Mar 21, 2026

Your FSA balance is sitting there. Thousands of dollars in pre-tax money, earmarked for medical expenses, ticking toward a deadline. And your semaglutide prescription costs hundreds per month. The connection seems obvious. But is it actually allowed?

Yes. You can use your FSA for semaglutide. But the rules are not as simple as swiping your benefits card at the pharmacy counter. The IRS has specific requirements about what qualifies as a medical expense, your plan administrator has their own verification process, and the type of semaglutide you use, whether that is brand-name Ozempic, FDA-approved Wegovy, or compounded semaglutide, changes which documentation you need. Get it wrong and your claim gets denied. Get it right and you save roughly 30% on every dose through tax-free spending.

This guide covers everything. The IRS rules that govern FSA eligibility. The qualifying medical conditions. The exact documentation your provider needs to write. The step-by-step reimbursement process. The differences between FSA and HSA coverage. The specific considerations for compounded versus brand-name formulations. And the strategies that experienced patients use to maximize every dollar in their flexible spending account.

Whether you are already on semaglutide and want to start paying with pre-tax dollars, or you are considering starting and want to understand the financial side before your first injection, this is the resource you will keep coming back to. SeekPeptides built this guide because the intersection of benefits administration and GLP-1 protocols confuses almost everyone, and bad information costs people real money.

What is an FSA and how does it apply to semaglutide

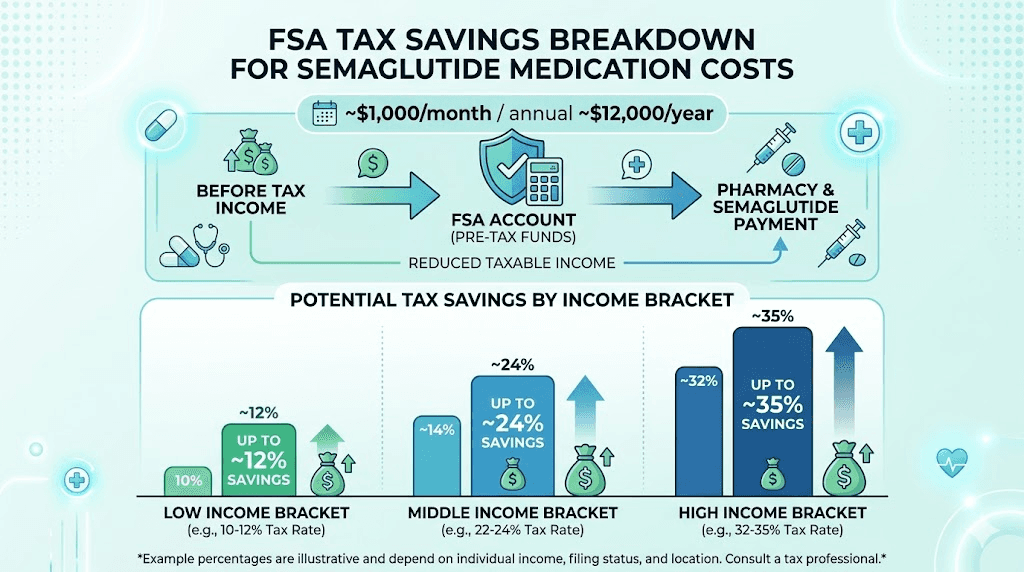

A Flexible Spending Account is an employer-sponsored benefit that lets you set aside pre-tax dollars for qualified medical expenses. The money comes out of your paycheck before federal income tax, state tax, and Social Security tax are calculated. That triple tax advantage is what makes FSAs so powerful for expensive medications like semaglutide.

Here is the critical distinction. An FSA is not insurance. It does not cover your medication the way a health plan does. Instead, it is a tax-advantaged savings vehicle. You contribute money throughout the year, and you spend that money on eligible medical expenses. The savings come from the tax break, not from someone else paying your bill.

For semaglutide specifically, this matters because the cost of GLP-1 medication can be substantial. Whether you are paying for compounded semaglutide out of pocket or covering copays on brand-name prescriptions, those dollars add up fast. Using FSA funds effectively reduces your cost by your marginal tax rate, which for most people falls between 22% and 37%.

FSA contribution limits and planning

The IRS sets annual contribution limits for FSAs. For the current plan year, you can contribute up to $3,300. Some employers also offer a matching contribution, though this is less common than with retirement accounts. The key planning consideration is that FSAs operate on a use-it-or-lose-it basis. Money you do not spend by the end of the plan year is generally forfeited, unless your employer offers a grace period of up to 2.5 months or a carryover of up to $640.

This deadline pressure actually works in your favor with semaglutide. Because the medication is taken weekly and costs are predictable, you can calculate almost exactly how much FSA money you will need for the year. If your semaglutide protocol costs $300 per month, that is $3,600 annually, more than enough to use your entire FSA contribution.

FSA versus HSA for semaglutide

People often confuse FSAs and HSAs. They sound similar. They both use pre-tax dollars. But the differences matter.

An HSA (Health Savings Account) requires a high-deductible health plan. The funds roll over indefinitely. You own the account even if you leave your employer. There is no use-it-or-lose-it pressure. HSA funds can be invested and grow tax-free.

An FSA does not require a specific health plan type. But the funds generally do not roll over. You lose access if you leave your employer. And the contribution limits are lower than HSA limits.

For semaglutide patients, both accounts work. The eligibility rules from the IRS are identical for both. The same qualifying conditions apply. The same documentation requirements exist. The only differences are in how the accounts themselves function, not in what they cover.

If you have access to both, use your HSA for longer-term medical savings and your FSA for predictable annual expenses like your weekly semaglutide doses. That way you are not risking FSA forfeiture while keeping your HSA growing for future needs.

