Mar 20, 2026

Some people walk into a pharmacy and pick up their tirzepatide with a $25 copay. Others get a denial letter before the prescription even processes. Same medication. Same insurance company. Completely different outcomes. The difference is not luck. It is not geography. It is not even the specific diagnosis on your chart. The difference comes down to understanding exactly how tirzepatide coverage works within the UnitedHealthcare system, which plan type you carry, and whether your provider knows how to navigate the prior authorization process that determines everything.

UnitedHealthcare is one of the largest health insurers in the United States, covering over 50 million members through employer-sponsored plans, individual marketplace policies, Medicare Advantage, and Medicaid managed care. Their coverage of tirzepatide, the active ingredient in both Mounjaro and Zepbound, depends on a web of factors that most people never think to investigate until they are staring at a four-figure pharmacy bill. This guide breaks down every detail you need, from plan-specific coverage rules to the exact prior authorization criteria UnitedHealthcare uses, the appeal strategies that actually work when you get denied, and the cost-saving alternatives that exist when insurance coverage is not an option. Whether you are exploring tirzepatide for weight management or type 2 diabetes, the information here will save you hundreds or even thousands of dollars.

The short answer on UnitedHealthcare tirzepatide coverage

Yes and no. That is the honest answer, and anyone telling you otherwise is oversimplifying a complicated situation.

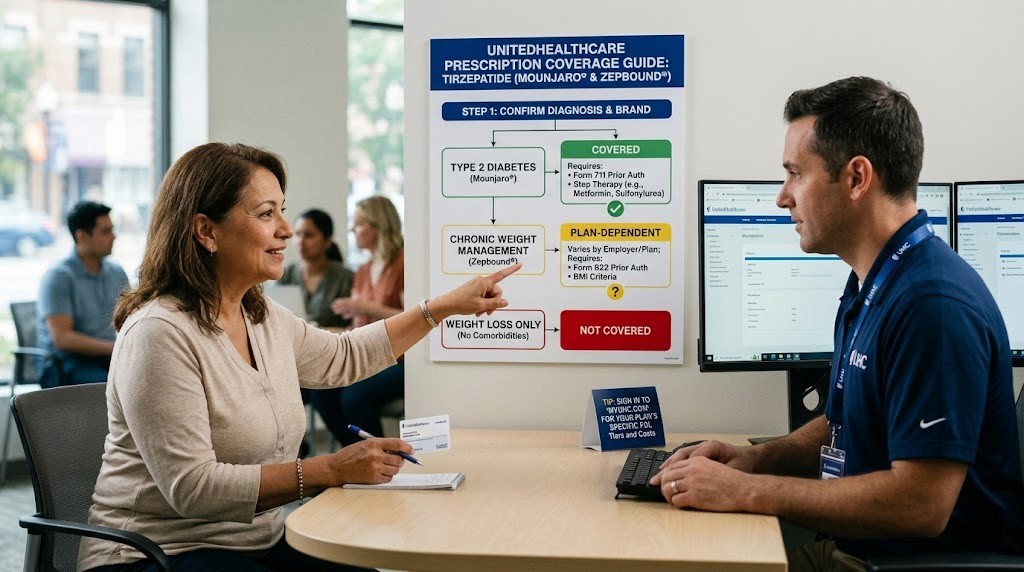

UnitedHealthcare may cover tirzepatide, but coverage depends entirely on three factors: which brand name your provider prescribes, what condition it is being prescribed for, and which specific UnitedHealthcare plan you carry. The same molecule, tirzepatide, is sold under two different brand names for two different FDA-approved indications. Mounjaro is approved for type 2 diabetes. Zepbound is approved for chronic weight management and, more recently, obstructive sleep apnea. Same active ingredient. Very different insurance treatment.

For type 2 diabetes (Mounjaro), most UnitedHealthcare commercial plans provide coverage after prior authorization. The medication typically sits on Tier 2 or Tier 3 of the formulary. Copays range from $25 to $150 per month depending on your specific plan design.

For weight loss (Zepbound), coverage is far more restrictive. Most UnitedHealthcare plans do not cover weight management medications unless the employer specifically elected to include that benefit. Individual and marketplace plans through UHC rarely cover Zepbound at all. Medicare Advantage plans do not cover it for weight loss.

That distinction matters more than anything else in this entire guide.

Understanding tirzepatide brand names and what they mean for coverage

Before diving into specific plan details, you need to understand something that confuses almost everyone. Tirzepatide is not one medication with one purpose. It is one molecule packaged under two brand names, each with its own FDA approval, its own insurance classification, and its own coverage pathway. Getting this wrong at the start can waste months of back-and-forth with your insurance company.

Mounjaro (tirzepatide for type 2 diabetes)

Mounjaro received FDA approval in May 2022 for improving blood sugar control in adults with type 2 diabetes. It works as a dual GIP and GLP-1 receptor agonist, targeting two incretin hormones simultaneously. This dual mechanism makes it more effective than single-target medications like semaglutide for some patients. Because diabetes is classified as a medical condition requiring treatment, insurance coverage for Mounjaro follows standard pharmacy benefit rules. Most commercial plans cover it after prior authorization confirms the diagnosis and previous treatment history.

Zepbound (tirzepatide for weight management)

Zepbound received FDA approval in November 2023 for chronic weight management in adults with a BMI of 30 or greater, or a BMI of 27 or greater with at least one weight-related condition. In late 2024, it also received approval for treating moderate-to-severe obstructive sleep apnea in adults with obesity. The weight management indication creates an insurance problem. Many insurers, including UnitedHealthcare, historically classify obesity medications as "lifestyle" drugs and exclude them from standard pharmacy benefits. This is changing slowly, but the reality today is that Zepbound coverage remains inconsistent across plan types.

