Mar 8, 2026

Tired of getting conflicting answers about whether Anthem covers GLP-1 medications for weight loss? You are not alone. One person says they got Wegovy covered with no issues. Another says Anthem denied everything. A third person claims their employer plan covered Ozempic for weight loss last year but dropped it this year. The confusion is real, and it affects millions of people trying to access these medications through their Anthem insurance plans.

Here is the truth that most articles will not tell you. Anthem coverage for GLP-1 weight loss medications is not a simple yes or no answer. It never was. Coverage depends on your specific plan type, your state, your employer, your diagnosis codes, and even the specific GLP-1 medication your doctor prescribes. Two Anthem members living on the same street in the same city can have completely different coverage for the exact same medication.

This guide breaks down everything you need to know. We will cover which GLP-1 medications Anthem covers, which plans include weight loss coverage, how to navigate prior authorization, what to do when you get denied, and the alternative paths forward when insurance says no. Whether you are considering semaglutide or tirzepatide, understanding your insurance landscape is the first step toward actually getting treatment.

Understanding Anthem and GLP-1 medications

GLP-1 receptor agonists have transformed the weight loss landscape. These medications, which include semaglutide (sold as Ozempic and Wegovy) and tirzepatide (sold as Mounjaro and Zepbound), work by mimicking a natural hormone that regulates appetite, slows gastric emptying, and influences how the brain perceives hunger. The results have been remarkable. Clinical trials show average weight loss of 15% to 22% of total body weight, depending on the specific medication and dosage used.

But here is where things get complicated with Anthem specifically.

Anthem is one of the largest health insurance providers in the United States, operating under the Blue Cross Blue Shield umbrella in multiple states. The company offers employer-sponsored plans, individual marketplace plans, Medicare Advantage plans, and Medicaid managed care plans. Each category has its own formulary, its own coverage rules, and its own prior authorization requirements for GLP-1 fat loss treatment.

The distinction between "medically necessary" and "cosmetic" weight loss is central to how Anthem evaluates GLP-1 coverage. When a doctor prescribes Ozempic for type 2 diabetes management, Anthem generally covers it because the FDA approved semaglutide for that indication under the Ozempic brand. When that same doctor prescribes Wegovy for weight management, the coverage calculation changes entirely. Anthem views these as different clinical scenarios even though the active ingredient is identical. Understanding this distinction matters enormously if you want to qualify for semaglutide through your insurance.

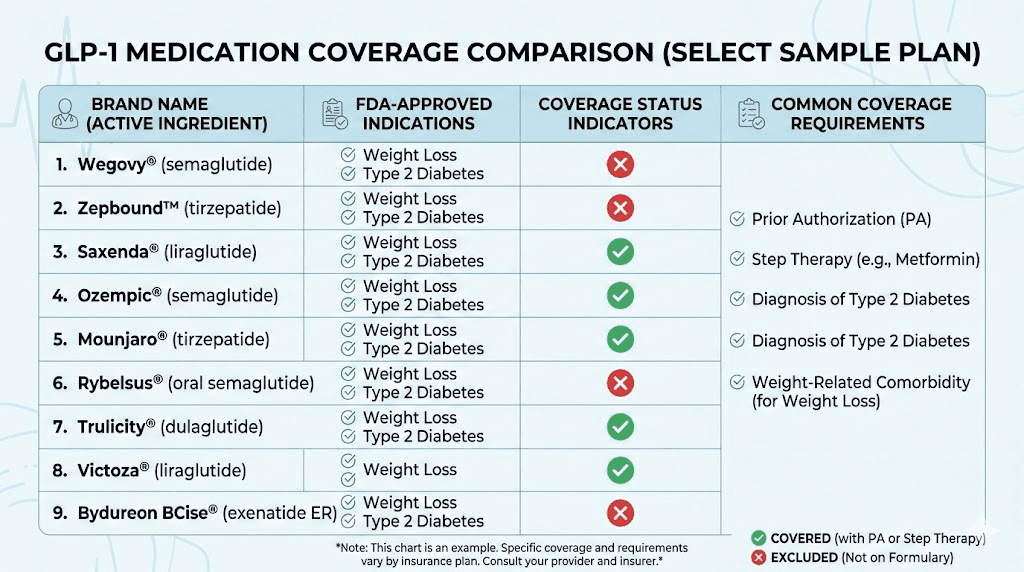

Which GLP-1 medications does Anthem cover?

The answer depends heavily on why the medication is prescribed. Let us break this down by medication and indication.

Semaglutide (Ozempic) for type 2 diabetes

Anthem generally covers Ozempic for type 2 diabetes management. It typically sits on Tier 2 of the formulary, which means higher copays than preferred generics but still within the covered medication list. Most Anthem plans require prior authorization even for diabetes use, and your doctor will need to document that you have tried other first-line diabetes medications like metformin before stepping up to Ozempic. If you are curious about whether GLP-1 is the same as Ozempic, the short answer is that Ozempic is one specific brand of GLP-1 receptor agonist.

The semaglutide dosage for diabetes typically starts at 0.25 mg weekly and increases over time. Your doctor will follow a specific titration schedule, and Anthem expects to see this documented progression in your medical records.

