Feb 23, 2026

You have done the research. You have talked to your provider. You know tirzepatide is the right choice for your weight loss goals. Then you see the price tag. Three hundred dollars a month. Five hundred. Sometimes more. And suddenly the medication that could change your life feels completely out of reach.

This is where most people get stuck.

They scroll through telehealth websites, compare provider after provider, and wonder if there is some secret discount they are missing. Some give up entirely. Others put the medication on a credit card with a 24% interest rate and hope for the best. Neither option is ideal, and both leave money on the table that could be saved with the right payment strategy.

But here is what most guides about affordable tirzepatide never tell you. Buy now, pay later services like Afterpay, Klarna, CareCredit, and Cherry have quietly entered the weight loss medication space. These platforms let you split your tirzepatide costs into smaller, more manageable payments, often with zero interest if you pay on time. The catch? Not every provider accepts every payment method, the fee structures vary wildly, and some options that look free actually cost you more than a traditional credit card would. This guide breaks down exactly how each payment option for tirzepatide works, which providers accept them, what the hidden fees look like, and how to choose the right financing strategy for your specific situation. No vague advice. No generic recommendations. Just the actual numbers and comparisons you need to make an informed decision about paying for your medication.

How Afterpay works for tirzepatide purchases

Afterpay follows a straightforward model. You make a purchase, and the total gets divided into four equal payments spread over six weeks. The first payment happens at checkout. The remaining three payments are automatically charged to your debit or credit card every two weeks after that. No interest. No fees, as long as you pay on time.

For tirzepatide specifically, this means a $400 monthly supply breaks down to $100 every two weeks. A $300 compounded option splits into $75 installments. The math is simple and the appeal is obvious.

But there are important limitations to understand before you count on Afterpay for your tirzepatide medication. Afterpay caps most purchases at around $2,000, which sounds like plenty for a monthly supply but can become restrictive if you are trying to prepay multiple months at a discount. The platform also runs a soft credit check on your first purchase. It will not show up on your credit report, but Afterpay can and does decline new customers based on their internal risk assessment.

The approval process takes seconds. You download the Afterpay app or select it at checkout, enter your payment details, and get an instant decision. If approved, your first installment processes immediately and your order ships. Simple. Fast. No lengthy application process like traditional medical financing.

At SeekPeptides, we see people navigate these payment decisions every day, and the biggest mistake is choosing a payment method before understanding the full landscape of options. Getting the financing right can save hundreds of dollars annually.

One critical detail many people miss. Afterpay is technically a point-of-sale financing product, not a healthcare financing tool. This means the provider you are purchasing from must specifically integrate Afterpay into their checkout system. You cannot retroactively apply Afterpay to a purchase made through a provider that does not offer it. So the first question is not "Can I use Afterpay?" but rather "Does my tirzepatide provider accept Afterpay?"

We will cover which providers accept Afterpay and other BNPL options in detail later in this guide. First, you need to understand all your options so you can compare them properly.

Every buy now, pay later option for tirzepatide compared

Afterpay is not the only game in town. Five major BNPL and financing platforms have established themselves in the weight loss medication space, and each one works differently. Understanding these differences can save you hundreds of dollars over the course of your tirzepatide treatment.

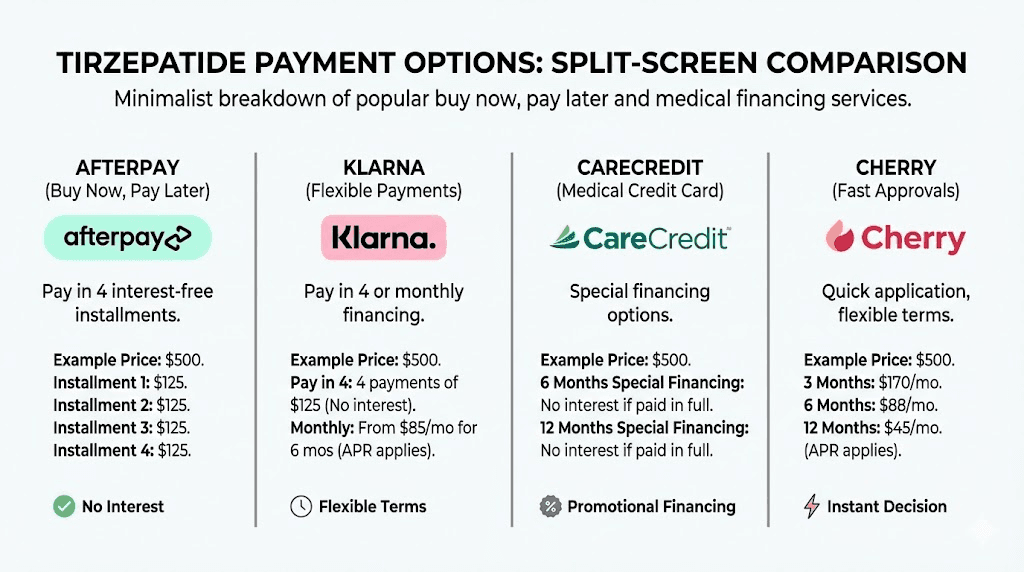

Afterpay

Afterpay splits purchases into four equal payments over six weeks with zero interest. No credit check appears on your report. The spending limit typically caps at $2,000, though this can increase over time with consistent on-time payments. Late fees apply if you miss a payment, currently capped at 25% of the order value or $68, whichever is less. Afterpay pauses your account after a missed payment, meaning you cannot make new purchases until you catch up.

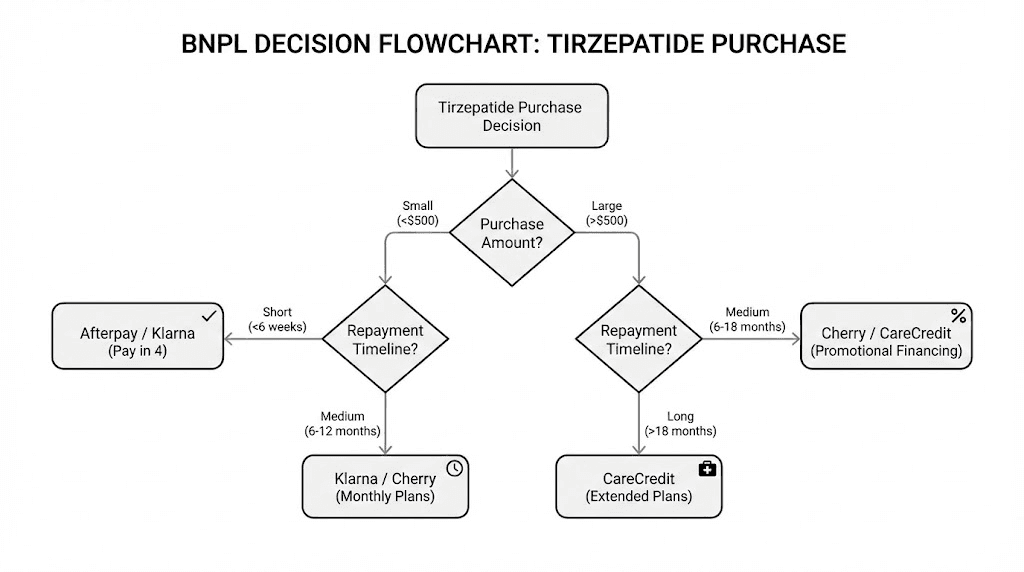

Best for: Monthly tirzepatide purchases under $500 when you want short-term, interest-free installments with no formal credit application.