IRS rules for FSA eligibility with semaglutide

The IRS does not maintain a list of specific medications that are FSA-eligible. Instead, they define categories of qualified medical expenses. Understanding these categories is essential because your FSA administrator will use them to approve or deny your claims.

IRS Publication 502 is the authoritative document. It states that you can include in medical expenses amounts paid for prescribed medicines or drugs. A prescribed drug is one that requires a prescription from a doctor to be obtained. Semaglutide, in all its forms, requires a prescription. That baseline requirement is met automatically.

But there is a catch. Not all prescribed medications automatically qualify for FSA reimbursement when they are used for weight management. The IRS makes a critical distinction between treating a diagnosed medical condition and pursuing general health improvement or cosmetic goals.

The medical necessity requirement

This is where most FSA claims for semaglutide succeed or fail. The IRS requires that the expense be primarily for the prevention or alleviation of a physical or mental defect or illness. Weight loss for general health or cosmetic improvement does not qualify. Weight loss to treat a specific diagnosed condition does.

That single distinction changes everything.

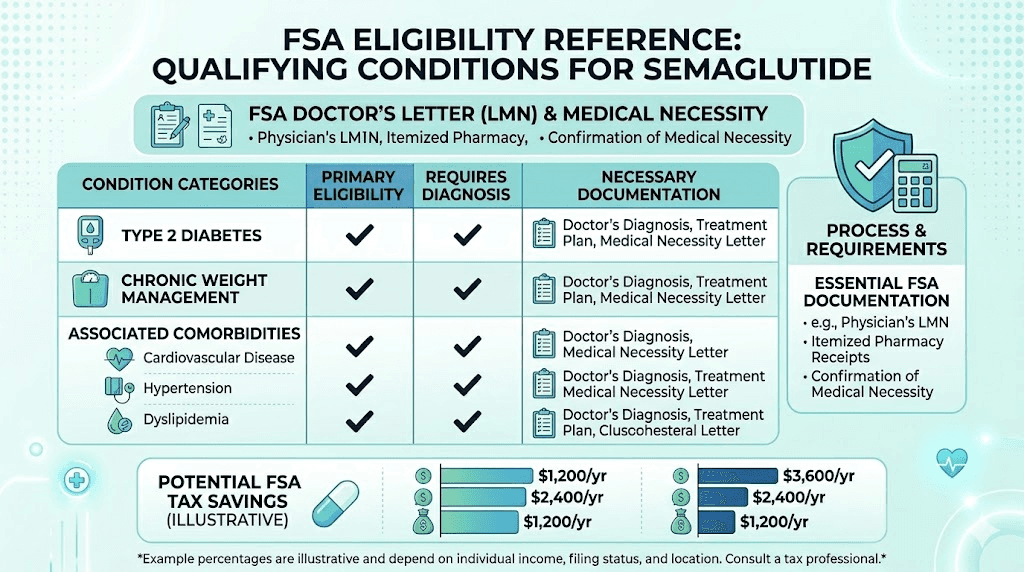

If your doctor prescribes semaglutide to treat type 2 diabetes, the medical necessity is clear and well-established. Diabetes is a diagnosed medical condition. Semaglutide (as Ozempic) has FDA approval for this indication. Your FSA claim will almost certainly sail through without additional documentation.

If your doctor prescribes semaglutide for weight loss, the situation requires more care. Weight loss itself is not a medical condition in the eyes of the IRS. But obesity is. Metabolic syndrome is. Hypertension related to excess weight is. The key is ensuring your prescription is tied to a diagnosed condition, not just a desire to lose weight.

Qualifying medical conditions

The following diagnosed conditions can make your semaglutide prescription FSA-eligible for weight management purposes. You do not need all of them. One qualifying diagnosis, properly documented, is sufficient.

Type 2 diabetes. This is the most straightforward qualifying condition. Semaglutide was originally developed and FDA-approved for type 2 diabetes management. If you have this diagnosis, your FSA eligibility for semaglutide is essentially automatic. No Letter of Medical Necessity is typically required, though keeping your diagnosis documentation accessible is still wise.

Obesity. When your healthcare provider documents obesity as a medical diagnosis (not just a lifestyle concern), semaglutide prescribed for treatment qualifies as a medical expense. The BMI threshold for obesity is 30 or above, or 27 or above with at least one weight-related comorbidity. Your provider can reference ICD-10 diagnosis codes E66.01 (morbid obesity due to excess calories) or E66.09 (other obesity due to excess calories).

Insulin resistance and prediabetes. When a provider prescribes semaglutide to treat insulin resistance or prevent progression to type 2 diabetes, it may qualify for FSA coverage. The documentation should reference specific lab values like elevated fasting glucose, elevated HbA1c, or abnormal glucose tolerance test results.

Metabolic syndrome. This cluster of conditions, including elevated blood pressure, high blood sugar, excess abdominal fat, and abnormal cholesterol levels, constitutes a diagnosed medical condition when documented by your provider. Semaglutide prescribed to treat metabolic syndrome qualifies.

Cardiovascular risk reduction. Wegovy received an expanded FDA indication for reducing cardiovascular events in adults with established cardiovascular disease and either obesity or overweight. If your prescription falls under this indication, the medical necessity argument is particularly strong.

Hypertension related to weight. When your provider documents that your blood pressure issues are connected to excess weight and prescribes semaglutide as part of the treatment plan, this qualifies as treatment of a specific diagnosed disease.

Ozempic versus Wegovy versus compounded semaglutide: FSA differences

The type of semaglutide you use affects your FSA experience. Not because the IRS treats them differently, but because plan administrators and verification processes handle them differently. Understanding these nuances prevents surprises at the pharmacy counter.