Semaglutide (Wegovy) for weight management

This is where things get difficult. Effective January 1, 2026, many Anthem plans removed Wegovy from their formulary for weight loss coverage. Some employer-sponsored plans still include it, but they are becoming rarer. When Wegovy is covered, it almost always sits in the non-preferred tier with strict prior authorization requirements.

However, Wegovy continues to receive coverage for two specific FDA-approved indications beyond general weight management. The first is MASH (metabolic dysfunction-associated steatohepatitis), a serious liver condition. The second is cardiovascular risk reduction in adults with established cardiovascular disease and obesity. If your doctor can document either of these conditions, your path to coverage becomes significantly clearer.

Tirzepatide (Mounjaro) for type 2 diabetes

Mounjaro maintains coverage under most Anthem plans for type 2 diabetes. Like Ozempic, it requires prior authorization and documentation of previous medication trials. The tirzepatide dosage protocol starts at 2.5 mg weekly with gradual increases, and Anthem typically wants to see this titration documented before approving ongoing coverage.

Tirzepatide (Zepbound) for weight management

Zepbound, the weight management formulation of tirzepatide, has an interesting coverage exception under some Anthem plans. While general weight loss coverage may be excluded, Zepbound has received FDA approval for moderate to severe obstructive sleep apnea in adults with obesity. If you have a documented sleep apnea diagnosis alongside obesity, some Anthem plans will cover Zepbound under this indication. The oral tirzepatide guide covers newer formulation options as well.

Other GLP-1 medications

Several other GLP-1 receptor agonists have also been affected by Anthem coverage changes. Victoza (liraglutide), Byetta (exenatide), Bydureon (extended-release exenatide), and Trulicity (dulaglutide) are no longer eligible for weight loss coverage under many Anthem plans. These medications may still be covered for their FDA-approved diabetes indications, but using them off-label for weight management is increasingly difficult to get approved. If you are comparing options, understanding the differences between medications like phentermine and GLP-1 can help you explore alternatives.

Why Anthem coverage varies so dramatically

Understanding why two Anthem members can have completely different coverage requires understanding how health insurance actually works in the United States.

Employer-sponsored plans

Most Americans with Anthem coverage get it through their employer. Here is the critical detail that many people miss. Large employers often self-insure, meaning the employer, not Anthem, decides what the plan covers. Anthem simply administers the plan, processes claims, and manages the provider network. When a self-insured employer decides to exclude GLP-1 weight loss coverage, Anthem has no say in that decision.

Some employers have embraced GLP-1 coverage as a way to reduce long-term healthcare costs. Others have dropped it because the short-term expense is enormous. A single employee on Wegovy costs the plan roughly $12,000 to $16,000 per year. Multiply that across hundreds or thousands of employees, and the financial impact becomes staggering. This is why coverage can change from one plan year to the next without warning.

State-level variations

Anthem operates under different names and regulatory environments in different states. California Medi-Cal plans administered by Anthem ended all GLP-1 weight loss coverage. Blue Cross Blue Shield of Massachusetts, which operates within the same corporate family, ended obesity coverage as well. Meanwhile, some state-regulated individual plans may still include weight management medications because state insurance commissioners mandate certain coverage minimums.

The regulatory patchwork creates a situation where moving from one state to another, or switching from an employer plan to a marketplace plan, can completely change your GLP-1 coverage status. If you previously had coverage through Blue Cross Blue Shield, switching to an Anthem plan in a different state may yield different results entirely.

Plan tier and formulary differences

Even within the same employer, different plan options may have different formularies. A gold-tier plan might include Wegovy as a non-preferred brand, while a bronze-tier plan from the same employer excludes it entirely. The annual open enrollment decisions you make can have massive implications for your medication access.

Your plan formulary is a living document. It can change mid-year in some cases, though insurers typically must provide 60 days notice before removing a medication. If you started the year with GLP-1 coverage and receive a notice that your formulary is changing, you have a narrow window to explore your options.