Why this distinction matters for your wallet

If your provider prescribes Mounjaro for diabetes, you are working within a system designed to cover that medication. If your provider prescribes Zepbound for weight loss, you are fighting against a system that often excludes it. Understanding which brand name appears on your prescription is the first step toward knowing what your insurance will do.

Some patients with type 2 diabetes who also want weight loss benefits may find that a Mounjaro prescription provides both, since tirzepatide produces significant weight reduction regardless of which brand name is on the label. The molecule does not change. Only the insurance classification does.

UnitedHealthcare coverage by plan type

Not all UnitedHealthcare plans are created equal. The type of plan you carry determines almost everything about your tirzepatide coverage. Here is what to expect from each.

Employer-sponsored large group plans

This is where coverage varies the most. Large employers (typically 100+ employees) that self-fund their health plans through UnitedHealthcare have significant control over what their plan covers. Some employers have added weight management drug benefits. Others have not. For Mounjaro (diabetes), most employer plans cover it through the standard pharmacy benefit with prior authorization. The medication typically falls on Tier 2 or Tier 3, meaning moderate copays. For Zepbound (weight loss), coverage exists only if the employer specifically elected to include anti-obesity medications in their plan design.

The only way to know for certain is to check your specific plan formulary or call the member services number on the back of your insurance card.

Employer-sponsored small group plans

Small group plans (typically under 50 employees) generally follow UnitedHealthcare standard formulary decisions more closely. Mounjaro for diabetes is usually covered. Zepbound for weight loss is usually excluded. Small employers have less flexibility to customize benefits, so if the standard UHC formulary excludes obesity medications, small group members typically cannot access them through insurance.

Individual and ACA marketplace plans

Individual plans purchased through the ACA marketplace or directly from UnitedHealthcare rarely cover tirzepatide for weight loss. ACA essential health benefits do not currently require coverage of anti-obesity medications, so most individual plans exclude them. Mounjaro for diabetes follows standard formulary rules and may be covered with prior authorization.

Medicare Advantage plans

Medicare does not cover medications prescribed specifically for weight loss. This includes Zepbound. However, Mounjaro for type 2 diabetes can be covered under Medicare Part D pharmacy benefits. If you have a UnitedHealthcare Medicare Advantage plan with Part D coverage, Mounjaro may be available through prior authorization for a confirmed diabetes diagnosis.

There is a significant development on the horizon. Starting in April 2026, Medicare and Medicaid may begin covering GLP-1 medications more broadly for obesity-related use under a tentative agreement between Eli Lilly and the US government. If this moves forward, eligible patients could see out-of-pocket costs capped at approximately $50 per month.

Medicaid managed care

Medicaid coverage through UnitedHealthcare varies by state. Some state Medicaid programs cover tirzepatide for diabetes. Very few cover it for weight management. Check your state Medicaid formulary for specific details.

Quick reference: coverage by plan type

Plan Type | Mounjaro (Diabetes) | Zepbound (Weight Loss) | Notes |

|---|---|---|---|

Large Group Employer | Usually covered | Varies by employer | Check your specific formulary |

Small Group Employer | Usually covered | Usually excluded | Less plan customization |

Individual/Marketplace | May be covered | Rarely covered | ACA does not require obesity drug coverage |

Medicare Advantage | Covered via Part D | Not covered | May change in 2026 |

Medicaid | State-dependent | Rarely covered | Check state formulary |

Prior authorization requirements for tirzepatide

Even when your plan covers tirzepatide, you cannot simply walk into a pharmacy and fill the prescription. UnitedHealthcare requires prior authorization for both Mounjaro and Zepbound. This means your healthcare provider must submit documentation to UHC before the prescription can be processed. The requirements differ depending on which medication and indication.

Mounjaro prior authorization criteria (type 2 diabetes)

For Mounjaro approval, UnitedHealthcare generally requires the following. A confirmed diagnosis of type 2 diabetes mellitus. Evidence that the patient has tried and failed, or cannot tolerate, first-line treatments. This typically means metformin, sulfonylureas, or basal insulin. A BMI of 25 or higher. Regular follow-up monitoring documented in medical records.

UnitedHealthcare considers tirzepatide a second-line or third-line option for diabetes management. Your provider will need to show that less expensive medications did not achieve adequate glycemic control before moving to Mounjaro. This is standard step therapy, and most endocrinologists are familiar with the documentation requirements.

Zepbound prior authorization criteria (weight management)

When a plan does cover Zepbound for weight loss, the prior authorization criteria are more stringent. According to UHC Policy P 1475-1, the requirements include BMI of 30 or greater, or BMI of 27 or greater with at least one comorbidity such as diabetes, hypertension, sleep apnea, or high cholesterol. The patient must be 16 years of age or older. There must be evidence of lifestyle changes including diet, exercise, and behavioral support. Enrollment in a weight management program is required.

One important distinction sets UnitedHealthcare apart from some other insurers. UHC does not require step therapy for Zepbound. You do not need to try and fail on Wegovy or Saxenda before getting Zepbound approved. This removes a significant barrier that exists with other insurance companies.

Initial approval lasts six months. Renewals require documented weight loss of at least 5% from baseline.

How long does prior authorization take?

Processing times vary. Electronic prior authorizations submitted through UnitedHealthcare automated systems can process in as little as 29 seconds. Standard submissions take 1 to 3 business days. Traditional paper or fax submissions may take 1 to 2 weeks. Urgent requests are processed within 72 hours.

If you are waiting for approval and already have a tirzepatide protocol planned, ask your provider to submit electronically whenever possible. The time difference is significant.

The sleep apnea coverage pathway

Here is something most people do not know about. Even if your UnitedHealthcare plan excludes weight loss medications, there may be a pathway to coverage through a sleep apnea diagnosis.

Zepbound received FDA approval for moderate-to-severe obstructive sleep apnea in adults with obesity. This creates an alternative coverage route because sleep apnea is a medical condition, not a lifestyle concern. When prescribed for sleep apnea rather than weight loss, Zepbound may fall under medical necessity criteria that bypass the weight management exclusion.

