglutide right now?

The cheapest path depends on your insurance status. With commercial insurance plus the Novo Nordisk savings card, you may pay as little as $25 per month. Without insurance, the NovoCare Pharmacy self-pay price of $199 per month for Wegovy pills is competitive. Compounded semaglutide from budget telehealth providers can sometimes be found for $129 to $150 per month, though availability is more limited following the FDA shortage resolution. Use every tool available, including insurance, savings cards, pharmacy discounts, and BNPL, to build the most affordable access possible. The peptide cost calculator can help you model different scenarios.

Is semaglutide worth the cost?

Clinical studies show average weight loss of 12% to 17% of body weight over 68 weeks with semaglutide. For a 250-pound person, that translates to 30 to 42 pounds of weight loss. Beyond weight, semaglutide has shown benefits for cardiovascular health, blood sugar regulation, and overall metabolic function. Whether the cost is "worth it" depends on your personal health goals, financial situation, and available alternatives. Reading before and after semaglutide results and understanding realistic weight loss timelines can help you evaluate the return on investment for your specific situation.

What about combining semaglutide with other supplements for better results?

Some patients explore combining semaglutide with other compounds to enhance results. Options like berberine and semaglutide together or phentermine and semaglutide together are topics patients frequently ask about. While these combinations may affect your total treatment cost, they should only be pursued under provider supervision. Better results could mean a shorter treatment duration, which would actually reduce your total financing needs.

How do I handle semaglutide storage and travel while on a payment plan?

Your payment plan does not change storage requirements. Semaglutide needs proper refrigeration. If your semaglutide arrives hot or gets warm during shipping, contact your provider about replacement regardless of how you paid. When traveling with semaglutide, use an insulated travel case and plan ahead. Understanding how long compounded semaglutide can be unrefrigerated and how long semaglutide remains potent helps you avoid wasting medication you have already paid for (or are still paying for through BNPL).

What if I experience side effects after paying through Afterpay?

Side effects do not entitle you to an Afterpay refund if the provider delivered the medication as ordered. Common side effects include bloating, constipation, fatigue, dizziness, burping, and insomnia. Most subside within the first few weeks. If side effects are severe enough that you want to stop treatment, cancel your subscription to prevent future charges, but expect to pay for medication already received. Learn about the best foods to eat on semaglutide and foods to avoid to minimize digestive side effects, which can help you stay on track and get full value from each paid month.

Can semaglutide affect other areas of health while I am paying for treatment?

Yes. Beyond weight loss, semaglutide can affect several aspects of health. Some patients report changes in sex drive, menstrual cycles, and energy levels. There are also less common concerns like kidney stones and blood clots. Discuss these possibilities with your provider before starting. Being informed about the full range of effects helps you make a better decision about how much treatment to finance and how long to continue.

What if I hit a weight loss plateau while still making payments?

Plateaus are common. A semaglutide plateau does not mean the medication stopped working. It often means your body is adapting and your provider may need to adjust your dose. If you are in the first four weeks with no weight loss, patience is usually the answer. Your provider can evaluate whether a dosage adjustment is needed. Strategies like pairing semaglutide with a proper diet plan, understanding the complete food list for semaglutide, and exploring whether you can lose weight without exercise on semaglutide can all help you break through.

What dosage-related questions should I understand before financing treatment?

Understanding dosage is critical because it directly affects cost. Knowing how many units is 0.25 mg, how many units is 1 mg, how many units is 2.5 mg, and how many units is 2.4 mg helps you calculate exactly how many doses you get per vial. Use the semaglutide units to mg conversion to verify your dosing and the 5mg reconstitution chart or 10mg reconstitution chart to understand how many weeks of treatment each vial provides. More doses per vial means lower cost per dose, which means you finance less overall. Questions about whether 20 units is too much or 50 units is a lot are worth discussing with your provider to make sure you are on the most cost-effective dose for your needs.

What about injection technique and medication handling?

Proper technique ensures you get the full benefit of every dose you pay for. Learn about the best injection site for semaglutide, the best time of day to take it, and the correct injection technique with a syringe. If you accidentally inject into muscle instead of subcutaneous tissue, absorption may be affected. Wasted medication is wasted money, especially when every dose is being financed. Similarly, if you accidentally leave semaglutide out overnight or accidentally use expired medication, understand the implications before discarding or using it.

Are there GLP-1 specific resources that can help me decide?

Absolutely. Understanding how semaglutide compares to other GLP-1 treatments helps you make a more informed financial commitment. Explore whether GLP-1 is the same as Ozempic, learn about GLP-1 fat loss treatment broadly, and review the semaglutide vs tirzepatide dosage comparison and side effect comparison. These resources help you choose the right medication before you commit to financing it. You should also understand GLP-1 injection site reactions, the best GLP-1 injection sites for weight loss, how to inject GLP-1, where to inject GLP-1, and the best time to take a GLP-1 shot. For dietary support during treatment, explore protein shakes for GLP-1 and GLP-1 breakfast ideas to maximize your results and get the best value from every financed month. If you experience fatigue, our GLP-1 fatigue guide can help, and understanding the GLP-1 lawsuit news keeps you informed about the broader regulatory landscape. For patients exploring fat loss peptides beyond GLP-1 medications, the peptides for fat loss resource and the peptide calculator and peptide reconstitution calculator at SeekPeptides provide additional tools for understanding costs and protocols.

What should I know about surgery and semaglutide treatment timing?

If you are planning a medical procedure, know that semaglutide may need to be paused. Our guide on when to resume semaglutide after surgery covers the timing details. If you pause treatment, you may also want to pause your BNPL payments by canceling your subscription. When ready to restart, you pick up both your prescription and your financing where you left off.

External resources

Afterpay official guide: How it works - Official overview of the Pay-in-4 structure, fees, and terms

NovoCare Wegovy savings card eligibility - Check eligibility for manufacturer savings and patient assistance programs

CareCredit weight loss financing - Healthcare-specific credit card with promotional 0% interest periods for qualifying purchases

GoodRx Wegovy pricing - Current pricing, coupons, and savings tips for brand-name semaglutide

CFPB buy now pay later guide - Consumer Financial Protection Bureau overview of BNPL consumer rights and risks

Navigating semaglutide costs does not have to be overwhelming. The tools exist. Afterpay, Klarna, Affirm, CareCredit, manufacturer savings cards, insurance appeals, and patient assistance programs all work toward the same goal: making effective treatment accessible to more people. The key is knowing which tools apply to your situation and how to combine them strategically.

SeekPeptides members access detailed protocol guides, dosage calculators, provider comparisons, and community support that can help you navigate every stage of semaglutide treatment, from choosing the right provider and understanding reconstitution to optimizing your dose and managing side effects. When cost is a concern, having access to comprehensive, trustworthy information helps you make smarter decisions about both your health and your finances. Explore SeekPeptides to learn more about membership benefits and how they support your entire peptide journey.

In case I do not see you, good afternoon, good evening, and good night.