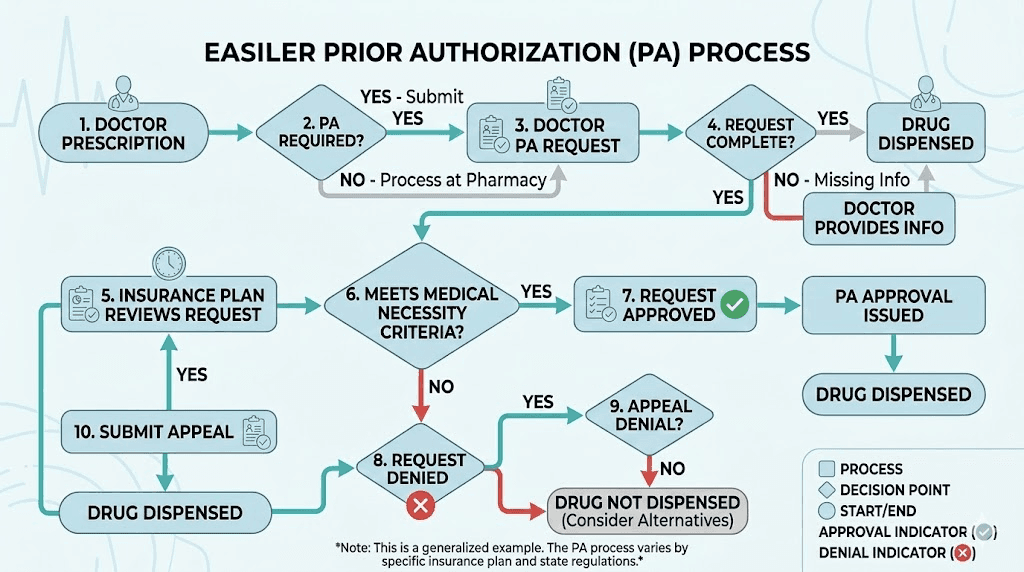

The prior authorization process for GLP-1 coverage

Even when your Anthem plan includes GLP-1 weight loss medications on the formulary, you will almost certainly need prior authorization before the pharmacy will fill your prescription. Prior authorization is the process where your doctor submits clinical documentation to Anthem proving that the medication is medically necessary for your specific situation. Understanding the BMI requirements for GLP-1 is essential before starting this process.

Clinical criteria Anthem evaluates

Anthem uses specific clinical criteria to determine whether a GLP-1 prescription meets their definition of medical necessity. The requirements typically include several factors that your doctor must document clearly.

First, your BMI must meet minimum thresholds. For most GLP-1 weight management medications, Anthem requires a BMI of 30 or greater (clinical obesity) or a BMI of 27 or greater with at least one weight-related comorbidity. Qualifying comorbidities include type 2 diabetes, hypertension, dyslipidemia (abnormal cholesterol levels), and obstructive sleep apnea. Your doctor needs to document your current BMI with recent measurements, not estimates from a previous visit.

Second, you must demonstrate documented lifestyle modification efforts. This means 3 to 6 months of structured diet and exercise programs with documentation in your medical records. A gym membership alone does not count. Anthem wants to see progress notes from your healthcare provider documenting specific dietary counseling, caloric goals, physical activity recommendations, and follow-up assessments showing that lifestyle changes alone were insufficient.

Third, step therapy requirements may apply. Many Anthem plans require you to try and fail 2 to 3 other weight management medications before approving a GLP-1. This might include medications like phentermine, orlistat, or naltrexone-bupropion (Contrave). "Failure" can mean inadequate weight loss, intolerable side effects, or documented contraindications. Understanding the difference between these older medications and GLP-1s, such as phentermine versus semaglutide or phentermine versus tirzepatide, can help you discuss options with your doctor.

Fourth, Anthem requires that you not be taking multiple GLP-1 medications simultaneously. You cannot be on Ozempic for diabetes and Wegovy for weight loss at the same time. This seems obvious, but it trips up patients who switch between medications without properly discontinuing the previous one.

Documentation your doctor needs to submit

The prior authorization submission is only as strong as the documentation behind it. Your doctor should include recent lab work showing metabolic markers, a detailed weight history spanning at least the past 12 months, documentation of all lifestyle modification efforts with specific dates and outcomes, records of previous weight management medications tried and the reasons they were discontinued, and a Letter of Medical Necessity explaining why a GLP-1 medication is the appropriate next step for your care.

A strong Letter of Medical Necessity goes beyond simply listing your BMI and comorbidities. The best letters connect your obesity to specific health outcomes, reference clinical guidelines supporting GLP-1 use, and explain why alternative treatments have been insufficient. If your doctor needs guidance on how to qualify for semaglutide through insurance, this documentation checklist is the starting point.

The timeline for prior authorization

Standard prior authorization requests through Anthem typically receive a response within 5 to 15 business days. Urgent requests, where your doctor certifies that a delay could seriously harm your health, must receive a response within 72 hours. During this waiting period, you cannot fill the prescription at the pharmacy.

If the prior authorization is approved, it typically lasts for 6 months. At the 6-month mark, Anthem requires renewal documentation showing that the medication is working. For weight loss indications, this usually means demonstrating at least a 5% reduction in total body weight. If you have not lost enough weight, the renewal may be denied, and you would need to explore other options or appeal. Tracking your progress with resources like semaglutide results week by week can help you stay on track for renewal.

What to do when Anthem denies your GLP-1 coverage

Denial is not the end. This is worth repeating because the statistics are striking. Up to 80% of insurance appeals succeed, yet 69% of people who receive a denial do not even know they can appeal. Even more alarming, 85% of denied patients never attempt an appeal at all. That means the vast majority of people who could get their medication covered simply give up at the first no.

Do not be one of them.

Understanding your denial letter

When Anthem denies your GLP-1 prior authorization, they are required to send you a written explanation. This letter is the most important document in your appeal process. Read it carefully. It will contain the specific reason for denial, which falls into a few common categories.

The most common denial reason is "not medically necessary," which means Anthem determined that your clinical documentation did not meet their coverage criteria. The second most common is step therapy failure, meaning you have not tried enough lower-cost medications first. Third is formulary exclusion, which means the specific medication is simply not on your plan formulary regardless of medical necessity. Each type of denial requires a different appeal strategy.

The internal appeal process

You have 180 days from the denial date to file an internal appeal with Anthem. This is your first formal opportunity to challenge the decision. The appeal should include updated clinical documentation from your doctor, a detailed Letter of Medical Necessity that directly addresses the specific reason for denial, any new medical evidence supporting your need for GLP-1 therapy, and peer-reviewed research supporting the use of GLP-1 medications for your specific condition.