Sleep apnea pathway requirements

To qualify through this pathway, you generally need a documented diagnosis of moderate-to-severe obstructive sleep apnea with an AHI (Apnea-Hypopnea Index) greater than 15. A BMI of 30 or greater. Documentation showing CPAP failure or inability to tolerate CPAP therapy. Involvement of a sleep specialist in your care. An A1C of 6.5% or lower, confirming you do not have diabetes (since that would route you to Mounjaro instead).

This pathway became available through UnitedHealthcare starting July 2025. If you have been diagnosed with sleep apnea and your plan excludes weight loss drugs, this is worth discussing with your provider. Many people with obesity have undiagnosed sleep apnea, so a sleep study could open a door to coverage you did not know existed.

Cost of tirzepatide with UnitedHealthcare insurance

When coverage is approved, your out-of-pocket cost depends on your plan design, formulary tier, and whether you use any available savings programs.

Formulary tier and copay structure

Mounjaro typically sits on Tier 2 or Tier 3 of UnitedHealthcare formularies. Tier 2 copays generally range from $25 to $75 per month. Tier 3 copays range from $75 to $150 per month. Some plans use coinsurance instead of fixed copays, meaning you pay a percentage of the drug cost rather than a flat amount.

Zepbound, when covered, usually lands on the specialty tier. Specialty tier medications often carry higher cost-sharing requirements, sometimes 20% to 30% coinsurance with a cap. The exact amount depends entirely on your plan design.

Manufacturer savings programs

Eli Lilly offers savings cards for both Mounjaro and Zepbound that can dramatically reduce your copay. If you have commercial (non-government) insurance and meet the eligibility criteria, the Lilly Savings Card can reduce your copay to as low as $25 per month for up to 12 fills per year. This applies even if your insurance places the medication on a high-cost tier.

The savings card does not work with government insurance programs like Medicare, Medicaid, or Tricare. It also requires that your insurance covers the medication, even partially. If your plan excludes tirzepatide entirely, the savings card cannot help.

OptumRx and pharmacy processing

UnitedHealthcare uses OptumRx as its pharmacy benefit manager. For 2026, OptumRx is maintaining Zepbound on formularies for plans that cover obesity medications. Your prescription will process through OptumRx, and you can use their mail-order pharmacy for potential additional savings.

If you are comparing tirzepatide costs against semaglutide options, the insurance dynamics are similar. Both require prior authorization, and both have brand-name pricing that makes insurance coverage critical for affordability.

Cost of tirzepatide without insurance

If UnitedHealthcare does not cover your tirzepatide prescription, the out-of-pocket cost is substantial. Understanding the full pricing landscape helps you evaluate whether to pursue insurance coverage aggressively or explore alternatives.

Brand-name list prices

Mounjaro carries a list price of $1,079.77 for a 28-day supply. Zepbound lists at $1,086.37 for the same period. These prices are consistent across all doses, from the lowest 2.5mg starting dose through the maximum 15mg dose. At full list price, a year of tirzepatide costs over $13,000.

LillyDirect self-pay options

Eli Lilly launched the Zepbound Self-Pay Journey Program, offering single-dose vials through their LillyDirect platform at significantly reduced prices. The 2.5mg and 5mg doses start at $299 per month. The 7.5mg dose costs $599. The 10mg, 12.5mg, and 15mg doses cost $699. Refills that occur 45 days prior to delivery reduce 7.5mg and 10mg doses to $499 per month.

These vials require syringe-based injection rather than the auto-injector pen format. If you are comfortable with that process, the savings compared to list price are considerable.

Compounded tirzepatide

Compounded versions of tirzepatide are available through telehealth providers and compounding pharmacies at $299 to $399 per month, representing 60% to 70% savings compared to brand-name list pricing. However, compounded tirzepatide is not FDA-approved, and insurance will not cover it. The quality can vary between compounding pharmacies, so sourcing matters significantly. If you are considering this route, understanding proper reconstitution and storage requirements is essential.

Cost comparison at a glance

Option | Monthly Cost | Annual Cost | Notes |

|---|---|---|---|

Brand with insurance + savings card | $25-$150 | $300-$1,800 | Requires coverage + Lilly card |

Brand with insurance (no card) | $75-$300 | $900-$3,600 | Tier-dependent copay/coinsurance |

LillyDirect self-pay | $299-$699 | $3,588-$8,388 | Vial format, dose-dependent |

Compounded | $299-$399 | $3,588-$4,788 | Not FDA-approved |

Brand at list price | $1,080-$1,086 | $12,960-$13,032 | Without any coverage or discounts |

How to get tirzepatide approved by UnitedHealthcare

Getting your tirzepatide prescription approved requires preparation. Most denials happen because of incomplete documentation, not because the patient does not qualify. Here is how to maximize your chances of approval on the first attempt.

Step 1: Verify your coverage before the appointment

Call the member services number on the back of your UnitedHealthcare insurance card. Ask three specific questions. First, is tirzepatide (either Mounjaro or Zepbound) on your plan formulary? Second, what tier is it on? Third, what are the specific prior authorization criteria for your plan? Write down the answers, including the name of the representative and the date of the call. This information helps your provider tailor the prior authorization submission to your plan requirements.

Step 2: Prepare your documentation

Before your provider submits the prior authorization, make sure your medical record includes everything UnitedHealthcare wants to see. A current BMI measurement taken within the last 30 days. Documentation of comorbidities if applicable, such as diabetes, hypertension, sleep apnea, or hormonal conditions. A history of weight management attempts including diet, exercise, and any previous medications. Lab results showing relevant biomarkers like A1C, fasting glucose, and lipid panels. For diabetes, documentation of previous medication trials and their outcomes.