Klarna

Klarna offers three payment structures. "Pay in 4" works like Afterpay, splitting the purchase into four interest-free installments over six weeks. "Pay in 30" gives you a full 30 days to pay with no interest. "Monthly financing" extends to 6-36 months but charges interest rates between 7.99% and 33.99% APR depending on your creditworthiness. Klarna performs a soft credit check for Pay in 4 and a hard credit check for monthly financing.

Several telehealth providers have specifically partnered with Klarna. Ivim Health, for example, offers Klarna financing on their compounded tirzepatide programs, making it one of the more accessible BNPL options in this space.

Best for: People who want more flexibility than Afterpay provides, especially the 30-day pay option for those who just need to align their medication purchase with their next paycheck.

CareCredit

CareCredit operates as a dedicated healthcare credit card issued by Synchrony Bank. This is fundamentally different from Afterpay and Klarna. You apply for a credit line (up to $25,000), undergo a hard credit check, and receive a card you can use at any of 270,000+ participating providers. The promotional offers include 0% interest for 6, 12, 18, or 24 months on purchases over $200.

Here is the catch that trips people up. CareCredit uses deferred interest on its promotional plans. If you do not pay off the full balance before the promotional period ends, you get charged interest retroactively from the original purchase date at the standard APR of up to 32.99%. On a $3,600 annual tirzepatide expense, that retroactive interest can exceed $1,000.

CareCredit also offers reduced APR fixed payment plans: 17.90% for 24 months, 18.90% for 36 months, 19.90% for 48 months, and 20.90% for 60 months. These are not promotional rates. Interest accrues from day one.

Best for: People with good credit who are disciplined about paying off promotional balances before the deadline, and who want to finance larger purchases like prepaid multi-month tirzepatide treatment plans.

Cherry

Cherry positions itself as a healthcare-first BNPL platform. It offers financing up to $50,000 (far more than other options) with both short-term Pay-in-4 plans and extended repayment up to 60 months. Cherry claims qualifying 0% APR options for some patients, though rates vary based on creditworthiness. No hard credit check for the initial application. Cherry is accepted at medical spas, weight loss clinics, and telehealth providers that specifically integrate it.

Cherry has gained traction in the weight loss medication space specifically because it was designed for healthcare purchases. The approval amounts tend to be higher than consumer BNPL platforms, making it useful for patients who want to lock in multi-month tirzepatide protocols at a discounted rate.

Best for: Larger purchases at medical spas and clinics, especially multi-month treatment packages where higher credit limits are needed.

Affirm

Affirm offers flexible terms from 3 to 60 months with APRs ranging from 0% to 36%. Unlike CareCredit, Affirm uses simple interest rather than deferred interest, meaning you will never face surprise retroactive charges. A soft credit check determines your rate and terms. Affirm shows you the total cost of financing upfront before you commit, including all interest charges.

Affirm has less penetration in the healthcare space than CareCredit or Cherry, but some telehealth providers do accept it. The transparency of simple interest makes it a safer choice for people who might need longer repayment periods for their tirzepatide treatment.

Best for: People who want longer repayment terms with clear, predictable interest charges and no deferred interest traps.

Head-to-head comparison

Feature | Afterpay | Klarna | CareCredit | Cherry | Affirm |

|---|---|---|---|---|---|

Payment structure | 4 payments / 6 weeks | 4 payments, 30 days, or monthly | 6-60 month plans | Pay-in-4 or up to 60 months | 3-60 months |

Interest rate | 0% (if on time) | 0% to 33.99% | 0% promo, then up to 32.99% | 0% to variable | 0% to 36% |

Credit check | Soft (no report impact) | Soft or hard | Hard check | Soft check | Soft check |

Max credit | ~$2,000 | Varies | $25,000 | $50,000 | $17,500 |

Late fees | Up to $68 | Varies by plan | Up to $41 | Varies | No late fees |

Deferred interest | No | No | Yes (promotional plans) | No | No |

Healthcare focus | No | No | Yes | Yes | No |

Best for | Small monthly purchases | Flexible short-term | Large treatment plans | Multi-month packages | Transparent long-term |

The right choice depends entirely on your situation. If you are paying for compounded tirzepatide at $300 per month and just need to split that single payment, Afterpay or Klarna Pay-in-4 makes perfect sense. If you want to lock in a six-month treatment plan at a discounted rate, CareCredit or Cherry gives you the credit limit and repayment timeline to make that work. If you are concerned about hidden fees and want maximum transparency, Affirm eliminates the deferred interest risk entirely.

What tirzepatide actually costs right now

Before choosing a payment method, you need accurate cost data. The price of tirzepatide varies dramatically depending on the source, and these differences matter more than which BNPL platform you use. A $200 per month difference in medication cost dwarfs any interest savings from financing.

Brand-name tirzepatide pricing

Brand-name tirzepatide (sold as Mounjaro for diabetes and Zepbound for weight loss) carries a list price of approximately $1,080 to $1,086 for a 28-day supply. This is the retail price without insurance, and very few people actually pay this amount.

Eli Lilly launched the Zepbound Self Pay Journey Program, offering reduced pricing through LillyDirect. The current self-pay pricing breaks down as follows:

2.5 mg dose: $349 per month

5 mg dose: $499 per month

7.5 mg and 10 mg single-dose vials: $499 per month

12.5 mg and 15 mg: $499 per month through LillyDirect

With commercial insurance and the Eli Lilly Savings Card, qualifying patients can access tirzepatide for as low as $25 per month. This requires non-government insurance that covers the medication. If your insurance covers tirzepatide or its branded versions, the savings card should be your first stop before considering any BNPL option.