Patient-initiated appeals carry stronger legal protections than provider-initiated appeals. When you file the appeal yourself as the patient, Anthem must respond within specific timeframes mandated by state and federal law. Standard appeals typically require a response within 30 days. Urgent appeals, where continued denial could seriously jeopardize your health, require a response within 72 hours.

Requesting an external review

If your internal appeal is denied, you have the right to request an external review. This means an independent third-party organization, not Anthem, reviews your case and makes a binding decision. External reviews are particularly valuable because the independent reviewers often apply clinical guidelines more broadly than insurance companies do.

To request an external review, file within 4 months of the internal appeal denial. The external reviewer will evaluate your complete medical record, the clinical evidence supporting GLP-1 use, and whether Anthem applied their own coverage criteria correctly. This process typically takes 45 days for standard requests and 72 hours for urgent situations.

Tips that improve your appeal success rate

Several specific strategies significantly improve your chances of a successful appeal. Your doctor should reference the American Medical Association and American Academy of Pediatrics clinical practice guidelines that recognize obesity as a chronic disease requiring medical treatment. Including specific clinical trial data showing the efficacy of the prescribed GLP-1 medication for patients with your BMI range and comorbidities strengthens the case considerably.

Document the financial burden of untreated obesity on your overall healthcare costs. If your obesity contributes to conditions that Anthem is already covering, like hypertension medication or sleep apnea equipment, make the argument that GLP-1 treatment could reduce those costs over time.

Request that your appeal be reviewed by a board-certified endocrinologist or obesity medicine specialist. Anthem is required to have the appeal reviewed by a physician with relevant clinical expertise, and specifying the specialty ensures the reviewer understands the nuances of obesity treatment.

State-specific Anthem GLP-1 coverage details

Because Anthem operates under different regulatory frameworks in different states, coverage rules can vary significantly depending on where you live.

California

Anthem Blue Cross in California administers Medi-Cal managed care plans that have ended all GLP-1 weight loss coverage. However, employer-sponsored plans in California may still include coverage depending on the employer decision. Individual marketplace plans in California follow Covered California formulary guidelines, which may differ from employer plans. If you are in California and considering your options, understanding the compounded semaglutide landscape can provide alternative pathways.

Massachusetts

Blue Cross Blue Shield of Massachusetts, operating within the Anthem corporate family, ended obesity medication coverage effective January 1, 2026. This affects both Wegovy and Zepbound for weight loss indications. However, these medications remain covered for type 2 diabetes (Ozempic, Mounjaro) and other FDA-approved non-weight-loss indications.

Other states

Coverage in states like Virginia, Georgia, Indiana, Ohio, Wisconsin, Connecticut, Colorado, Nevada, New Hampshire, and Maine varies based on plan type and employer decisions. Some states have enacted or are considering legislation that would require insurers to cover FDA-approved obesity medications. Checking with your state insurance commissioner office can provide the most current regulatory landscape for your location.

Alternative paths when Anthem does not cover GLP-1 for weight loss

When insurance coverage is not available, several alternative pathways exist for accessing GLP-1 medications. Each has trade-offs in terms of cost, convenience, and clinical supervision.

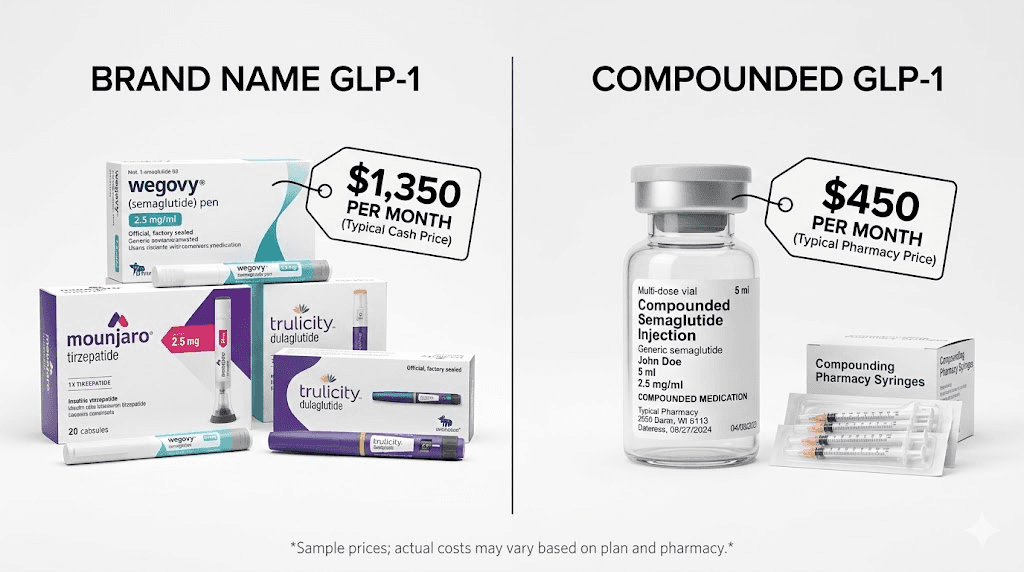

Compounded semaglutide and tirzepatide

Compounded versions of semaglutide and tirzepatide represent one of the most popular alternatives to brand-name medications. These formulations are produced by 503A and 503B compounding pharmacies and typically cost a fraction of the brand-name price. Monthly costs for compounded semaglutide range from $100 to $300, compared to $1,000 or more for brand-name Wegovy without insurance.