Step 3: Request a letter of medical necessity

Ask your healthcare provider to include a letter of medical necessity with the prior authorization submission. This letter should explain why tirzepatide is specifically necessary for your condition, why alternative treatments are insufficient, and what clinical outcomes are expected. A strong letter of medical necessity significantly increases approval rates, especially for weight management indications where coverage is less automatic.

Step 4: Submit electronically

Electronic submissions through UnitedHealthcare automated systems process in as little as 29 seconds to 72 hours. Paper or fax submissions can take 1 to 2 weeks. Always ask your provider to submit electronically. The faster turnaround means you can address any issues or denials more quickly.

Step 5: Follow up actively

Do not assume no news is good news. Follow up with both your provider and UnitedHealthcare within 3 business days of submission. Ask for the status of the prior authorization and whether any additional documentation is needed. Proactive follow-up catches problems early and prevents unnecessary delays.

What to do if UnitedHealthcare denies your tirzepatide coverage

Denial is not the end. It feels like it. You open the letter, read the word "denied," and your stomach drops. But here is what the data shows: over 65% of tirzepatide insurance appeals succeed. In some studies, 83.2% of appeals resulted in either partial or full overturn of the initial denial. Those numbers should give you hope.

Common denial reasons

Understanding why UnitedHealthcare denied your claim is the first step toward overturning it. The most common reasons include plan exclusion, where your specific plan does not cover weight management medications at all. Incomplete documentation, where the prior authorization submission was missing required information. Non-compliance with step therapy, where UHC wanted evidence of trying less expensive medications first, though this is less common with UHC for tirzepatide specifically. Failure to meet medical necessity criteria, where the submitted documentation did not demonstrate that tirzepatide was medically necessary for your condition. Off-label use, where the prescription was written for an indication not covered by your plan.

Each denial reason requires a different response strategy. A plan exclusion is harder to overturn than missing documentation. Read your denial letter carefully. UnitedHealthcare is required to explain exactly why the claim was denied and what your appeal rights are.

Types of denials

Not all denials are the same. A "hard" denial based on a plan exclusion means your plan literally does not cover the category of medication. Appealing this type of denial is difficult because it is a plan design issue, not a medical necessity question. A "soft" denial based on insufficient documentation or unmet criteria is much more likely to succeed on appeal because you can provide the missing information.

If your denial is plan-based, your energy may be better spent exploring alternative options rather than fighting the appeal. If your denial is documentation-based, the appeal process is your best path forward.

The appeal process step by step

UnitedHealthcare provides two levels of internal appeal and an external review option. Here is exactly how to navigate each.

Internal appeal (first level)

You have 180 days from the denial date to file an internal appeal. Your healthcare provider should submit a formal appeal letter that directly addresses the specific denial reason. Include all documentation that was part of the original prior authorization plus any additional evidence. Attach scanned copies of chart notes, medication history, weight and BMI logs, lab results, and any supporting documents like a sleep study. If a letter of medical necessity was not included originally, include one now. This is often the single most impactful addition to an appeal.

UnitedHealthcare must respond to internal appeals within 30 days for non-urgent requests. Urgent appeals receive a response within 72 hours.

Internal appeal (second level)

If the first internal appeal is denied, you can file a second-level appeal. This is reviewed by a different team than the first appeal. Include any new evidence or documentation that has become available since the first appeal. A stronger letter of medical necessity with additional clinical justification can make a difference at this stage.

External review

If both internal appeals fail, you have 4 months to request an external review by an independent review organization. This is a completely independent evaluation by reviewers who do not work for UnitedHealthcare. External reviews carry significant weight because the decision is binding on the insurance company. If the external review approves your claim, UnitedHealthcare must cover the medication.

Tips that increase appeal success rates

Get your provider invested. Appeals written by motivated physicians who provide detailed clinical justification succeed at much higher rates than form letters. Include peer-reviewed literature supporting the use of tirzepatide for your specific condition. Reference specific studies, clinical trial data, and FDA labeling information. If applicable, document that you have tried and failed other treatments, including lifestyle modifications, other medications, and behavioral programs.

Keep records of everything. Every phone call, every letter, every submission. Note the date, time, representative name, and what was discussed. This documentation protects you throughout the process and is essential if you escalate to external review.

Alternatives when insurance does not cover tirzepatide

Sometimes, despite your best efforts, insurance coverage is simply not available. Maybe your plan excludes obesity medications. Maybe your employer chose not to add that benefit. Maybe you are on Medicare and the new coverage has not started yet. Whatever the reason, you still have options.

Compounded tirzepatide

Compounded tirzepatide from reputable pharmacies costs $299 to $399 per month, a fraction of brand-name pricing. Multiple telehealth platforms offer compounded tirzepatide with dosage guidance included. The tradeoff is that compounded versions are not FDA-approved, and quality varies between pharmacies. If you go this route, research the compounding pharmacy thoroughly. Look for pharmacies that are 503B-registered, which means they operate under stricter manufacturing standards.

Several reputable providers offer compounded tirzepatide, including pharmacies reviewed in our guides on Empower Pharmacy, Boothwyn Pharmacy, Southend Pharmacy, and ProRx. Each has different pricing structures, formulations, and dosing options.

LillyDirect self-pay program

Eli Lilly sells Zepbound directly through their LillyDirect platform in single-dose vial format. Starting prices are $299 per month for the lowest doses. This is brand-name, FDA-approved tirzepatide without needing insurance. The vials require you to draw up your own injection rather than using a pre-filled pen, but the cost savings are meaningful.

Switching to a covered alternative

If tirzepatide is not covered but other GLP-1 medications are, your provider might consider an alternative. Semaglutide is available as Wegovy (weight loss) and Ozempic (diabetes), and some UnitedHealthcare plans cover these even when they exclude tirzepatide. The switch between tirzepatide and semaglutide requires dosage adjustment and monitoring, but it is a viable path when insurance drives the decision.