Ozempic (semaglutide for diabetes)

Ozempic is FDA-approved for type 2 diabetes. When your prescription is for this indication, FSA reimbursement is usually the smoothest. Your pharmacy claim goes through with your diagnosis code attached. The plan administrator sees a prescription medication treating a diagnosed condition. Approval is typically automatic.

However, many providers prescribe Ozempic off-label for weight loss. This is legal and medically accepted, but it changes your FSA documentation needs. Off-label use means the medication is being prescribed for a purpose other than its FDA-approved indication. Your FSA administrator may flag this and request additional documentation, specifically a Letter of Medical Necessity.

Wegovy (semaglutide for weight management)

Wegovy is FDA-approved specifically for chronic weight management. You might think this makes FSA eligibility straightforward. It does not. Even though Wegovy has FDA approval for weight loss, the IRS still requires that the expense treat a diagnosed medical condition. FDA approval and IRS eligibility are two different standards.

In practice, Wegovy prescriptions almost always require a Letter of Medical Necessity for FSA reimbursement. Your provider needs to document the specific medical condition being treated, not just the desire for weight loss. The good news is that almost everyone who qualifies for a Wegovy prescription also has a qualifying medical condition that can be documented.

The cost difference matters here too. Wegovy without insurance can run over $1,000 per month. Even with insurance, copays can be substantial. Using FSA funds for these copays is one of the most effective ways to reduce your effective semaglutide cost.

Compounded semaglutide

Compounded semaglutide is where things get more interesting. Compounded medications are custom-prepared by compounding pharmacies, often at significantly lower prices than brand-name versions. Many patients pay $150-400 per month for compounded semaglutide compared to $1,000+ for Wegovy.

The IRS does not distinguish between compounded and brand-name medications. If a prescribed medication treats a diagnosed medical condition, it qualifies. Period. Compounded semaglutide is FSA-eligible under the same rules as Ozempic or Wegovy.

But. FSA administrators sometimes push back on compounded medications. They may not recognize the pharmacy. The claim format may look different from standard prescription claims. And because compounded medications do not have NDC (National Drug Code) numbers in the same way brand-name drugs do, automated verification systems sometimes flag them.

The solution is proactive documentation. Before your first compounded semaglutide purchase, gather your prescription, your Letter of Medical Necessity, and your pharmacy receipt showing the medication name, dose, and prescriber. Submit these together with your claim. This front-loaded approach prevents the back-and-forth that delays reimbursement.

One critical requirement for compounded semaglutide FSA eligibility: the medication must come from a licensed compounding pharmacy. Compounded versions obtained without a real prescriber or from pharmacies that are not FDA-compliant will not qualify. If you are sourcing from a 503B outsourcing facility or a state-licensed 503A pharmacy with a valid prescription, you are on solid ground.

The Letter of Medical Necessity: your most important document

If there is one document that determines whether your FSA claim succeeds or fails, it is the Letter of Medical Necessity. Understanding what it needs to contain and how to get one from your provider will save you weeks of back-and-forth with your plan administrator.

What is a Letter of Medical Necessity

A Letter of Medical Necessity (LMN) is a document from your healthcare provider that explains why a specific treatment is medically necessary for your condition. It is not a prescription. It is not a diagnosis code. It is a written explanation that connects your medical condition to the treatment your provider has recommended.

Think of it as your provider making the case to your FSA administrator that this medication is treating a disease, not improving your appearance.

When you need one

You need a Letter of Medical Necessity when your semaglutide prescription is for weight management rather than type 2 diabetes. Here is the breakdown.

Probably do not need an LMN: Semaglutide prescribed as Ozempic for documented type 2 diabetes. The diagnosis code on your prescription usually satisfies FSA administrators.

Definitely need an LMN: Semaglutide prescribed for weight loss (Wegovy or compounded), off-label Ozempic for weight management, or any situation where the primary indication is not type 2 diabetes.

Should get one anyway: Every situation. Even if you think you do not need it, having an LMN on file prevents future disputes. Ask your provider during your next appointment. It takes them five minutes and saves you hours of appeals.

What your LMN must contain

An effective Letter of Medical Necessity for semaglutide FSA coverage should include these specific elements. Share this list with your provider so they know exactly what to write.

Your specific diagnosis. Not just "overweight" or "wants to lose weight." The letter needs a specific medical diagnosis with the corresponding ICD-10 code. Obesity (E66.01 or E66.09), type 2 diabetes (E11.x), metabolic syndrome (E88.81), or another qualifying condition.

The recommended treatment. Semaglutide should be named explicitly, including the formulation (Ozempic, Wegovy, or compounded semaglutide) and the prescribed dose. Your provider should reference the specific dosing protocol they have recommended.

Why the treatment is medically necessary. This is the critical section. Your provider needs to explain that the medication treats the diagnosed condition, that the condition poses health risks, and that the treatment is expected to improve health outcomes. Generic statements like "patient would benefit from weight loss" are weak. Specific statements like "patient has documented obesity with BMI of 34.2, comorbid hypertension, and elevated HbA1c of 6.1% indicating prediabetes; semaglutide is prescribed to treat these conditions and reduce cardiovascular risk" are strong.

Treatment duration. The IRS expects LMNs to include a specific treatment period with clear start and end dates. For semaglutide, your provider might write "12-month treatment course beginning [date]" or "ongoing treatment to be reassessed at 6-month intervals."

Provider credentials. The letter must come from a licensed healthcare provider. It should be on official letterhead, signed, and dated. A nurse practitioner, physician assistant, or physician can all write valid LMNs.