Compounded tirzepatide pricing

Compounded tirzepatide costs between $200 and $500 per month depending on the provider, dose, and any added compounds. The most common formulations include tirzepatide with glycine and B12, tirzepatide with niacinamide, and tirzepatide with methylcobalamin.

Important context: compounded medications are not FDA-approved, and the FDA does not verify their safety, quality, or potency. This does not mean they are inherently dangerous, but it does mean you need to choose your provider carefully. Quality varies significantly between compounding pharmacies, and the cheapest option is not always the safest. Read our guide on grey market tirzepatide to understand the risks and how to identify legitimate providers.

Starting in April of this year, Medicare and Medicaid may begin covering GLP-1 medications more broadly, with eligible patients potentially seeing out-of-pocket costs capped at approximately $50 per month. This is a developing situation worth monitoring if you have government insurance.

Telehealth provider pricing breakdown

The real variation lives in the telehealth market. Provider pricing for compounded tirzepatide ranges from around $219 to $700 per month, and the price differences often reflect what is included in the program. Some prices cover medication only. Others bundle consultations, shipping, lab work, and ongoing provider access.

Here is what the current market looks like for popular providers:

Provider | Monthly cost | What is included | BNPL accepted |

|---|---|---|---|

Varies by dose | Medication, consultations, shipping | Check provider | |

$279-$399 | Medication, consultations | Month-to-month | |

Varies | Compounded tirzepatide, pharmacy services | Check provider | |

Varies | Medication, provider access | Check provider | |

Varies | Compounded medication | Check provider | |

Varies | Compounded tirzepatide | Check provider |

The key insight here is that reducing your base cost matters more than financing. If you are paying $500 per month and financing with Afterpay, you are still spending $500. If you switch to a provider charging $300 per month and pay cash, you save $200 with zero financing complexity. Always calculate your total peptide costs before deciding on a payment method.

Also factor in ancillary costs that many people overlook. Consultation fees, shipping charges, lab work requirements, and the cost of supplies like alcohol swabs and syringes all add to the monthly total. Some all-inclusive programs appear expensive at first glance but actually cost less when you account for everything included. Others advertise low medication prices but nickel-and-dime you with add-on fees. Get the complete cost picture before committing to any payment arrangement, and compare apples to apples across providers.

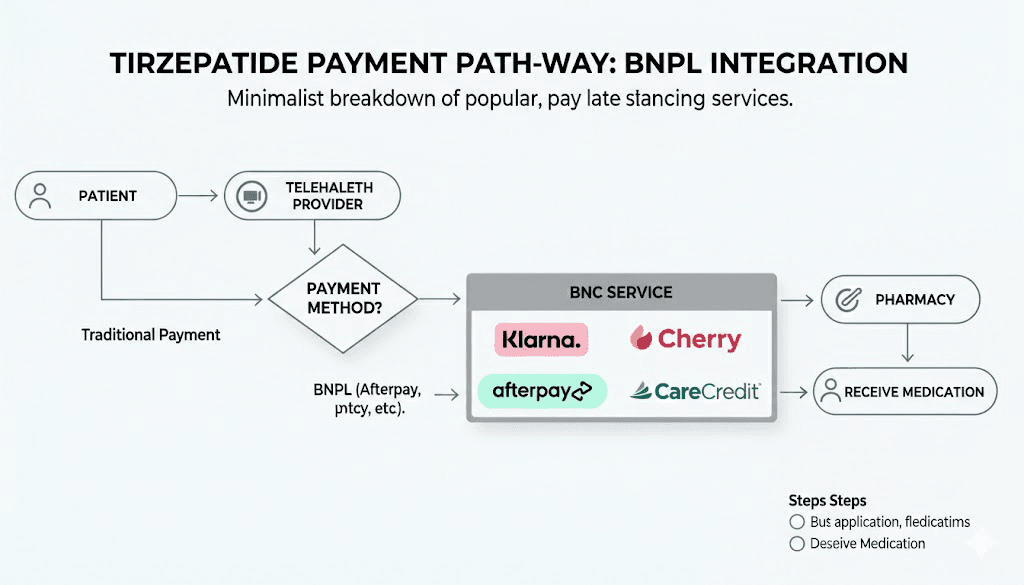

Which providers accept Afterpay and other BNPL for tirzepatide

This is the question everyone asks first, and the answer is more nuanced than a simple list. BNPL acceptance for tirzepatide breaks down into three categories: online telehealth platforms, in-person medical spas and clinics, and compounding pharmacies.

Online telehealth providers

The major telehealth platforms for tirzepatide prescriptions have varying payment integrations. Most operate on monthly subscription models that charge your card automatically. Some have added BNPL options, but availability changes frequently as these partnerships evolve.

Ivim Health specifically advertises Klarna integration, making it one of the more transparent telehealth options for BNPL. Their GLP-1 weight loss program allows you to spread payments through Klarna Pay-in-4 installments. Several smaller telehealth providers have begun integrating Afterpay and Cherry as well, though these integrations tend to be newer and less established.

CenterWell Pharmacy (a Humana-affiliated pharmacy) accepts Afterpay for prescription purchases, allowing four interest-free payments over six weeks. This represents one of the few traditional pharmacy chains embracing BNPL for medications.

When evaluating a telehealth provider, check their checkout page before committing. Look for BNPL logos at the bottom of payment sections. If you do not see your preferred payment method, contact their support team directly. Some providers accept BNPL but do not prominently advertise it.

Medical spas and weight loss clinics

In-person clinics represent the largest category of BNPL acceptance for tirzepatide. Medical spas, weight loss clinics, and aesthetic practices commonly offer CareCredit, Cherry, and increasingly Afterpay or Klarna. This is because these businesses already use BNPL for cosmetic procedures and can easily extend the same payment options to weight loss medications.

Balanced Hormone Health, for example, explicitly offers Afterpay, Klarna, and CareCredit for their tirzepatide programs. Many similar clinics offer comparable flexibility.

The advantage of in-person clinics is direct provider access and often more payment flexibility. The disadvantage is typically higher overall costs compared to online-only telehealth platforms. A clinic charging $600 per month with Afterpay might actually cost you more than an online provider charging $350 with no BNPL option.

Compounding pharmacies

Most compounding pharmacies operate on a cash-pay or insurance model and have been slower to adopt BNPL. Empower Pharmacy, Olympia Pharmacy, and similar large compounders primarily accept standard payment methods.

However, the telehealth providers that partner with these pharmacies sometimes offer BNPL at the point of sale, even though the pharmacy itself does not. The provider handles the BNPL transaction, pays the pharmacy directly, and manages your installment plan. This indirect BNPL access is becoming increasingly common as the market for compounded GLP-1 medications grows.