Other alternatives include phentermine, which is inexpensive but less effective and has more restrictions on long-term use, and liraglutide (Saxenda), which some plans cover when they exclude newer agents.

Open enrollment plan changes

If you know you want tirzepatide coverage and your current plan excludes it, open enrollment is your opportunity to switch. Review available plans specifically for their obesity medication coverage. Look at the formulary before enrolling. Some UnitedHealthcare plans explicitly cover anti-obesity medications while others in the same product line do not. The difference in premium may be worth the medication coverage.

Employer advocacy

For those on employer-sponsored plans, talking to your HR department about adding weight management drug coverage can make a difference, especially if multiple employees are interested. Self-funded employers can modify their plan design at any time. The growing body of evidence showing that GLP-1 medications reduce healthcare costs long-term is making more employers willing to add this benefit.

Compounded tirzepatide as a cost-effective option

For many people denied insurance coverage, compounded tirzepatide becomes the most practical path forward. Understanding what compounded tirzepatide is, how it differs from brand-name versions, and what to look for when choosing a source is critical for making an informed decision.

What is compounded tirzepatide?

Compounded tirzepatide is the same active molecule prepared by a compounding pharmacy rather than manufactured by Eli Lilly. Compounding pharmacies can legally prepare tirzepatide when there is a documented shortage of the brand-name product or when a patient needs a specific formulation not commercially available. The FDA has maintained tirzepatide on its drug shortage list intermittently, which has allowed compounding to continue.

Compounded versions come in various formats. Injectable vials requiring reconstitution are the most common. Some pharmacies offer sublingual drops or orally disintegrating tablets as alternative delivery methods. Each format has different bioavailability profiles, so dosing does not translate directly between formats.

Cost comparison: compounded vs brand

Brand-name tirzepatide costs $1,080 or more per month at list price. Compounded versions typically cost $299 to $399 per month. That is a savings of $700 to $780 every month, or $8,400 to $9,360 per year. For many people, this cost difference is the deciding factor.

Quality considerations

Not all compounding pharmacies are equal. 503B outsourcing facilities operate under FDA oversight and must follow current good manufacturing practices. 503A pharmacies operate under state pharmacy board oversight with less rigorous manufacturing requirements. When choosing a compounding pharmacy, look for 503B registration, third-party testing of products, and a track record of quality. Grey market sources should be avoided entirely due to quality and safety concerns.

Proper storage is essential regardless of the source. Compounded tirzepatide must be refrigerated and used within the timeframe specified by the compounding pharmacy. Understanding how long compounded tirzepatide can be out of the fridge is important for maintaining potency and safety.

Combination formulations

One advantage of compounded tirzepatide is the ability to create combination formulations not available commercially. Compounding pharmacies can prepare tirzepatide combined with vitamin B12, glycine, niacinamide, or levocarnitine. These combinations may offer additional benefits, though the evidence for enhanced efficacy over tirzepatide alone varies.

SeekPeptides provides detailed guides on each of these combination formulations, helping members understand the evidence behind each additive and make informed decisions about which formulation best fits their goals.

Savings programs and manufacturer discounts

Even if your insurance covers tirzepatide, the copay or coinsurance amount might still be more than you want to pay. Several savings programs exist that can reduce your cost significantly.

Eli Lilly Savings Card

The Lilly Savings Card is the most impactful program for commercially insured patients. If you have commercial insurance that covers Mounjaro or Zepbound, the savings card can reduce your copay to as low as $25 per month. The card covers up to 12 fills per year. Eligibility requires commercial (non-government) insurance. You can apply through the Mounjaro or Zepbound websites.

Important note: the savings card requires that your insurance covers the medication at least partially. If your plan excludes tirzepatide entirely, the savings card will not bridge the gap.

Zepbound Self-Pay Journey Program

For patients without insurance coverage, Lilly offers Zepbound in single-dose vial format through LillyDirect at reduced pricing. This is not a discount card. It is a separate product offering at a lower price point. The 2.5mg and 5mg vials cost $299 per month. Higher doses cost $499 to $699 per month with certain refill discounts applied.

Patient assistance programs

Eli Lilly offers the Lilly Cares Patient Assistance Program for uninsured or underinsured patients who meet income requirements. This program can provide Mounjaro or Zepbound at no cost for qualifying individuals. Income thresholds and other eligibility criteria apply. Applications are submitted through your healthcare provider.

Pharmacy discount programs

GoodRx, RxSaver, and similar pharmacy discount programs can sometimes reduce the cash price of brand-name tirzepatide, though the discounts on specialty medications like Mounjaro and Zepbound are typically modest compared to what savings cards or patient assistance programs offer.

How UnitedHealthcare compares to other insurers

Understanding how UHC stacks up against other major insurers for tirzepatide coverage helps you evaluate whether switching plans might be worthwhile. It also provides context if you are choosing between insurance options during open enrollment.

UnitedHealthcare vs Anthem/Elevance

Anthem (now Elevance Health) has taken a somewhat more progressive approach to GLP-1 coverage for weight loss in certain markets. Some Anthem plans cover Zepbound without the same employer opt-in requirement that UHC uses. However, Anthem often requires step therapy, meaning you must try and fail on another GLP-1 before accessing tirzepatide. UHC does not require step therapy for Zepbound, which is an advantage when coverage is available.

UnitedHealthcare vs Cigna

Cigna coverage of tirzepatide follows a similar pattern to UHC. Employer-sponsored plans have the most flexibility, individual plans rarely cover weight loss medications, and prior authorization is required. Cigna uses Express Scripts as its pharmacy benefit manager, and formulary placement can differ from UHC OptumRx formularies.