Understanding the differences matters. Compounded semaglutide uses the same active ingredient but may differ in formulation, concentration, and added compounds. Some pharmacies add vitamin B12, niacinamide, or other components to their semaglutide compounds. Resources on semaglutide with B12, semaglutide with methylcobalamin, and semaglutide with glycine can help you understand these formulations.

For tirzepatide, compounded options exist as well. The cheapest compounded tirzepatide options and the most affordable tirzepatide alternatives provide detailed pricing breakdowns. Various pharmacies offer compounded tirzepatide with different added ingredients, including formulations with glycine and B12.

Several reputable compounding pharmacies specialize in GLP-1 medications. Detailed reviews exist for providers like Empower Pharmacy for semaglutide, Empower Pharmacy for tirzepatide, Olympia Pharmacy, Belmar Pharmacy, and Red Rock Pharmacy. Each pharmacy has different pricing structures, formulation options, and ordering processes.

Storage and handling matter with compounded medications. Understanding semaglutide refrigeration requirements, shelf life, and expiration ensures you get the full benefit from each vial.

Oral GLP-1 options

Oral formulations represent an emerging alternative to injectable GLP-1 medications. Oral semaglutide drops and sublingual GLP-1 drops offer needle-free administration, which some patients prefer. The sublingual semaglutide guide covers absorption, effectiveness, and proper administration technique.

Tirzepatide also has oral options being explored. The tirzepatide drops and oral versus injectable tirzepatide comparison detail the trade-offs between these delivery methods. Some patients find that tirzepatide tablets offer a more convenient option when injectable formulations are difficult to obtain through insurance.

Manufacturer savings programs

Both Novo Nordisk (maker of Wegovy and Ozempic) and Eli Lilly (maker of Zepbound and Mounjaro) offer savings programs that can reduce out-of-pocket costs for eligible patients. These programs typically require that you have commercial insurance, even if the specific medication is not covered. The savings cards can reduce monthly costs to as low as $25 for qualifying patients, though eligibility requirements and maximum benefit amounts change periodically.

Medicare and Medicaid patients are generally not eligible for manufacturer savings programs. If you have government-sponsored insurance, the alternative pathways described above become more important.

Cash-pay and telehealth options

Direct-pay telehealth platforms have emerged as another pathway to GLP-1 access. These services connect patients with licensed providers who can prescribe compounded GLP-1 medications without insurance involvement. Platforms like Lavender Sky, Lavender Sky for tirzepatide, WeightCare, Direct Meds, and Elevate Health offer various pricing tiers and service levels.

Some services also offer buy-now-pay-later options. The semaglutide Afterpay guide and tirzepatide Afterpay options explain how to spread the cost of medication across multiple payments.

How to check your specific Anthem GLP-1 coverage

Before assuming your plan does or does not cover GLP-1 medications, take these specific steps to verify your coverage status.

Step 1: access your formulary

Log into your Anthem member portal at anthem.com. Navigate to the pharmacy benefits section and look for the drug list or formulary. Search for each GLP-1 medication by both brand name and generic name. The formulary will show which tier each medication falls into and whether prior authorization is required.

Step 2: check your plan benefit document

Your Summary of Benefits and Coverage (SBC) document contains specific language about weight management medication coverage. Look for sections titled "prescription drug coverage," "weight management," or "obesity treatment." Some plans explicitly exclude "anti-obesity medications" or "weight loss drugs" in a separate exclusion section, even if other prescription medications are covered.

Step 3: call Anthem member services

Call the number on the back of your Anthem insurance card and ask specifically about GLP-1 coverage for weight management. Request the prior authorization criteria in writing. Ask whether your plan distinguishes between weight loss coverage and coverage for other GLP-1 indications like cardiovascular risk reduction or sleep apnea. Document the name of the representative, the date, time, and reference number for the call.

Step 4: ask your doctor to run a benefits verification

Your prescribing physician office can often run a real-time benefits check through their pharmacy benefits management system. This check provides the most accurate coverage information for your specific plan, including estimated copay amounts, prior authorization requirements, and any quantity limits or step therapy mandates.

Managing GLP-1 treatment with or without insurance

Regardless of whether Anthem covers your GLP-1 medication, managing the treatment effectively involves understanding dosing, side effects, and lifestyle modifications that support the medication.

Starting your GLP-1 protocol

Whether you access GLP-1 medications through insurance or through alternative channels, the starting process follows similar patterns. The first dose experience varies from person to person, but understanding what to expect helps manage initial side effects. Most protocols start with the lowest available dose and increase gradually over weeks to months.

For semaglutide users, the dosage chart provides the standard titration schedule. Understanding the best time to take semaglutide and optimal injection sites can improve both effectiveness and comfort. If you are using compounded formulations, the reconstitution guide and injection technique guide are essential references.

For tirzepatide users, the dose chart outlines the progression schedule. Resources on injection technique, timing, and thigh injection placement help ensure proper administration.

Managing common side effects

GLP-1 medications share common side effects that can be managed effectively with the right approach. Nausea is the most frequently reported side effect, typically peaking during dose increases and subsiding as your body adjusts. The semaglutide bloating guide and tirzepatide bloating guide provide specific strategies for digestive discomfort.