Hidden fees and traps you need to know about

Every BNPL platform markets itself as free or low-cost. And technically, most of them can be free if you use them perfectly. But nobody talks about what happens when things do not go perfectly. For a medication you will likely take for months or years, understanding the worst-case scenarios is just as important as understanding the best-case ones.

Late payment penalties

Afterpay charges late fees in two increments. The first late fee hits immediately when you miss a payment, and a second fee follows seven days later if the payment remains unpaid. Total late fees are capped at 25% of the order value or $68, whichever is less. On a $400 tirzepatide purchase, that is up to $68 in fees for missing a single payment. Over 12 months of treatment, one missed payment per quarter adds $272 in unnecessary costs.

Klarna Pay-in-4 may charge a late fee of up to $7, which sounds minimal until you realize they can also pause your account and report repeated late payments to credit agencies. The reputational damage and credit score impact can cost far more than the $7 fee.

CareCredit does not charge traditional late fees the way consumer BNPL platforms do. Instead, it charges the standard credit card late fee of up to $41 and, more importantly, a missed payment can void your promotional 0% interest period. One late payment on a $3,000 balance at 32.99% APR means nearly $1,000 in interest charges you were not expecting.

Cherry and Affirm handle late payments differently, with Affirm notably charging no late fees at all. This makes Affirm one of the safer options for people who might occasionally need flexibility with payment timing.

The deferred interest trap

This is the single most important concept in this entire guide, and it applies specifically to CareCredit.

Deferred interest means interest accrues from day one but is not charged to your account as long as you pay off the full balance within the promotional period. If you pay off a $3,600 annual tirzepatide treatment within 18 months at 0%, you pay zero interest. Great.

But if you have even $1 remaining when the promotional period ends, all the deferred interest gets charged at once. At 32.99% APR on $3,600 over 18 months, that is approximately $1,782 in retroactive interest. You would have been better off putting the entire amount on a standard credit card at 22% APR from day one.

Afterpay, Klarna Pay-in-4, Cherry, and Affirm do not use deferred interest. What you see is what you pay. This transparency is a significant advantage, even if their interest rates on extended plans might be slightly higher than CareCredit promotional rates.

Impact on your credit score

Afterpay and Klarna Pay-in-4 perform soft credit checks that do not affect your score. However, both platforms have started reporting payment data to credit bureaus. On-time payments can help your score. Late payments can hurt it. This is a relatively new development and something to factor into your decision, especially if you are planning a major purchase like a home or car in the near future.

CareCredit performs a hard credit inquiry when you apply, which temporarily lowers your score by 5-10 points. The account also shows up as a new credit line, which can affect your credit utilization ratio if you carry a balance.

Cherry and Affirm both start with soft checks. Affirm may perform a hard check for larger financing amounts, but they disclose this clearly before you proceed.

For most people paying for monthly tirzepatide, the credit impact is minimal if payments are made on time. But if you are juggling multiple BNPL accounts for various expenses, the cumulative effect on your credit profile can become significant.

How to reduce tirzepatide costs without financing

The best financing is no financing at all. Before committing to a BNPL plan, exhaust every option for reducing your base cost. A lower monthly payment to finance is always better than a higher one, regardless of the interest rate.

Compounded alternatives

If you are currently paying $1,000+ for brand-name tirzepatide, switching to a compounded version can reduce your monthly cost by 50-75%. Compounded tirzepatide from reputable telehealth providers typically costs between $200 and $500 per month depending on the dose and any added compounds like glycine or B12.

The savings are substantial. Over a year, the difference between $1,000 per month brand-name and $300 per month compounded is $8,400. That is more than any BNPL platform could ever save you in interest avoidance.

Use the compounded tirzepatide dosage calculator to determine exactly how much medication you need at your current dose, then compare provider prices at that specific dose level. Prices can vary significantly between dose tiers.

Manufacturer savings programs

Eli Lilly offers several savings programs that can dramatically reduce costs:

The Zepbound Savings Card brings the cost to as low as $25 per month for commercially insured patients. You need non-government insurance that covers tirzepatide, and you must meet eligibility criteria. But if you qualify, this is by far the cheapest option available.

The Zepbound Self Pay Journey Program through LillyDirect reduces self-pay pricing to $349-$499 per month depending on dose. No insurance required. This program launched specifically to address affordability concerns and represents a significant price reduction from the $1,080+ list price.

Both programs are worth exploring before turning to BNPL. The savings card alone could reduce your annual cost from $12,000+ to $300, making the entire question of financing irrelevant.

HSA and FSA accounts

Health Savings Accounts and Flexible Spending Accounts let you pay for tirzepatide with pre-tax dollars. Depending on your tax bracket, this effectively reduces the cost by 22-37%. On a $400 monthly tirzepatide expense, HSA/FSA usage saves $88-$148 per month compared to after-tax dollars.

Most telehealth providers accept HSA and FSA debit cards directly. Some providers, like Fridays, specifically advertise HSA/FSA acceptance for their GLP-1 medication programs. If your provider does not accept HSA/FSA cards at the point of sale, you can often submit the receipt for reimbursement through your plan administrator.

Important: HSA/FSA eligibility for tirzepatide requires a qualifying medical diagnosis (obesity or Type 2 diabetes). Weight loss for cosmetic purposes alone may not qualify. Check with your plan administrator before assuming coverage.

You can combine HSA/FSA with some BNPL options. Pay with Afterpay, then submit the Afterpay receipt to your HSA/FSA for reimbursement. This gives you both the installment flexibility of BNPL and the tax savings of pre-tax dollars. Not all plan administrators allow this, so verify before attempting it.

Insurance coverage strategies

Insurance coverage for tirzepatide has expanded significantly. If you have commercial insurance:

Check if Mounjaro (for Type 2 diabetes) or Zepbound (for weight management) is on your formulary. Even if the branded weight loss indication is not covered, the diabetes indication might be if you have a qualifying diagnosis. Work with your prescribing provider to ensure proper coding.

Prior authorization is almost always required. Your provider should handle this, but follow up proactively. Prior authorization denials can often be appealed, and many appeals succeed on the first try. The typical timeline from initial denial to successful appeal is 2-4 weeks.

If your insurance denies coverage entirely, ask your provider about patient assistance programs and copay cards. The combination of insurance (even partial coverage) plus a copay card can reduce costs to near-zero for qualifying patients.

Dose optimization

One of the most overlooked cost reduction strategies is dose optimization. Many patients continue at higher doses when a lower dose would maintain their results. A step down from 15 mg to 10 mg or from 10 mg to 7.5 mg can reduce costs by 20-40% depending on the provider pricing structure.