UnitedHealthcare vs Aetna/CVS Caremark

Aetna uses CVS Caremark for pharmacy benefits. In early 2026, CVS Caremark made headlines by removing Zepbound from some formularies, affecting Aetna members. This highlights the importance of checking your specific formulary annually, as coverage can change between plan years.

UnitedHealthcare vs Blue Cross Blue Shield

BCBS plans vary dramatically by state because each Blue Cross Blue Shield affiliate operates independently. Some BCBS plans have robust GLP-1 coverage. Others exclude weight loss medications entirely. Comparing BCBS to UHC requires comparing your specific BCBS plan to your specific UHC option.

Key insurer comparison

Insurer | Step Therapy Required? | Employer Opt-in for Weight Loss? | Sleep Apnea Pathway? |

|---|---|---|---|

UnitedHealthcare | No | Yes | Yes (July 2025+) |

Anthem/Elevance | Often yes | Varies | Varies |

Cigna | Varies | Yes | Varies |

Aetna/CVS | Varies | Yes | Varies |

BCBS | Varies by state | Varies by state | Varies by state |

Medicare and Medicaid coverage changes on the horizon

The landscape for tirzepatide insurance coverage is evolving rapidly, especially for government programs. If you are on Medicare or Medicaid, these developments could change your access to tirzepatide significantly.

Medicare coverage expansion

Historically, Medicare has not covered medications prescribed for weight loss. The Treat and Reduce Obesity Act and similar legislative efforts have sought to change this for years. A tentative agreement between Eli Lilly and the US government could bring broader Medicare coverage for GLP-1 medications including tirzepatide starting in April 2026. Under this agreement, eligible patients may see out-of-pocket costs capped at approximately $50 per month.

This change, if finalized, would affect millions of Medicare beneficiaries who currently have no pathway to covered tirzepatide for weight management. UnitedHealthcare Medicare Advantage members would benefit directly from this expansion.

Medicaid expansion

Several states are expanding Medicaid coverage of anti-obesity medications. States that use UnitedHealthcare as a Medicaid managed care organization may begin covering tirzepatide for weight management as state formularies update. Check your state Medicaid program for the most current information.

The broader trend

The insurance industry is slowly acknowledging that obesity is a chronic medical condition requiring treatment, not a lifestyle choice. As more clinical data demonstrates that GLP-1 medications produce sustained weight loss and reduce obesity-related comorbidities, coverage is expanding. This does not help you today if your plan excludes coverage. But it means the situation is improving year over year.

Understanding your UnitedHealthcare formulary

Your UnitedHealthcare formulary is the list of medications your plan covers and the tier each medication sits on. Knowing how to read and use your formulary can save you significant time and money when pursuing tirzepatide coverage.

How to find your formulary

Log into your UnitedHealthcare member portal at myuhc.com. Navigate to pharmacy benefits and search for your prescription drug list. You can also call the number on your insurance card and ask for your formulary to be mailed or emailed. OptumRx also maintains searchable formulary tools through their website and mobile app.

Understanding formulary tiers

UnitedHealthcare formularies typically have 4 to 6 tiers. Tier 1 covers generic medications with the lowest copays. Tier 2 covers preferred brand-name medications. Tier 3 covers non-preferred brand-name medications. Tier 4 and above cover specialty medications with the highest cost-sharing. Mounjaro typically appears on Tier 2 or Tier 3. Zepbound, when covered, may appear on the specialty tier.

Formulary exclusions

If tirzepatide does not appear on your formulary at all, it means your plan explicitly excludes it. This is different from the medication appearing on a high tier. An excluded medication has no coverage pathway through standard pharmacy benefits, though appeal processes and formulary exceptions may still be available in limited circumstances.

Formulary changes

Formularies can change annually during plan renewals. They can also change mid-year in some cases. If your formulary excluded tirzepatide this year, check again during the next plan year. Coverage decisions evolve as more clinical evidence accumulates and as employer demand for GLP-1 medications increases.

Tirzepatide dosing and what insurance covers

Insurance coverage applies to the medication regardless of dose, but understanding the tirzepatide dosing schedule is important because dose escalation affects both clinical outcomes and long-term cost.

Standard dosing protocol

Tirzepatide starts at 2.5mg weekly for the first 4 weeks. The dose then increases to 5mg weekly. Further escalation proceeds in 2.5mg increments at 4-week intervals based on tolerability and response, up to a maximum of 15mg weekly.

Insurance covers the medication at whatever dose your provider prescribes, as long as prior authorization is maintained. The cost per fill is the same regardless of dose for brand-name products. A 2.5mg pen costs the same as a 15mg pen at the pharmacy level. Where dosing matters for cost is in the compounded space, where higher concentrations may cost more.

Dose-related coverage considerations

Some insurance companies require updated prior authorization when moving to higher doses. UnitedHealthcare generally approves the full dose range once initial prior authorization is granted, but check with your provider to confirm. If your plan requires a new authorization for dose escalation, your provider should submit it before you run out of your current dose to avoid gaps in treatment.

Understanding your dosage in units helps you verify that your pharmacy is dispensing the correct product. Each dose corresponds to a specific pen or vial configuration, and errors, while rare, can happen. Knowing that 20 units equals a specific mg amount allows you to double-check your prescription against what the pharmacy dispenses.

Managing side effects while navigating insurance

Insurance coverage does not just apply to the medication itself. Understanding how side effects affect your treatment plan, and therefore your ongoing coverage, matters for maintaining continuous access.

Common side effects and their insurance implications

The most common tirzepatide side effects include nausea, diarrhea, constipation, and decreased appetite. These typically improve over the first few weeks of treatment and often resolve with dose adjustments. From an insurance perspective, side effects matter because dose adjustments or treatment interruptions can complicate ongoing prior authorizations.

If side effects require you to stop tirzepatide temporarily and restart later, you may need a new prior authorization. Communicate with your provider about any side effects so they can document them properly. Good documentation protects your future coverage by showing that treatment decisions are medically appropriate.