Step-by-step process for using FSA for semaglutide

Here is the exact process, from start to reimbursement. Follow these steps in order and you will minimize the chance of claim denials or delays.

Step 1: Verify your FSA plan covers prescription medications

This sounds obvious. It is not. Not all FSAs cover prescription medications. Some plans are "limited purpose" FSAs that only cover dental and vision expenses. Others may have specific exclusions for weight management medications. Before you commit to paying for semaglutide with FSA funds, call your plan administrator and ask two specific questions.

First: Does my plan cover prescription medications for diagnosed medical conditions? Second: Are there any specific exclusions for GLP-1 medications or weight management drugs?

Document the answers, including who you spoke with and when. If they confirm coverage, you are clear to proceed.

Step 2: Get your diagnosis documented

Schedule an appointment with your healthcare provider. During this visit, make sure they document your qualifying medical condition in your medical record. Ask them to note specific objective measurements: BMI, blood pressure, HbA1c levels, fasting glucose, lipid panel results. These numbers transform a subjective assessment into an objective medical diagnosis.

If you are already on semaglutide and your provider has already diagnosed a qualifying condition, you may just need to request that they write the LMN based on your existing medical records. Most providers are familiar with this process.

Step 3: Obtain your Letter of Medical Necessity

Ask your provider to write an LMN during the same appointment. Show them the requirements listed above. Many providers have templates they use regularly. Some will charge a small fee for the letter. This is also typically an FSA-eligible expense.

Get the original letter and make copies. You will need to submit it with your first FSA claim, and potentially again if you change pharmacies or renew your prescription.

Step 4: Fill your prescription

Whether you are filling at a retail pharmacy, a mail-order pharmacy, or a compounding pharmacy, keep your receipt. The receipt should show the medication name, the prescribing provider, the date, and the amount paid. For FSA purposes, you need receipts that clearly identify the purchase as a prescription medication.

If your pharmacy accepts FSA debit cards, you can try paying directly. Some point-of-sale systems will process it automatically when the pharmacy transmits the proper IIAS (Inventory Information Approval System) codes. If the card is declined, do not panic. Pay out of pocket and submit for reimbursement instead.

Step 5: Submit your claim

Most FSA administrators have online portals where you can upload documentation and submit claims. Here is what to include with your first claim.

Your pharmacy receipt showing the medication name, date, and amount. Your Letter of Medical Necessity. Your prescription or a copy of it. Any additional forms your specific FSA administrator requires.

For subsequent claims, you usually only need the pharmacy receipt. The LMN stays on file. However, some administrators require annual LMN renewals, so check your plan rules.

Step 6: Track reimbursement

After submitting, monitor your claim status through your FSA portal. Most claims process within 5-14 business days. If approved, funds are deposited directly to your bank account or a check is mailed. If denied, you will receive a notice explaining why.

Common denial reasons include missing documentation, LMN that does not meet requirements, or plan-specific exclusions. Most denials can be overturned by resubmitting with the right documentation.

Maximizing your FSA savings on semaglutide

Smart FSA planning can save you thousands of dollars on your semaglutide protocol. These strategies go beyond basic reimbursement.

Calculate your annual semaglutide cost first

Before your FSA enrollment period, calculate exactly what you will spend on semaglutide in the coming year. This prevents both over-contributing (and risking forfeiture) and under-contributing (and missing tax savings).

For compounded semaglutide at $200-400 per month, your annual cost is $2,400-4,800. For brand-name copays, calculate based on your specific insurance plan. Add in related expenses like provider visits, lab work, and injection supplies.

Then set your FSA contribution to match. If your total expected cost is $3,600 and the FSA limit is $3,300, contribute the maximum. The remaining $300 comes out of pocket with after-tax dollars.

Include related medical expenses

Semaglutide is not the only FSA-eligible expense in your weight management plan. You can also use FSA funds for provider visits related to your treatment, lab work ordered by your provider (blood panels, HbA1c tests, metabolic panels), prescription supplies like syringes and alcohol swabs, and other prescribed medications that treat your qualifying condition.

If your provider has you on a comprehensive protocol that includes semaglutide with B12 or semaglutide with glycine, those compounded formulations are also eligible. The same goes for any prescribed supplements that your provider recommends as part of your treatment plan, as long as they are prescribed for your diagnosed condition.

Time your purchases strategically

With FSAs, your full annual election is available from day one of the plan year, even though your contributions come out gradually from each paycheck. This means you can stock up on semaglutide at the beginning of the plan year if needed.

This is particularly useful if you are switching from one formulation to another, starting a new semaglutide protocol, or want to buy a three-month supply from a compounding pharmacy that offers bulk pricing. You get the full tax benefit on day one.

Do not forget the grace period

If your employer offers a grace period (up to 2.5 additional months after the plan year ends), you can incur eligible expenses during that window and still use the previous year funds. This gives you extra time to use any remaining balance on semaglutide purchases or related medical expenses.

Alternatively, if your employer offers a carryover option, up to $640 can roll into the next plan year. Know which option your employer provides and plan accordingly.

What happens when your FSA claim gets denied

Claim denials happen. They are frustrating but rarely permanent. Understanding why claims get denied and how to appeal puts you back in control.

Common denial reasons

Missing Letter of Medical Necessity. This is the most common reason. Your administrator needs documentation that ties your prescription to a diagnosed medical condition. Submit your LMN and resubmit the claim.

Insufficient diagnosis documentation. Your LMN might be too vague. "Patient needs semaglutide for weight management" is insufficient. "Patient has documented obesity (BMI 33.7, ICD-10 E66.09) with comorbid hypertension and insulin resistance requiring pharmacological intervention including semaglutide" is sufficient. Ask your provider to revise the letter with more specific language.