Some researchers also explore microdosing tirzepatide or using a microdose schedule during maintenance phases. This approach can significantly extend the life of each vial, reducing monthly costs. Always work with your healthcare provider when adjusting doses.

Use the tirzepatide dosage calculator to understand exactly how your dose translates to units and cost per injection. This data empowers conversations with your provider about dose optimization for both results and affordability.

Step by step guide to using Afterpay for tirzepatide

If you have decided Afterpay is the right choice for your situation, here is exactly how to set it up and use it effectively.

Step 1: Download and set up Afterpay

Download the Afterpay app from the Apple App Store or Google Play Store. Create an account using your email address and phone number. Link a debit or credit card. Afterpay works with most major cards, but debit cards are recommended since they draw from existing funds rather than creating additional credit debt.

Step 2: Find a provider that accepts Afterpay

Visit the Afterpay website and search for "weight loss" in their store directory. This will show you providers that have integrated Afterpay. Alternatively, when browsing telehealth providers or tirzepatide medication options, look for the Afterpay logo on their checkout page.

You can also use the Afterpay Card (a virtual card) at providers that accept Visa but do not specifically integrate Afterpay. The Afterpay Card generates a one-time virtual Visa number that charges to your Afterpay account. This dramatically expands where you can use Afterpay, including at some telehealth providers that do not have a direct integration.

Step 3: Complete your purchase

At checkout, select Afterpay as your payment method. Log in to your Afterpay account. The platform will show you the payment schedule: four equal installments, the first due immediately and the remaining three every two weeks. Review the schedule, confirm, and complete the purchase. Your first payment processes immediately and your order ships normally.

Step 4: Manage your payment schedule

The Afterpay app shows all upcoming payments, due dates, and payment history. Enable push notifications so you never miss a due date. You can also set up auto-pay to ensure payments process automatically. If you need to make a payment early, the app allows that as well.

Step 5: Repeat monthly

For ongoing tirzepatide treatment, you will create a new Afterpay installment plan each month when you reorder medication. Each month is a separate Afterpay transaction. This means at any given time, you might have overlapping installment plans. For example, your February purchase might still have two payments remaining when you place your March order.

Track this carefully. Overlapping plans can stack up. Two active Afterpay plans at $400 each means $200 in biweekly payments rather than $100. Budget accordingly and make sure your linked card has sufficient funds for each automatic deduction.

Pro tips for using Afterpay effectively

Time your purchases strategically. If you get paid biweekly, place your tirzepatide order the day after payday. This aligns your first Afterpay payment with your highest bank balance, and subsequent payments will land near future paydays.

Build a buffer. Before starting Afterpay for medication, have at least two months of medication cost in savings. This protects you from cascading late fees if an unexpected expense disrupts your cash flow.

Never use Afterpay on top of a credit card unless you pay that credit card in full each month. Afterpay charging to a credit card that carries a balance means you are effectively paying interest on your Afterpay purchases, defeating the entire purpose of interest-free installments.

When financing makes sense (and when it does not)

BNPL for medication is not inherently good or bad. It is a tool, and like any tool, it works well in some situations and poorly in others.

Financing makes sense when

Your income is stable but your cash flow is lumpy. Maybe you get paid monthly or have irregular freelance income. Splitting a $400 expense into four $100 payments aligns the cost with your cash flow without any actual financial risk. You have the money. You just need it spread out.

You are starting tirzepatide and want to test it before committing financially. Using Afterpay for your first month lets you try the starting dose without a large upfront investment. If the medication does not work for you or the side effects are intolerable, you have not overcommitted financially.

A multi-month prepayment discount exceeds the financing cost. Some providers offer 10-20% off for 3-month or 6-month prepayments. If you can finance a $1,500 three-month supply at 0% through Afterpay or Cherry and save $300 compared to paying monthly, the math clearly favors financing.

Financing does not make sense when

You are already carrying significant debt. Adding another payment obligation, even an interest-free one, increases your financial stress and risk. If you miss a payment due to other obligations, the late fees and credit impact negate any benefits.

You are stretching to afford the medication at all. If $400 per month is genuinely beyond your means, splitting it into $100 installments does not solve the underlying problem. You will still owe the full amount. Consider a lower-cost provider, compounded alternatives, or discussing affordability options with your provider before turning to financing.

You tend to lose track of payment schedules. BNPL platforms are designed to be easy to use, which also makes them easy to forget about. If you have a history of missing bill payments, the late fees and credit impact make BNPL more expensive than simply waiting until you have saved enough to pay outright.

The medication is not yet proven to work for you. If you have not started tirzepatide treatment yet, consider starting with a single month paid in full before committing to financed multi-month packages. This protects you from financing medication you might not continue using.

Real-world payment scenarios for different budgets

Abstract comparisons only go so far. Here is how BNPL plays out in three real budgeting situations that cover the majority of people looking at tirzepatide financing.

Scenario 1: the steady paycheck ($60,000 annual income)

At $60,000 per year, your monthly take-home is roughly $3,800 after taxes. A $400 monthly tirzepatide expense represents about 10.5% of your net income. That is significant but manageable for most household budgets.

The best approach here: Use Afterpay or Klarna Pay-in-4 to smooth cash flow, not to extend your budget. Set up automatic payments aligned with your pay schedule. The four biweekly installments of $100 feel much more manageable than a single $400 charge, and the zero interest means you pay exactly the same amount either way. Factor in the cost of recommended supplements and proper nutrition planning to get a complete picture of your monthly investment.

At this income level, also explore whether a compounded option at $250-$300 per month makes the BNPL question irrelevant entirely. The compounded tirzepatide dosing chart can help you understand whether compounded versions deliver equivalent dosing to what you need.

Scenario 2: the tight budget ($35,000 annual income)

At $35,000 per year, monthly take-home is roughly $2,450. A $400 medication expense is over 16% of net income, which puts significant pressure on other essentials. BNPL does not solve this problem. It just rearranges the same money into smaller pieces.

The priority here is cost reduction, not financing. Start with the lowest-cost compounded tirzepatide provider available. Maximize manufacturer savings programs and copay cards. Apply for patient assistance if available. Consider whether compounded semaglutide at a lower price point achieves similar goals. Only after minimizing the base cost should you layer in BNPL to manage what remains.

If you are in this situation, Cherry or CareCredit promotional financing might actually be counterproductive. The temptation to finance a larger package "because the monthly payment is low" can lead to debt that outlasts your treatment. Stick to Afterpay or Klarna Pay-in-4, which limit your exposure to six weeks per purchase cycle.