Side effects that may require additional treatment

Some side effects, such as headaches, body aches, insomnia, or bloating, may require supportive treatments that are usually covered under your standard medical benefits. Over-the-counter remedies like anti-nausea medication are not covered but are inexpensive. Prescription supportive medications would go through standard pharmacy benefits separate from your tirzepatide coverage.

Renewal and continued coverage

UnitedHealthcare requires renewal of tirzepatide prior authorization, typically every 6 to 12 months depending on the plan. For Zepbound renewals, you must demonstrate at least 5% weight loss from baseline. Your provider needs to document this at each renewal point. If you have not achieved the required weight loss, the renewal may be denied. Work with your provider to ensure your progress is documented at every visit, not just at renewal time.

For Mounjaro diabetes renewals, continued documentation of glycemic management, typically through A1C levels, is required. As long as the medication is contributing to diabetes control, renewals are generally straightforward.

Special situations and coverage exceptions

Certain situations create unique coverage considerations that do not fit neatly into standard prior authorization pathways.

Pregnancy and breastfeeding

Tirzepatide is not approved for use during pregnancy or breastfeeding. If you become pregnant while on tirzepatide, coverage will end because the medication is contraindicated. If you are planning pregnancy, discuss timing with your provider. Tirzepatide and breastfeeding is a topic many women have questions about, and understanding the timeline for stopping before conception is important for both health and insurance continuity.

Switching between tirzepatide brands

If you are on Mounjaro for diabetes and want to switch to Zepbound for weight management, or vice versa, a new prior authorization is required. The switch is not automatic even though the active ingredient is identical. Your provider must submit documentation supporting the new indication. This situation sometimes arises when patients achieve diabetes remission on Mounjaro but want to continue tirzepatide for weight maintenance under Zepbound coverage.

Traveling with tirzepatide

Insurance coverage does not change when you travel domestically, but filling prescriptions at out-of-network pharmacies may affect your copay. If you travel frequently, mail-order pharmacy through OptumRx can ensure consistent supply. For international travel, check whether your plan provides any coverage for prescription fills abroad, though most do not for specialty medications.

Switching from semaglutide to tirzepatide

If you are currently on semaglutide and considering tirzepatide, the insurance process starts fresh. A new prior authorization is needed for tirzepatide even if semaglutide was previously approved. Your provider should document why the switch is necessary, whether due to inadequate response, side effects, or clinical preference. The dosage conversion between semaglutide and tirzepatide requires careful adjustment, and your provider should outline this in the prior authorization to demonstrate appropriate clinical management.

Working with your healthcare provider

Your healthcare provider plays a critical role in whether your tirzepatide coverage gets approved. Not all providers are equally experienced with the insurance side of prescribing GLP-1 medications.

Choosing the right provider

Endocrinologists and obesity medicine specialists typically have the most experience navigating tirzepatide prior authorizations. They know what documentation UnitedHealthcare requires, how to write effective letters of medical necessity, and how to handle appeals. Primary care physicians can also prescribe tirzepatide but may be less familiar with the insurance process for newer specialty medications.

What to ask your provider

Before your appointment, prepare these questions. Have they prescribed tirzepatide before through UnitedHealthcare? Are they familiar with the prior authorization process? Will they write a letter of medical necessity? Will they handle the appeal if coverage is denied? How quickly does their office submit prior authorizations?

A provider who is proactive about the insurance process can mean the difference between a 3-day approval and a month-long battle.

Documentation your provider needs from you

Help your provider help you. Bring your complete weight history, including any documented weight loss attempts. Bring records of any weight management programs, gym memberships, or nutritional counseling. Bring lab results showing obesity-related conditions. If you have a sleep study showing sleep apnea, bring that too. The more comprehensive the documentation package, the stronger the prior authorization submission.

SeekPeptides members access comprehensive guides on tirzepatide dosing protocols, dietary guidelines, and supplement recommendations that complement the clinical information your provider manages.

Real-world coverage scenarios

Abstract coverage rules become clearer with concrete examples. Here are common scenarios UnitedHealthcare members encounter when seeking tirzepatide coverage.

Scenario 1: Type 2 diabetes with employer plan

Sarah has type 2 diabetes and a UnitedHealthcare employer-sponsored plan. She tried metformin for 6 months without achieving her target A1C. Her endocrinologist submitted a prior authorization for Mounjaro. The authorization was approved within 48 hours. With the Lilly Savings Card, her copay dropped to $25 per month. This is the most straightforward coverage scenario.

Scenario 2: Weight management with employer plan (coverage included)

Marcus has a BMI of 34 with hypertension. His employer added anti-obesity medication coverage to their UnitedHealthcare plan. His provider submitted a prior authorization for Zepbound with documentation of his BMI, hypertension diagnosis, and participation in a weight management program. The authorization was approved. With the Lilly Savings Card, he pays $25 per month. Not everyone is this fortunate, but it illustrates what is possible when the employer includes the benefit.

Scenario 3: Weight management with employer plan (coverage excluded)

Jennifer has a BMI of 32 with sleep apnea. Her employer UnitedHealthcare plan excludes weight loss medications. Her initial Zepbound prior authorization was denied based on plan exclusion. However, her provider resubmitted through the sleep apnea pathway, documenting her moderate-to-severe OSA, CPAP failure, and BMI. The resubmission was approved under the medical necessity criteria for sleep apnea treatment. She now pays her standard specialty tier copay.

Scenario 4: Individual marketplace plan

David has a UnitedHealthcare marketplace plan. His plan does not cover weight loss medications. He does not have diabetes or sleep apnea. After a denial and failed appeal, he enrolled in the Zepbound Self-Pay Journey Program through LillyDirect and pays $299 per month for the 2.5mg dose. As his dose escalates, his cost will increase, but it remains significantly below the $1,086 list price.