Pharmacy not recognized. This happens more frequently with compounded semaglutide from smaller pharmacies. Provide your pharmacy license number and contact information to your administrator. They may need to manually verify the pharmacy.

Receipt does not meet requirements. FSA administrators need receipts that show the patient name, medication name, prescribing provider, date, and amount. A credit card statement alone is usually not sufficient. Get an itemized receipt from your pharmacy.

Plan-specific exclusions. Some FSA plans exclude weight management medications.

If this is the case, your options are limited to appealing based on the medical necessity of treating your diagnosed condition (not weight management per se) or waiting for the next enrollment period to switch plans if available.

The appeal process

Most FSA administrators offer a formal appeal process. Here is how it typically works.

First, review the denial notice carefully. It should state the specific reason for denial and reference the plan provision that applies. This tells you exactly what documentation or information is missing.

Second, gather the missing documentation. If they want an LMN, get one. If your LMN was insufficient, get a revised version. If the pharmacy was not recognized, provide pharmacy credentials.

Third, submit your appeal in writing through the designated channel. Include a clear statement of why the claim should be approved, referencing the specific IRS rules that support your position. Attach all supporting documentation.

Fourth, track the appeal timeline. Most plans must respond within 30 calendar days. If you have not heard back, follow up in writing.

The appeal success rate is actually quite high when the claim was denied for documentation issues rather than fundamental ineligibility. If your medication genuinely treats a diagnosed medical condition and you can document that, persistence usually wins.

FSA coverage for semaglutide-related expenses

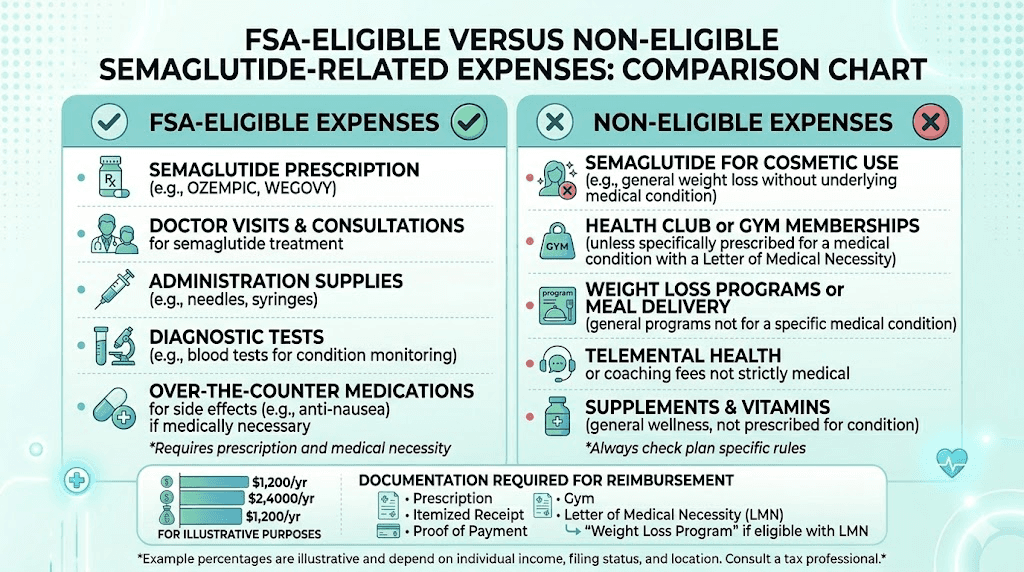

Your semaglutide treatment involves more than just the medication itself. Many related expenses also qualify for FSA reimbursement. Knowing what else you can claim maximizes your tax savings across your entire treatment plan.

Provider visits and consultations

Every office visit related to your semaglutide treatment is FSA-eligible. This includes your initial consultation where the provider evaluates you and writes the prescription, follow-up visits to monitor progress and adjust your dosing protocol, telehealth appointments for prescription renewals, and any specialist referrals related to your diagnosed condition.

If your provider charges for the Letter of Medical Necessity, that fee is also eligible. So are copays for any visit connected to your semaglutide treatment.

Laboratory work

Blood tests your provider orders as part of your semaglutide treatment qualify. Common tests include HbA1c monitoring, fasting glucose panels, comprehensive metabolic panels, lipid panels, liver function tests, and kidney function markers. These tests serve the dual purpose of monitoring your health on semaglutide and documenting the medical necessity of continued treatment.

Injection supplies

If you are using injectable semaglutide (which most formulations are), the supplies you need are FSA-eligible. This includes insulin syringes (the same type used for GLP-1 injections), alcohol prep pads, sharps disposal containers, and bandages. These are relatively small expenses individually but add up over a year of weekly injections.

Prescription anti-nausea medications

Nausea is one of the most common side effects when starting semaglutide, particularly during the first few weeks. If your provider prescribes anti-nausea medication to manage this side effect, that prescription is FSA-eligible because it is treating a side effect of a medication prescribed for a diagnosed condition.

Nutritional counseling

If your provider refers you to a registered dietitian as part of your treatment plan, those visits qualify for FSA reimbursement. This is especially relevant for patients following a specific diet plan on semaglutide or who need guidance on what to eat while on the medication. The referral should note that the nutritional counseling is part of treatment for your diagnosed condition.

What is NOT FSA-eligible

Some things you might expect to be covered are not. Over-the-counter supplements that are not prescribed by your provider do not qualify. Gym memberships, even if your provider recommends exercise. Meal prep services or specific food purchases. Health apps or weight tracking subscriptions. And any product marketed as a weight loss supplement that is not a prescription medication.