Scenario 3: the variable income (freelancers, gig workers, commission-based)

Variable income creates a unique challenge. You might earn $6,000 one month and $2,000 the next. BNPL platforms with fixed payment schedules do not adapt to this reality. A $100 Afterpay payment that is easy in a good month becomes a problem in a lean one.

The best approach for variable income: Build a medication fund during high-income months. Set aside two to three months of medication cost in a dedicated savings account. Pay for tirzepatide from this fund rather than from monthly income. This eliminates the need for BNPL entirely and protects against late fees during low-income periods.

If you do use BNPL with variable income, Affirm is the safest choice because it charges no late fees. One missed payment does not cascade into a penalty spiral the way it can with Afterpay or CareCredit. This flexibility matters when your income timing is unpredictable.

SeekPeptides provides detailed guides on optimizing treatment protocols for maximum efficiency, which is especially valuable when every dollar counts. Understanding how to get the best possible results from each dose means potentially achieving your goals faster and spending less overall on your treatment journey.

Comparing total cost of ownership by payment method

Raw numbers tell the real story. Here is what $400 per month of tirzepatide actually costs over 12 months under different payment scenarios:

Payment method | Monthly payment | Total paid (12 months) | Total interest/fees |

|---|---|---|---|

Cash pay | $400 | $4,800 | $0 |

Afterpay (on time) | $100 x 4 biweekly | $4,800 | $0 |

Afterpay (1 late/quarter) | $100 x 4 + fees | $5,072 | $272 |

Klarna Pay-in-4 | $100 x 4 biweekly | $4,800 | $0 |

CareCredit 0% (paid in full) | $400 | $4,800 | $0 |

CareCredit (not paid in full) | Varies | Up to $6,384 | Up to $1,584 |

Affirm 12-month 15% | $436 | $5,232 | $432 |

Credit card 24% APR | Minimum varies | $5,568+ | $768+ |

HSA/FSA (25% tax bracket) | $300 effective | $3,600 effective | -$1,200 (savings) |

The takeaways are clear. Afterpay and Klarna Pay-in-4 cost nothing extra if you pay on time. CareCredit is either the best or worst option depending on whether you clear the balance before the promotional period ends. HSA/FSA provides the most genuine savings by reducing your tax-adjusted cost by 20-37%.

For perspective, the difference between the cheapest compounded tirzepatide provider ($219/month) and a mid-range provider ($400/month) over 12 months is $2,172. That dwarfs any interest savings from choosing the right BNPL platform. Shopping for the right provider matters far more than shopping for the right payment method.

Alternative payment strategies worth considering

BNPL is not the only creative approach to managing tirzepatide costs. Several other strategies can make your medication more affordable without any financing at all.

Prescription discount cards

GoodRx, RxSaver, and similar platforms offer discount pricing on brand-name tirzepatide. These discounts vary by pharmacy and location, but savings of 10-30% off retail pricing are common. Prescription discount cards work independently of insurance and BNPL, so they can be stacked with other savings strategies.

Multi-month purchasing

Some providers offer significant discounts for committing to multi-month supplies. A three-month purchase at 15% off effectively gives you two weeks of free medication. Even if you need to use CareCredit or Cherry to finance the larger upfront cost, the discount often exceeds any interest charges.

This strategy works particularly well for established patients who know their optimal dose and are committed to long-term treatment. New patients should avoid multi-month prepayments until they have confirmed their starting dose works for them. The tirzepatide dose chart can help you understand the standard titration schedule before committing to a bulk purchase.

Reconstitution at home

For compounded lyophilized tirzepatide (powder form), learning to reconstitute tirzepatide yourself can save money compared to pre-mixed liquid formulations. The powder form is often less expensive, and proper reconstitution using the right amount of bacteriostatic water ensures accuracy. The peptide reconstitution calculator walks you through the exact measurements needed for your specific vial size and desired concentration.

Semaglutide as a lower-cost alternative

If tirzepatide costs remain prohibitive even with BNPL, semaglutide offers a potentially more affordable alternative. Compounded semaglutide typically costs less than compounded tirzepatide, and some patients achieve similar results. Our semaglutide vs tirzepatide side effects comparison and the dosage comparison chart can help you and your provider evaluate whether switching makes sense for your situation.

For those curious about newer options, the three-way comparison between semaglutide, tirzepatide, and retatrutide provides a broader view of the GLP-1 medication landscape and how costs compare across the category.

Common mistakes people make when financing tirzepatide

After reviewing hundreds of conversations about BNPL for weight loss medication, clear patterns emerge. These are the mistakes that cost people the most money, and each one is completely avoidable.

Mistake 1: Choosing a provider based on payment options instead of quality. A clinic that accepts Afterpay is not automatically better than one that requires cash. If the Afterpay-friendly provider charges $500 per month for the same compounded tirzepatide that a cash-only provider sells for $280, the payment convenience costs you $2,640 per year. Always compare the medication price first, then layer in the payment method.

Mistake 2: Stacking multiple BNPL plans without tracking totals. With monthly tirzepatide purchases, Afterpay plans overlap. Your January purchase still has payments due when February order ships. By month three, you might have three active plans running simultaneously, totaling $300 in biweekly BNPL deductions instead of $100. People who do not track these overlaps get hit with insufficient funds fees from their bank on top of Afterpay late fees.

Mistake 3: Using CareCredit without a payoff plan. The 0% promotional rate is genuinely appealing. But one in four CareCredit users fails to pay off their promotional balance before the deadline, according to consumer advocacy reports. At 32.99% deferred interest, a $2,400 balance left unpaid for even one day past the promotional period generates $800+ in retroactive interest. If you use CareCredit, set up automatic payments that will clear the balance at least one month before the promotional deadline.

Mistake 4: Not exploring all discount options before financing. Many people jump to BNPL without checking whether they qualify for the Eli Lilly Savings Card ($25/month with qualifying insurance), manufacturer patient assistance programs, or HSA/FSA tax savings. The combination of these programs can make financing unnecessary entirely. Check every discount avenue before committing to installment payments.

Mistake 5: Continuing to finance medication that is not working. If you are not losing weight on tirzepatide after adequate time at an appropriate dose, financing additional months does not fix the problem. It just adds to your debt. Discuss treatment adjustments with your provider before continuing to pay for medication that needs optimization. Sometimes a dose adjustment, switching to a different formulation, or addressing weight loss plateau factors makes the difference between wasted money and a successful outcome.