Constipation affects many GLP-1 users. Detailed management strategies appear in the semaglutide constipation treatment and tirzepatide constipation treatment guides. Other side effects like fatigue, headaches, dizziness, and sulfur burps are covered in dedicated guides that provide practical, evidence-based management strategies.

Hair loss is a concern some patients raise. The GLP-1 hair loss guide addresses whether this is caused by the medication itself or by rapid weight loss, and what you can do about it. Additionally, understanding the vitamin supplementation needs during GLP-1 therapy can help prevent nutritional deficiencies that contribute to side effects.

Nutrition and lifestyle during GLP-1 treatment

What you eat while on GLP-1 medications significantly impacts both your results and your side effect experience. The semaglutide diet plan and tirzepatide diet plan provide meal frameworks designed specifically for patients on these medications.

Understanding which foods to emphasize and which to limit makes a real difference. The best foods for semaglutide and foods to avoid on tirzepatide guides provide practical lists. For meal inspiration, the GLP-1 breakfast ideas collection offers high-protein morning meals that work well with reduced appetite. Protein shakes can also help maintain muscle mass during weight loss.

Supplements play a supporting role. The supplements to take with tirzepatide guide and the best probiotic for semaglutide recommendation help optimize your treatment protocol.

Cost comparison: insurance versus alternative pathways

Understanding the true cost of each pathway helps you make informed decisions about how to access GLP-1 treatment.

Pathway | Monthly cost estimate | Pros | Cons |

|---|---|---|---|

Anthem covered (with insurance) | $25 to $150 copay | Lowest out-of-pocket, brand-name medication, clinical supervision | Prior authorization hassle, step therapy delays, coverage can change |

Manufacturer savings card | $25 to $100 | Brand-name medication, low cost | Requires commercial insurance, may not apply if plan excludes GLP-1 |

Compounded semaglutide | $100 to $300 | No insurance needed, widely available | Not brand-name, quality varies, may lack clinical oversight |

Compounded tirzepatide | $150 to $400 | No insurance needed, dual-agonist benefits | Higher cost than semaglutide compounds, fewer providers |

Cash-pay brand-name | $800 to $1,500 | Identical to insured version | Very expensive, not sustainable long-term for most |

Telehealth platforms | $150 to $500 | Convenient, includes provider visits | Variable quality, limited physical examination |

The peptide cost calculator can help you compare costs across different formulations and providers. For dosing calculations, the semaglutide dosage calculator and the general peptide calculator provide precise measurements for compounded formulations.

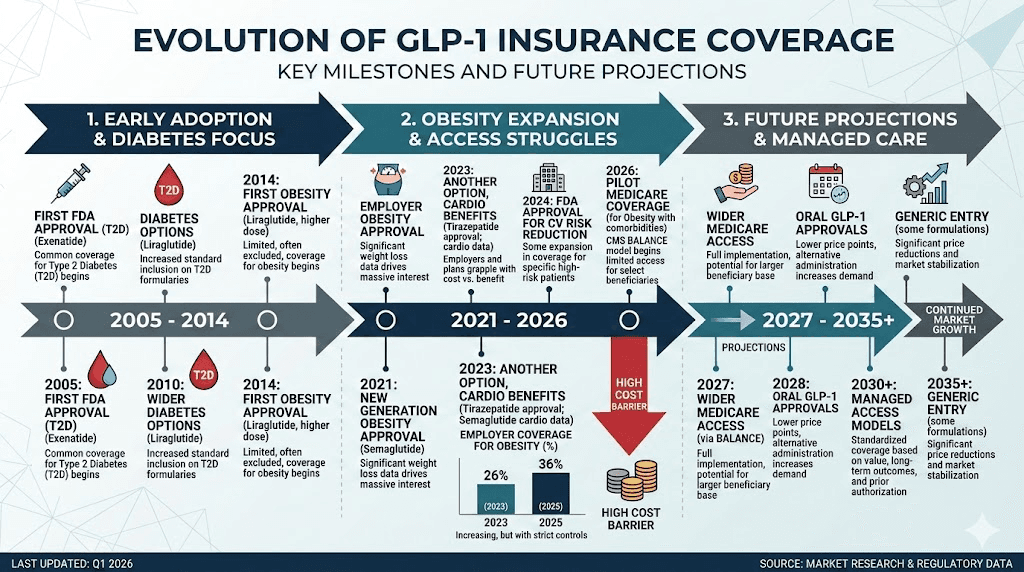

The bigger picture: GLP-1 insurance coverage trends

Understanding the broader insurance landscape helps you anticipate future changes to your coverage and plan accordingly.

Why insurers are pulling back

The cost of GLP-1 medications has created a genuine financial crisis for health insurers and employers. Annual per-patient costs of $12,000 to $16,000 for brand-name GLP-1 medications, combined with the massive number of potentially eligible patients (roughly 42% of American adults have obesity), create projected costs that threaten to destabilize employer health plans. Some estimates suggest that if just 10% of eligible employees started GLP-1 therapy, employer health costs could increase by 15% to 25%.

This financial pressure is driving the coverage rollbacks you see with Anthem and other major insurers. The trend is not unique to Anthem. Blue Cross Blue Shield affiliates across multiple states, UnitedHealthcare, Cigna, and Aetna have all made similar moves to restrict or eliminate GLP-1 weight loss coverage.