The line is clear: prescribed treatments for diagnosed conditions qualify. General wellness products do not.

Compounded semaglutide and FSA: special considerations

Compounded semaglutide deserves its own section because it is the most common scenario where FSA claims get complicated. The lower cost makes it attractive. The documentation requirements make it trickier.

Why compounded semaglutide FSA claims get flagged

When you fill a brand-name prescription at a retail pharmacy, the transaction generates standardized data that FSA systems recognize automatically. The NDC number, the pharmacy identifier, the prescriber NPI, all of these flow through established verification channels.

Compounded medications do not always flow through these same channels. The compounding pharmacy may not be in your FSA administrator network. The medication may not have a standard NDC code. The receipt format may differ from what automated systems expect. None of this means the claim is ineligible. It just means it may require manual review.

How to make compounded semaglutide FSA claims smooth

Preparation is everything. Before your first purchase, call your FSA administrator and let them know you will be submitting claims for compounded semaglutide from a compounding pharmacy. Ask what specific documentation they need. Some administrators have specific forms for compounded medication claims.

When you submit, include all of the following. Your prescription showing the medication (semaglutide), dose, and prescribing provider. A detailed receipt from the pharmacy showing the medication name, pharmacy name and license number, date, and amount. Your Letter of Medical Necessity. And if your administrator requests it, documentation that the pharmacy is a licensed compounding facility.

The pharmacies that cater to semaglutide patients, such as Empower Pharmacy, Belmar Pharmacy, and others, are generally familiar with FSA documentation requirements. Many will provide receipts formatted specifically for FSA submission. Ask your pharmacy if they offer this.

Compounded formulations with additional ingredients

Many compounding pharmacies offer semaglutide combined with other ingredients. Semaglutide with glycine and B12, semaglutide with methylcobalamin, semaglutide with niacinamide, and semaglutide with L-carnitine are all common formulations.

These combination formulations are still FSA-eligible as long as the overall compounded medication is prescribed by a healthcare provider for a diagnosed medical condition. The additional ingredients do not change the eligibility status. Your LMN should reference the specific formulation your provider has prescribed.

FSA for tirzepatide and other GLP-1 medications

If you are considering or currently using tirzepatide instead of semaglutide, the FSA rules are identical. The IRS does not distinguish between different GLP-1 medications. What matters is the diagnosis, not the specific drug.

This means everything in this guide applies equally to tirzepatide (Mounjaro/Zepbound), liraglutide (Saxenda), and any other prescribed GLP-1 medication. The qualifying conditions are the same. The LMN requirements are the same. The reimbursement process is the same.

If you are switching between GLP-1 medications, your existing LMN may still be valid as long as it references the underlying medical condition rather than a specific medication. However, having your provider update the LMN to reflect your current prescription is best practice.

The same applies to retatrutide and other next-generation GLP-1 receptor agonists. As long as the medication is prescribed by a licensed provider for a diagnosed medical condition, FSA eligibility follows the same framework.

Comparing costs across GLP-1 options with FSA

When factoring in FSA tax savings, the effective cost of different GLP-1 medications shifts. Here is how the math works for someone in the 24% federal tax bracket with an additional 7.65% FICA tax savings.

Medication | Monthly cost | Annual cost | FSA tax savings (~31%) | Effective annual cost |

|---|---|---|---|---|

Compounded semaglutide | $200-400 | $2,400-4,800 | $744-1,488 | $1,656-3,312 |

Wegovy (with insurance copay) | $100-300 | $1,200-3,600 | $372-1,116 | $828-2,484 |

Wegovy (no insurance) | $1,000-1,400 | $12,000-16,800 | $3,300 max FSA | $8,700-13,500 |

$200-500 | $2,400-6,000 | $744-1,860 | $1,656-4,140 |

The FSA contribution limit caps your tax savings. If your annual medication cost exceeds $3,300, you still get the maximum tax benefit, but only on the first $3,300. The rest comes from after-tax dollars. If you also have an HSA, you can use both accounts to maximize your pre-tax coverage.

Common mistakes people make with FSA and semaglutide

After researching hundreds of patient experiences and FSA claim outcomes, clear patterns emerge. These mistakes cost people money and cause unnecessary frustration. Avoid them.