What to look for in a tirzepatide provider (beyond payment options)

Payment flexibility matters, but it should not be the primary factor in choosing a provider. A provider that accepts Afterpay but delivers inconsistent medication quality is a worse deal than a cash-only provider with excellent track record.

Quality indicators

Check if the provider works with an accredited compounding pharmacy. Empower Pharmacy, for instance, is a well-known 503B outsourcing facility with stringent quality controls. Providers who name their compounding pharmacy partner are generally more transparent than those who do not.

Verify that the provider requires a consultation (telehealth or in-person) before prescribing. Any provider that ships tirzepatide without a medical evaluation should be avoided entirely. Proper medical oversight ensures your tirzepatide dosage is appropriate for your health profile and that potential interactions with other medications are screened.

Look for providers who include ongoing monitoring. Weight loss medication is not a one-time prescription. The best programs include regular check-ins, dose adjustments, and access to medical support throughout your treatment. This ongoing care is especially important during dose titration when side effects like headaches, constipation, and fatigue are most common.

Red flags to watch for

Prices significantly below market rates can indicate quality issues. If a provider charges $150 per month when comparable providers charge $300-$400, ask what accounts for the difference. Lower doses, less frequent shipments, or unaccredited compounding sources might explain the gap.

Providers who push unnecessary add-ons or upsells during the payment process should raise concerns. Your focus should be on getting the right medication at the right dose, not on adding supplements or accessories that inflate the total cost and BNPL balance.

Guaranteed rapid results or "money back" promises are marketing tactics, not medical claims. Tirzepatide works, but results vary between individuals and the typical weight loss timeline spans months, not days. Providers making unrealistic claims may also be cutting corners on quality.

Optimizing your tirzepatide investment

Whether you use Afterpay, Klarna, CareCredit, or pay cash, getting the most value from your tirzepatide investment goes beyond payment method. Several factors affect how much medication you actually need and how long your supply lasts.

Proper storage extends shelf life

Improperly stored tirzepatide loses potency, which means you are paying full price for medication that is not working at full strength. Compounded tirzepatide should be refrigerated between 36-46 degrees Fahrenheit. Understanding how long tirzepatide lasts in the fridge and how long it can be out of the fridge protects your investment and ensures every dollar you spend delivers the expected results.

If you travel, plan your medication transport carefully. Our guide on traveling with GLP-1 medications covers storage solutions for various travel scenarios, which applies equally to tirzepatide.

Injection technique affects absorption

Poor injection technique can reduce how much medication your body absorbs, effectively wasting a portion of each dose. Learn the correct injection technique for tirzepatide and rotate injection sites to maximize absorption and minimize injection site reactions. Our guide on optimal injection sites provides detailed guidance on site selection and rotation patterns.

Understanding proper syringe dosage is equally important. Drawing too much or too little medication from a vial means either wasted product or underdosing. Both scenarios cost you money.

Diet and lifestyle amplify results

Tirzepatide is not a standalone solution. Pairing your medication with the right nutrition strategy amplifies results, potentially allowing you to achieve your goals at a lower dose (saving money) and maintain results longer. Our tirzepatide diet plan, meal plan, and foods to avoid guide provide specific nutritional strategies designed to work with the medication rather than against it.

Supporting your treatment with the right supplements can also improve outcomes and reduce side effects. Fewer side effects means better adherence, which means faster results, which means potentially shorter treatment duration and lower total cost.

Getting adequate protein is especially important on GLP-1 medications. These drugs reduce appetite significantly, and without deliberate protein intake, you risk losing muscle mass along with fat. Muscle loss slows your metabolism and can compromise long-term weight maintenance.

The bigger picture: budgeting for long-term tirzepatide treatment

Most BNPL guides treat medication purchases as one-time transactions. Tirzepatide treatment is fundamentally different. This is a recurring monthly expense that may continue for a year or longer. Your payment strategy needs to account for this reality.

Building a medication budget

Calculate your total expected annual cost based on your provider pricing and expected dose progression. If you are starting at 2.5 mg and expect to titrate up to 10 mg over several months, factor in price increases at each dose tier. A provider that charges $250 for the starting dose might charge $450 at the maintenance dose.

Map your expected costs month by month. Include the medication itself, any consultation fees, shipping costs, and the BNPL installment schedule if you choose to finance. Seeing the full picture upfront prevents surprises and helps you identify points where the cost might become unsustainable.

Set aside a medication emergency fund equal to at least one month of treatment cost. This buffer prevents missed doses (and missed BNPL payments) if an unexpected expense disrupts your cash flow. Consistency is critical with tirzepatide. Missed doses can trigger treatment plateau and set back your progress.

Planning your exit strategy

Tirzepatide treatment is not meant to continue indefinitely at the same dose. Many patients eventually reduce their dose, switch to maintenance-level dosing, or transition off the medication entirely. Understanding the typical weight loss timeline helps you estimate how long you will need treatment and plan your budget accordingly.

If you are using CareCredit or Cherry for extended financing, align your repayment timeline with your expected treatment duration. Paying off a 24-month CareCredit balance should ideally coincide with the point where you expect to reduce or stop treatment, eliminating the risk of financing medication you no longer need.

Some patients find success with switching from tirzepatide to semaglutide for maintenance. Since semaglutide is often less expensive, this can reduce your long-term costs while maintaining results. Discuss this possibility with your provider as part of your overall treatment and financial plan.

Navigating the medication form options

The form of tirzepatide you choose also affects cost and, by extension, your payment strategy. Injectable tirzepatide remains the most common form, but alternatives are entering the market.

Oral tirzepatide is in development and early availability, offering a needle-free option. Our oral vs injection comparison covers the current state of this alternative, including how pricing compares between the two forms. Tirzepatide drops and tirzepatide tablets each have different cost structures and absorption profiles that affect value per dollar spent.

The orally dissolving tablet (ODT) format represents another option with its own pricing structure. As more delivery methods become available, comparing the cost per effective milligram across formats becomes increasingly important for budget-conscious patients.

Special considerations for specific situations

Starting treatment on a tight budget

If you are determined to start tirzepatide but your budget is extremely tight, here is the most cost-effective approach. Choose a compounded tirzepatide provider at the lowest price point for starting doses. Use Afterpay or Klarna Pay-in-4 to split the first month into installments. Start at the lowest effective dose and titrate slowly based on response. Do not prepay for multiple months until you have confirmed the medication works for you.

This approach minimizes risk. If tirzepatide is not right for you, due to side effects, body aches, insomnia, or simply not seeing results after adequate time, you have only committed to one month of financing rather than a multi-month package.