What could change

Several factors could shift the coverage landscape in the coming months and years. Generic semaglutide could enter the market as patent protections evolve, potentially reducing costs by 70% to 90%. New GLP-1 medications like retatrutide, survodutide, and CagriSema may offer improved efficacy at competitive prices. State and federal legislation mandating obesity medication coverage is being debated in multiple jurisdictions.

Medicare Part D coverage for GLP-1 weight loss medications is currently excluded, but CMS is exploring pilot programs that could begin as early as 2027. If Medicare starts covering GLP-1s for weight loss, the pressure on commercial insurers like Anthem to follow suit would increase significantly.

Long-term treatment considerations

One important question that affects both insurance coverage and personal planning is how long you need to stay on GLP-1 medication. The duration guide for semaglutide addresses this question in detail. Research shows that many patients regain weight after discontinuing GLP-1 therapy, which raises questions about whether insurance should cover indefinite use.

Understanding what happens when you stop is crucial. The semaglutide withdrawal symptoms guide and tirzepatide tapering guide provide strategies for safely reducing or discontinuing medication. Some patients choose to restart semaglutide after a break, which may require going through the prior authorization process again.

Comparing GLP-1 options when coverage changes

If your Anthem coverage changes, you may need to switch between medications. The semaglutide versus tirzepatide comparison provides a comprehensive head-to-head analysis. The side effect comparison helps you understand what to expect with each option.

Switching between medications requires careful dose conversion. The semaglutide to tirzepatide conversion chart and the switching guide provide the clinical details needed for a smooth transition. If one medication does not work, understanding whether tirzepatide will work when semaglutide does not helps you make informed decisions about next steps.

Working with your healthcare provider for the best outcome

Your doctor plays a crucial role in both getting insurance coverage and managing your GLP-1 treatment effectively. Here is how to optimize that partnership.

Choosing the right provider

Not all doctors are equally experienced with GLP-1 medications or insurance navigation. Obesity medicine specialists, endocrinologists, and weight management clinics typically have more experience with prior authorization processes and know how to document cases in ways that maximize approval chances. General practitioners can prescribe GLP-1 medications, but they may not be as familiar with the specific documentation Anthem requires.

Ask your provider directly whether they have experience with Anthem GLP-1 prior authorizations and appeals. A provider who handles these regularly knows which documentation details Anthem scrutinizes most closely and how to present your case in the strongest possible light.

Documenting your weight loss journey

Start creating a paper trail now, even before you apply for prior authorization. Regular office visits documenting your weight, BMI, blood pressure, and any obesity-related health conditions create the foundation for a strong prior authorization submission. If you are doing dietary counseling, keep records. If you are exercising regularly, document it through your provider.

Track your food intake and physical activity in a structured way. Many insurance reviewers look for evidence of "structured lifestyle intervention" rather than vague statements about "trying to eat better." Specific caloric goals, meal plans, and exercise logs demonstrate the level of effort that Anthem expects to see before approving GLP-1 therapy.

Understanding timing

Knowing how quickly semaglutide works and how quickly tirzepatide works helps set expectations for both you and your insurance company. Most patients notice appetite suppression within the first few weeks, but significant weight loss typically takes 3 to 6 months to become clearly measurable. The first month results vary widely between individuals.

If you are struggling with slow results, the troubleshooting guide for semaglutide and troubleshooting guide for tirzepatide identify the most common reasons for suboptimal outcomes and provide specific fixes. Sometimes the issue is dosage, sometimes timing, and sometimes dietary factors that can be adjusted.

Special situations and additional considerations

Medicare and Medicaid Anthem plans

Medicare Part D currently does not cover GLP-1 medications for weight loss. However, these medications may be covered under Medicare for type 2 diabetes, cardiovascular risk reduction (Wegovy), or obstructive sleep apnea (Zepbound). Anthem Medicare Advantage plans follow CMS guidelines on GLP-1 coverage, with limited flexibility to add benefits beyond what traditional Medicare covers.

Medicaid coverage through Anthem varies by state. Only 13 state Medicaid programs currently cover GLP-1 medications for obesity treatment, and several states have recently pulled back coverage due to budget pressures. If you have Anthem Medicaid coverage, check your specific state program for current eligibility.

Traveling with GLP-1 medications

If you are an Anthem member who travels frequently, understanding how to transport your GLP-1 medication safely is important. The travel guide for tirzepatide and travel guide for semaglutide cover TSA regulations, temperature management during travel, and what to do if your medication gets too warm. Understanding temperature sensitivity and tirzepatide heat exposure effects helps protect your investment in these medications.

Combining GLP-1 with other treatments

Some patients explore combining their GLP-1 medication with other treatments for enhanced results. Common questions include whether you can combine GLP-1s with phentermine and semaglutide or phentermine and tirzepatide. The metformin and tirzepatide combination guide addresses another common question.

Alcohol consumption is a frequent concern. The alcohol and semaglutide guide and alcohol and tirzepatide guide cover safety considerations and practical recommendations.

Women-specific considerations

Several GLP-1 concerns are specific to women. The semaglutide and menstrual changes and tirzepatide and periods guides address hormonal impacts. For women considering pregnancy, understanding GLP-1 use during breastfeeding and tirzepatide during breastfeeding is essential. The effects on sex drive represent another topic that women frequently ask about.