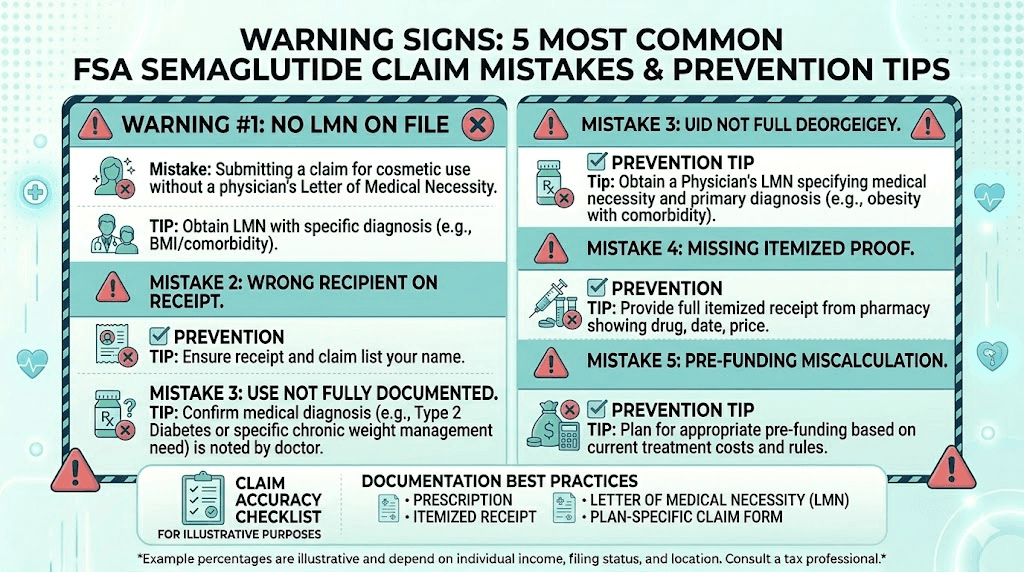

Mistake 1: Waiting until the claim is denied to get an LMN

This is the most expensive mistake in terms of time. You submit a claim without an LMN. It gets denied. You request an LMN from your provider, which takes 1-2 weeks. You resubmit. The resubmission takes another 5-14 business days to process. You have now spent a month waiting for reimbursement that could have been processed in two weeks if you had the LMN ready from the start.

Get your LMN before your first claim. Always.

Mistake 2: Under-contributing to your FSA

People are afraid of the use-it-or-lose-it rule, so they contribute conservatively. Then they spend their FSA balance by June and pay for the rest of the year with after-tax dollars. If you know you will be on semaglutide for the full year, contribute enough to cover it. The math is straightforward. Better to contribute the maximum and use it all than to leave tax savings on the table.

Mistake 3: Not keeping receipts

Digital or physical, you need them. Every pharmacy purchase, every provider visit, every lab test related to your semaglutide treatment. FSA administrators can request documentation for any claim, even months after reimbursement. If you cannot provide receipts when audited, you may have to repay the reimbursement.

Create a dedicated folder, digital or physical, for all semaglutide-related receipts and documentation. This takes five minutes to set up and saves hours of scrambling later.

Mistake 4: Assuming your FSA card will work at every pharmacy

FSA debit cards use the IIAS system to verify purchases at the point of sale. Not every pharmacy, especially compounding pharmacies, is set up for this. When your card gets declined, it does not mean the expense is ineligible. It just means the pharmacy could not verify it electronically.

Always have a backup payment method. Pay out of pocket and submit for reimbursement if the card does not work. The reimbursement process takes longer but the result is the same.

Mistake 5: Forgetting to re-enroll

FSA enrollment does not automatically renew in most plans. You need to actively re-enroll during each open enrollment period. If you forget, you lose access to FSA funds for the entire next plan year. Set a calendar reminder for your employer open enrollment period.

FSA and semaglutide for specific situations

Different life circumstances create different FSA considerations. Here are the most common scenarios semaglutide patients encounter.

Starting semaglutide mid-year

If you begin your semaglutide protocol after your FSA enrollment period, you cannot change your contribution until the next enrollment period unless you experience a qualifying life event. This means you might not have enough FSA funds to cover the rest of the year.

However, if starting a new prescription medication constitutes a change in coverage under your plan, it may qualify as a life event that allows mid-year FSA changes. Check with your benefits administrator. Some plans are more flexible than others.

Changing jobs

When you leave an employer, you generally lose access to your FSA. Unused funds are forfeited. You may have the option to continue your FSA through COBRA continuation, but the cost is often not worth it because you lose the pre-tax benefit and pay the full administrative cost.

If you know you are changing jobs, try to use your FSA balance before your last day. Stock up on semaglutide if your pharmacy allows it. Fill prescriptions early. Use any remaining balance on other eligible medical expenses.

Using FSA for a spouse or dependent

Your FSA can cover eligible medical expenses for your spouse and tax dependents, even if they are not covered by your health insurance plan. If your spouse is on semaglutide, you can use your FSA to cover their medication costs. The same documentation requirements apply.

Switching from brand-name to compounded semaglutide

Many patients start on brand-name Wegovy or Ozempic and later switch to compounded semaglutide for cost savings. Your existing LMN may still work, but it is best to have your provider update it to reflect the compounded formulation. This prevents any questions from your FSA administrator about the change.

The good news is that switching to compounded semaglutide often brings your annual cost below the FSA contribution limit, meaning you can cover the entire expense with pre-tax dollars. That is a significant financial advantage over brand-name medications where the cost far exceeds what an FSA can cover.

Dose changes during the year

As you progress through your semaglutide dosing protocol, your dose may increase. This changes your monthly cost, which could affect whether your FSA contribution covers the full year. If your costs increase significantly, you cannot change your FSA contribution mid-year unless it qualifies as a change in status event.

Plan for the maximum expected dose when calculating your FSA contribution. If you start at 0.25mg and plan to titrate up to 2.5mg, budget for the higher dose for the majority of the year.

State-by-state considerations

FSA rules are primarily federal, governed by IRS regulations. However, state laws can affect certain aspects of your FSA and semaglutide experience.

Some states have their own tax codes that may not conform to federal FSA rules. In most states, FSA contributions are exempt from state income tax in addition to federal tax. But a few states (like New Jersey and California for some accounts) may treat the contributions differently. Check your state tax rules to understand your exact savings.

State regulations also affect compounding pharmacy licensing. If you are purchasing compounded semaglutide from an out-of-state pharmacy, verify that the pharmacy is licensed in your state or that your state allows out-of-state compounding. This affects both the legality of the purchase and your FSA administrator willingness to reimburse it.

Planning ahead: FSA open enrollment strategy for semaglutide patients

The best time to optimize your FSA for semaglutide is during open enrollment. Here is a planning framework.

Calculate your expected annual medication cost

Start with your current monthly semaglutide cost. Factor in any planned dose changes. Add related expenses like provider visits, lab work, and supplies. Multiply monthly costs by 12 for your annual estimate.