Combining medications

Some patients combine tirzepatide with other compounds like AOD-9604 or take it alongside phentermine. These combinations increase total monthly medication cost. If you are using BNPL for tirzepatide alone and paying cash for add-on medications, or vice versa, track the total across all payment methods to maintain an accurate picture of your monthly healthcare spending.

Pregnancy and treatment interruption

If you become pregnant while on tirzepatide, treatment must be stopped immediately. Understanding this possibility is relevant to payment planning because you may need to pause BNPL installments on medication you can no longer use. Our guide on pregnancy and tirzepatide covers what to do, and breastfeeding considerations address the postpartum timeline for potentially resuming treatment.

Surgical procedures can also interrupt treatment. If you have surgery planned, read our guide on resuming GLP-1 medication after surgery and factor the treatment gap into your financial planning. Unused medication that expires during a treatment interruption is wasted money.

Understanding the real cost of weight loss medication

Tirzepatide is an investment, not just an expense. Framing it purely as a cost overlooks the value it delivers. Successful weight loss reduces healthcare expenses over time: fewer medications for obesity-related conditions, lower risk of costly interventions, and improved quality of life that has economic value even if it does not show up on a balance sheet.

That said, an investment still needs to be affordable. The combination of choosing the right provider, selecting the appropriate payment method, optimizing your dose, and maximizing the effectiveness of each injection through proper storage, injection technique, and dietary support collectively determine your return on investment.

SeekPeptides members access detailed cost comparison tools, provider reviews, and protocol guides that help optimize every aspect of peptide treatment. Understanding not just what to take but how to take it most effectively translates directly into better results per dollar spent. The peptide cost calculator gives you a clear picture of your expected expenses across different providers and dose levels.

For researchers serious about optimizing their protocols and making informed decisions about providers, dosing, and treatment strategies, SeekPeptides offers the most comprehensive resource available, with evidence-based guides, proven protocols, and a community of thousands who have navigated these exact questions about affordability and treatment optimization.

Frequently asked questions

Can I use Afterpay to buy tirzepatide online?

Yes, but only through providers that have integrated Afterpay into their checkout system. Not all telehealth providers accept Afterpay. You can also use the Afterpay virtual Visa card at providers that accept Visa but do not have a direct Afterpay integration. Always confirm payment acceptance before starting the consultation process.

Does using Afterpay for tirzepatide affect my credit score?

Afterpay performs a soft credit check that does not appear on your credit report. However, Afterpay has begun reporting payment history to credit bureaus, meaning on-time payments can help your score and late payments can hurt it. CareCredit performs a hard credit check that temporarily lowers your score by 5-10 points.

What happens if I miss an Afterpay payment for my tirzepatide?

Afterpay charges a late fee when you miss a payment, with a second fee seven days later if still unpaid. Total late fees are capped at 25% of the order value or $68, whichever is less. Your account gets paused until you catch up. Repeated late payments may result in account suspension and can be reported to credit bureaus.

Is it better to use Afterpay or CareCredit for tirzepatide?

For monthly purchases under $500, Afterpay is simpler and carries no risk of deferred interest. For larger purchases like multi-month treatment plans, CareCredit offers higher credit limits and longer repayment terms but carries the risk of retroactive interest charges if you do not pay off the promotional balance in full. Afterpay charges no interest if paid on time. CareCredit can charge up to 32.99% retroactively.

Can I use HSA or FSA to pay for tirzepatide through Afterpay?

You can potentially link your HSA/FSA debit card as the payment method for Afterpay, though not all HSA/FSA plans allow this. Alternatively, pay with Afterpay using a regular card and submit the receipt to your HSA/FSA for reimbursement. Check with your plan administrator, as eligibility requires a qualifying medical diagnosis.

Which telehealth providers accept Afterpay for tirzepatide?

Provider acceptance changes frequently as new partnerships form. Currently, some medical spas, weight loss clinics, and telehealth platforms accept Afterpay either directly or through the Afterpay virtual card. Ivim Health specifically advertises Klarna, and Balanced Hormone Health offers Afterpay, Klarna, and CareCredit. Check each provider individual checkout page for current payment options.

How much does compounded tirzepatide cost with Afterpay?

The cost of compounded tirzepatide ranges from approximately $200 to $500 per month depending on the provider and dose. Afterpay does not change the price. It splits the payment into four equal, interest-free installments over six weeks. A $400 purchase becomes four payments of $100.

Are there any interest-free ways to pay for tirzepatide long-term?

Yes. Afterpay and Klarna Pay-in-4 are interest-free for each individual purchase cycle. CareCredit offers 0% promotional periods of 6-24 months (but watch for deferred interest). Cherry offers qualifying 0% APR on some plans. HSA/FSA accounts provide tax-advantaged payments that effectively reduce costs by 22-37%.

Should I prepay for multiple months of tirzepatide using BNPL?

Only if the provider offers a meaningful discount for multi-month purchases (typically 10-20% off) AND you are already on a stable dose. New patients still titrating through starting doses should not prepay, because dose adjustments might require switching products or providers. If you do prepay, use CareCredit or Cherry for the higher credit limits, and ensure you can pay off the balance before any promotional period expires.

Can I use the Afterpay virtual card for tirzepatide at any provider?

The Afterpay Card generates a single-use virtual Visa number that works anywhere Visa is accepted. This means you can potentially use Afterpay at providers that do not have a direct Afterpay integration, as long as they accept Visa payments online. However, some telehealth platforms use subscription billing that may not be compatible with single-use virtual cards. Test with a provider before relying on this method for ongoing medication purchases.

What is the cheapest way to get tirzepatide right now?

For commercially insured patients, the Eli Lilly Savings Card can bring costs as low as $25 per month. For uninsured or self-pay patients, the Zepbound Self Pay Journey through LillyDirect offers brand-name tirzepatide starting at $349 per month. For the absolute lowest cost, compounded tirzepatide from reputable telehealth providers starts around $200-$250 per month. Combining the lowest available price with HSA/FSA tax savings provides the greatest overall value.

How does tirzepatide cost compare to semaglutide?

Compounded semaglutide generally costs less than compounded tirzepatide, sometimes by $50-$150 per month depending on the provider and dose. However, clinical data suggests tirzepatide may produce greater average weight loss, which could mean shorter treatment duration. The tirzepatide vs semaglutide dosage chart and our head-to-head comparison cover the cost-effectiveness tradeoffs between these two GLP-1 medications in detail.

External resources

IRS Publication 502: Medical and Dental Expenses (HSA/FSA guidance)

Consumer Financial Protection Bureau: Buy Now, Pay Later guide

In case I do not see you, good afternoon, good evening, and good night. May your payments stay on time, your medication stay potent, and your results stay consistent.