Scenario 5: Medicare Advantage member

Robert has a UnitedHealthcare Medicare Advantage plan with Part D coverage. He has type 2 diabetes. Mounjaro was approved through Part D with prior authorization. He pays his Part D copay. He also has obesity but cannot access Zepbound for weight loss through Medicare. He is watching the potential Medicare expansion in 2026 closely.

The billing side: CPT codes and claims

Understanding the billing mechanics behind tirzepatide coverage can help you catch errors and avoid unexpected charges.

Pharmacy vs medical benefit

Tirzepatide is typically covered under pharmacy benefits, meaning it processes through your pharmacy plan (OptumRx for UnitedHealthcare) rather than your medical plan. However, some plans cover injectable medications like tirzepatide under the medical benefit, especially for in-office administration. If your pharmacy claim is denied, ask your provider whether submitting under medical benefits might be an option.

CPT codes

If tirzepatide is administered in a clinical setting and billed under medical benefits, the appropriate CPT codes for tirzepatide must be used. Incorrect coding is a common reason for claim denials. Ensure your provider billing staff is familiar with the current codes for tirzepatide injection.

Checking your claims

After each fill, review your explanation of benefits (EOB) from UnitedHealthcare. Verify that the correct medication, quantity, and price appear. Check that your copay or coinsurance matches what you were quoted. If anything looks wrong, contact UnitedHealthcare member services immediately. Claims errors are more common with specialty medications than with standard prescriptions.

Planning for long-term tirzepatide use

Tirzepatide is intended for long-term use. Both diabetes management and weight management require ongoing treatment. Planning for the long term means thinking beyond your first prescription fill.

Annual plan changes

Review your UnitedHealthcare plan during every open enrollment period. Formularies change. Copay structures change. Employer benefit elections change. A plan that covers tirzepatide this year might not cover it next year, and vice versa. Check your formulary proactively rather than finding out at the pharmacy counter.

Prior authorization renewals

Set calendar reminders for prior authorization renewal dates. Do not wait until your prescription is due to discover that your authorization has expired. Submit renewals 30 to 60 days before expiration to ensure continuous coverage without gaps.

Documenting your progress

Keep a personal record of your weight, lab results, and any improvements in comorbidities. This documentation supports prior authorization renewals and appeals. If you are using tirzepatide for weight management, tracking your first month results and ongoing before and after progress provides concrete evidence for insurance renewals.

What happens if coverage changes mid-treatment

If your UnitedHealthcare plan drops tirzepatide coverage mid-year, you have several options. A formulary exception request asks UHC to continue covering the medication despite the formulary change, based on medical necessity. Transitional supply rules may allow a short-term fill (typically 30 days) to bridge the gap while you arrange alternatives. Switching to a covered alternative like semaglutide may be necessary if the formulary change is permanent.

For researchers serious about optimizing their peptide protocols, SeekPeptides offers the most comprehensive resource available, with evidence-based guides, proven protocols, and a community of thousands who have navigated these exact questions. SeekPeptides members get access to detailed tirzepatide diet plans, meal plans, and injection timing guidance that maximize results while on treatment.

Frequently asked questions

Does UnitedHealthcare cover Mounjaro for weight loss?

No. Mounjaro is only covered for type 2 diabetes. If you want tirzepatide for weight loss, your provider would need to prescribe Zepbound, and your plan would need to include anti-obesity medication coverage. The active ingredient is the same, but insurance treats them as different medications based on the indicated use.

How do I know if my UnitedHealthcare plan covers Zepbound?

Check your plan formulary through the UnitedHealthcare member portal at myuhc.com, or call the member services number on your insurance card. Ask specifically whether anti-obesity medications are covered under your plan. Your HR department can also confirm if your employer elected this benefit.

Can I get tirzepatide covered through the sleep apnea pathway without a weight loss benefit?

Potentially, yes. If you have diagnosed moderate-to-severe obstructive sleep apnea, a BMI of 30 or higher, documented CPAP failure, and an A1C of 6.5% or lower, you may qualify for Zepbound coverage through the sleep apnea indication even if your plan excludes weight loss medications. Discuss this with your sleep specialist and prescribing provider.

How much does tirzepatide cost with UnitedHealthcare insurance?

With insurance coverage and the Lilly Savings Card, your copay can be as low as $25 per month. Without the savings card, copays typically range from $75 to $300 depending on your plan tier and cost-sharing structure. The peptide cost calculator on SeekPeptides can help you estimate total treatment costs.

What should I do if UnitedHealthcare denies my tirzepatide prior authorization?

First, read the denial letter carefully to understand the specific reason. Then file an internal appeal within 180 days, including additional documentation and a letter of medical necessity from your provider. Over 65% of appeals succeed. If internal appeals fail, request an external review within 4 months. The external review decision is binding on UnitedHealthcare.

Is compounded tirzepatide covered by UnitedHealthcare?

No. UnitedHealthcare does not cover compounded tirzepatide. Compounded versions are available as a cash-pay option at $299 to $399 per month through various compounding pharmacies and telehealth providers. See our guides on affordable compounded tirzepatide for sourcing options.

Will Medicare cover tirzepatide for weight loss in 2026?

A tentative agreement between Eli Lilly and the US government may expand Medicare coverage of tirzepatide for obesity-related use starting in April 2026, with out-of-pocket costs potentially capped at $50 per month. This is not finalized, so check CMS.gov for the most current information.

Can I use a GoodRx coupon for tirzepatide if UnitedHealthcare does not cover it?

GoodRx coupons can sometimes reduce the cash price of brand-name tirzepatide, but discounts on specialty medications are typically modest. The LillyDirect self-pay program usually offers better pricing for uninsured or uncovered patients. Compare options before deciding.

External resources

In case I do not see you, good afternoon, good evening, and good night. May your coverage stay approved, your copays stay low, and your results stay consistent.