If you are on compounded semaglutide at $250/month, your medication cost alone is $3,000 annually. Add four provider visits at $50 copay each ($200), two lab panels at $30 each ($60), and injection supplies at roughly $50 for the year. Total: approximately $3,310. That is almost exactly the FSA contribution limit, meaning you can cover virtually everything with pre-tax dollars.

Consider your other medical expenses

Remember that your FSA covers all qualified medical expenses, not just semaglutide. If you also have dental work planned, vision expenses, other prescriptions, or anticipated medical procedures, factor those into your contribution calculation. Every dollar that goes through your FSA saves you roughly 30% compared to paying with after-tax money.

Coordinate with your HSA if applicable

If you have access to both an FSA and an HSA (which requires a limited-purpose FSA), coordinate your strategy. Use the FSA for predictable expenses like semaglutide. Use the HSA for unexpected medical costs or long-term savings. This dual approach maximizes your tax advantage across both accounts.

Set up automatic payments

If your pharmacy accepts FSA debit cards, set up automatic monthly payments. This ensures your FSA funds are used consistently throughout the year and prevents the year-end scramble to spend remaining funds. For compounding pharmacies that do not accept FSA cards, set a monthly reminder to submit reimbursement claims so they do not pile up.

The bigger picture: total cost optimization for semaglutide

FSA savings are one piece of a larger cost optimization strategy for semaglutide patients. Combining multiple approaches can dramatically reduce your out-of-pocket costs.

Insurance coverage. If your health insurance covers semaglutide, your FSA covers the copay. This combination provides the lowest total cost. Check with your insurer about qualification requirements and coverage details. For Anthem, Blue Cross Blue Shield, UnitedHealthcare, and other major carriers, coverage policies vary but have been expanding.

Compounded semaglutide pricing. If insurance does not cover your medication, compounded semaglutide is typically 60-85% less expensive than brand-name Wegovy. Combined with FSA tax savings, the effective cost drops further. Research reputable compounding pharmacies and compare pricing.

Payment plans. Some pharmacies and telehealth providers offer buy now, pay later options for semaglutide. You can use these to spread costs across months while submitting FSA reimbursement claims for each payment.

Tax deductions. If your total medical expenses (including semaglutide) exceed 7.5% of your adjusted gross income, you may be able to deduct them on your tax return. This is separate from and in addition to FSA benefits. However, you cannot claim a tax deduction for expenses already reimbursed through your FSA.

SeekPeptides members get access to detailed cost comparison tools and protocol guides that help identify the most cost-effective approach for their specific situation. Understanding the full picture of insurance, FSA benefits, compounding options, and tax strategies often reveals savings that patients miss when looking at each piece in isolation.

Frequently asked questions

Can I use my FSA debit card directly at the pharmacy for semaglutide?

Yes, if the pharmacy is set up with the IIAS verification system. Most retail pharmacies accept FSA cards for prescription medications. Compounding pharmacies may or may not accept FSA cards. If the card is declined, pay out of pocket and submit for reimbursement through your FSA portal.

Do I need a Letter of Medical Necessity every year?

Most FSA plans require annual renewal of Letters of Medical Necessity. Check with your plan administrator. Some accept letters that cover a multi-year treatment period, while others require annual updates. Getting a new LMN during your annual checkup is the easiest approach.

Is compounded semaglutide FSA-eligible even though it is not a brand-name drug?

Yes. The IRS does not distinguish between brand-name and compounded medications. As long as the medication is prescribed by a licensed provider for a diagnosed medical condition and obtained from a licensed pharmacy, it qualifies. Compounded semaglutide follows the same FSA rules as Ozempic or Wegovy.

Can I use my FSA for semaglutide prescribed off-label for weight loss?

Yes, if the prescription treats a diagnosed medical condition. Off-label prescribing is common and legal. Your Letter of Medical Necessity needs to clearly state the diagnosed condition being treated. The fact that semaglutide is being used off-label does not affect FSA eligibility as long as the underlying medical necessity is documented.

What if my employer FSA plan specifically excludes weight loss medications?

If your plan has a specific exclusion, you have a few options. First, check whether the exclusion applies to weight loss medications generally or to medications treating obesity as a diagnosed disease. These are different categories under IRS rules. Second, appeal based on the medical necessity of treating your specific diagnosed condition. Third, consider whether your HSA (if you have one) has the same exclusion. HSA eligibility is determined by IRS rules, not employer plan provisions.

How much can I save using FSA for semaglutide?

The savings depend on your tax bracket and how much you spend on semaglutide annually. At a combined federal and FICA tax rate of roughly 31%, you save approximately $31 for every $100 spent through your FSA. On $3,000 of annual semaglutide costs, that is approximately $930 in tax savings per year.

Can I use FSA funds for semaglutide injection supplies?

Yes. Syringes, alcohol prep pads, sharps containers, and other supplies needed for your semaglutide injections are FSA-eligible medical supplies. Keep receipts for these purchases and submit claims the same way you would for the medication itself.

What happens to my FSA if I stop taking semaglutide mid-year?

Your FSA contribution is set for the year and cannot be changed mid-year unless you experience a qualifying life event. If you stop semaglutide and have remaining FSA funds, use them for other eligible medical expenses before the plan year ends. This is another reason to consider your full range of medical expenses when setting your FSA contribution, not just semaglutide costs.

External resources

For researchers serious about optimizing their peptide protocols and understanding every cost-saving option available, SeekPeptides offers the most comprehensive resource available, with evidence-based guides, proven protocols, and a community of thousands who have navigated these exact questions.

In case I do not see you, good afternoon, good evening, and good night. May your FSA claims stay approved, your tax savings stay maximized, and your semaglutide protocols stay effective.