Frequently asked questions

Does Anthem Blue Cross cover Wegovy for weight loss?

Most Anthem commercial plans have excluded Wegovy for weight loss as of recent formulary changes. However, some employer-sponsored plans and state-regulated individual plans may still include coverage. Wegovy remains covered for cardiovascular risk reduction and MASH liver disease under many plans. Check your specific formulary through your Anthem member portal.

What BMI do I need for Anthem to cover a GLP-1 for weight loss?

When coverage exists, Anthem typically requires a BMI of 30 or greater, or a BMI of 27 or greater with at least one weight-related comorbidity such as type 2 diabetes, hypertension, dyslipidemia, or obstructive sleep apnea. The complete BMI requirements guide covers eligibility criteria in detail across different insurers.

How long does Anthem prior authorization take for GLP-1 medications?

Standard prior authorization requests typically receive a response within 5 to 15 business days. Urgent requests must be processed within 72 hours. Your doctor initiates the process by submitting clinical documentation, and you can track the status through your Anthem member portal or by calling member services.

Can I appeal if Anthem denies my GLP-1 prescription?

Yes. You have 180 days to file an internal appeal. Up to 80% of appeals succeed, and you have the right to an external review if the internal appeal is denied. Your doctor should provide updated documentation and a Letter of Medical Necessity addressing the specific reason for denial.

Does Anthem cover compounded semaglutide or tirzepatide?

Generally no. Compounded medications are typically not covered by insurance plans because they are not FDA-approved branded products. However, compounded GLP-1 medications cost significantly less than brand-name versions, making them a viable self-pay alternative. The compounded semaglutide guide covers pricing, sourcing, and quality considerations.

Will Anthem cover Mounjaro if I also have type 2 diabetes?

Yes. Mounjaro (tirzepatide) is generally covered by Anthem for type 2 diabetes management, even when plans exclude GLP-1 coverage for weight loss alone. Your doctor must document the diabetes diagnosis with appropriate lab work (typically HbA1c levels) and show that first-line diabetes medications were tried first. The tirzepatide dosing guide covers the standard diabetes titration schedule.

What happens if I lose my GLP-1 coverage mid-treatment?

If your formulary changes mid-year, your insurer must typically provide 60 days notice. During this transition period, work with your doctor to explore appeal options, alternative covered medications, or one of the cash-pay pathways described in this guide. The weaning off guide covers safe tapering if you need to temporarily discontinue.

Is there a way to get Anthem to cover Zepbound for weight loss?

Direct weight loss coverage for Zepbound is excluded under most Anthem plans. However, if you have documented moderate to severe obstructive sleep apnea alongside obesity, Zepbound may be covered under that indication. Work with your doctor to determine whether a sleep study and formal sleep apnea diagnosis could create a coverage pathway.

How much does a GLP-1 medication cost without Anthem coverage?

Brand-name Wegovy and Zepbound cost approximately $800 to $1,500 per month without insurance. Compounded alternatives range from $100 to $400 per month depending on the medication and pharmacy. The peptide cost calculator helps estimate costs based on your specific dosing needs.

Can my doctor prescribe Ozempic off-label for weight loss through Anthem?

Some doctors do prescribe Ozempic off-label for weight loss, and some Anthem plans may cover this if the diabetes indication criteria are met through the prior authorization process. However, this approach involves ethical and documentation considerations that you should discuss thoroughly with your healthcare provider. If your plan covers Ozempic for diabetes, the dosing chart shows the titration schedule your doctor would follow.

Emerging GLP-1 options and future coverage possibilities

The GLP-1 landscape is evolving rapidly, and emerging alternatives may offer new insurance coverage opportunities. The cagrilintide side effect profile and the cagrilintide weight loss data suggest this amylin analog could offer a complementary or alternative approach to GLP-1 therapy.

Combination therapies continue to show promise. Alternating between semaglutide and tirzepatide is an approach some patients and providers explore, though insurance coverage for such protocols can be challenging to navigate. The retatrutide dosage protocols and purchasing guide provide information on this triple-agonist medication that may eventually receive FDA approval and insurance coverage.

Patch-based delivery through products like Onmorlo could change the insurance coverage equation by offering a different product category that formulary committees may evaluate independently from injectable GLP-1 medications.

External resources

CMS Guide to Health Insurance Appeals, the official government resource for understanding your appeal rights under the Affordable Care Act

Anthem Pharmacy Benefits, the official Anthem portal for checking your formulary and prescription coverage details

The Obesity Action Coalition, a patient advocacy organization providing resources for navigating insurance coverage for anti-obesity medications

FDA Semaglutide Safety Information, the official FDA resource on approved semaglutide medications and safety data

NIDDK Prescription Weight Loss Medications, the National Institutes of Health overview of FDA-approved weight management medications

SeekPeptides members navigate these insurance challenges with confidence because they have access to comprehensive medication guides, dosage calculators, and protocol resources that help them work effectively with their healthcare providers. When you understand the clinical evidence behind your treatment, you can advocate for yourself through prior authorization, appeals, and conversations with your insurance company. Membership gives you the knowledge edge that turns a confusing system into a manageable process.

In case I do not see you, good afternoon, good evening, and good night. May your coverage stay approved, your appeals stay successful, and your health goals stay within reach.